When to start retirement planning is a critical question that often looms large in the minds of expatriates, especially those at the CXO level residing in UAE.

As experts suggest, starting early can significantly influence your financial stability post-retirement.

In this comprehensive guide, we will delve deep into understanding the basics of retirement planning, the importance of saving for retirement, and discuss how much money you might need for a comfortable life after retiring.

The role of individual retirement accounts (IRAs) in maximizing returns and strategic investing approaches during different career phases are other essential topics we’ll cover.

Lastly, managing debt levels prior to retirement, estate planning alongside market trends reviewing, along with potential activities and unexpected expenses during the early retirement phase will be addressed.

This information should help you determine when to start retirement planning effectively based on your unique circumstances.

When to Start Planning for Retirement

As a savvy CXO in UAE, you know that securing your financial future requires understanding the basics of retirement planning.

This involves deciding when to start saving and choosing the right accounts and investments.

Evolution of Effective Retirement Planning Over Time

Effective retirement planning has evolved over time. In today’s dynamic economic environment, relying solely on pension plans may not be enough.

Diversifying your investment portfolio through various channels like stocks, bonds, and mutual funds is often recommended for consistent growth.

This approach allows you to maximize potential returns and mitigate risks associated with market volatility. For instance, Quadra Wealth helps Middle East residents and ex-pats achieve financial freedom by providing structured notes that offer steady growth regardless of market conditions.

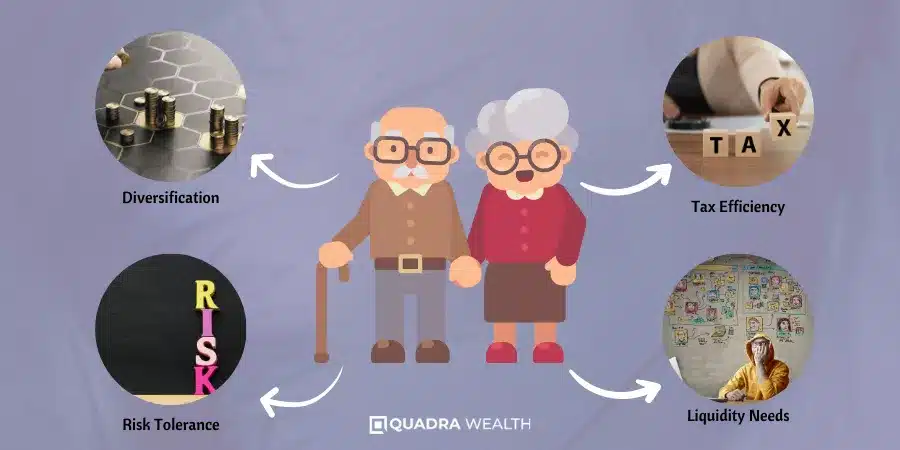

- Diversification: Spreading investments across different asset classes reduces risk.

- Risk Tolerance: Assess how much risk you’re willing to take on before deciding where to invest.

- Tax Efficiency: Maximize tax efficiency within your portfolio by investing in tax-advantaged accounts like Individual Retirement Accounts (IRAs).

- Liquidity Needs: Your liquidity needs will determine what types of assets best suit your strategy.

Retirement planning isn’t just about setting aside money every month. It requires strategic thinking based on personal circumstances, lifestyle aspirations, and long-term financial goals.

By starting early and making informed decisions along the way, you can set yourself up for a comfortable and secure post-retirement life.

Key takeaways

"Secure your financial future by understanding the basics of retirement planning. Start early, diversify investments, and maximize tax efficiency with Quadra Wealth's structured notes.

Importance of Saving for Retirement

As a CXO in the UAE, saving for retirement is crucial for financial planning. It’s not just about putting away money; it’s about creating a safety net for financial security during your golden years.

How much money you'll need for a comfortable post-retirement life

The amount needed to live comfortably after retiring varies depending on individual circumstances such as lifestyle choices, family plans, relocation possibilities, and healthcare needs. However, experts suggest aiming to save around $1 million by retirement.

Starting early can make this goal more achievable due to the power of compound interest. Even small amounts saved regularly can grow significantly over time.

Inflation rates and rising living costs make having substantial savings crucial. Unexpected expenses such as medical emergencies or major home repairs are inevitable occurrences that could potentially drain your resources if unprepared.

Ensure a steady income stream post-retirement through savings and investments like structured notes provided by Quadra Wealth. Factor in potential sources of passive income such as rental properties, dividends from stocks, and royalties from intellectual property.

Use online calculators available on websites like Bankrate to determine how much you need to save for retirement considering all factors. They take into consideration various parameters including current age, expected retirement age, and current annual income, providing an estimate based on those inputs.

Tips For Achieving Your Retirement Saving Goal:

- Create A Budget: A detailed budget helps track spending habits while identifying areas where cutbacks can be made, freeing up funds toward saving goals.

- Diversify Investments: In addition to traditional savings accounts, consider investing in diverse avenues offering higher returns albeit with associated risks.

- Prioritize Debt Repayment: Paying off high-interest debts sooner frees up more money for achieving long-term goals.

- Maximize Employer Matched Contributions: If applicable, ensure contributing enough within employer-sponsored pension schemes allowing maximum matching contributions, thus effectively doubling a certain portion of your investment.

Key takeaways

The importance of saving for retirement cannot be overstated, especially in the UAE where unexpected expenses and rising living costs can drain your resources. To ensure a comfortable post-retirement life, experts suggest aiming to save around $1 million by retirement by starting early and diversifying investments while prioritizing debt repayment and maximizing employer-matched contributions. Creating a budget is also crucial in tracking spending habits and identifying areas where cutbacks can be made toward achieving long-term savings goals.

Individual Retirement Account (IRA) Benefits

Are you a UAE-based CXO or ex-pat who doesn’t have access to workplace pension schemes? Fear not, an Individual Retirement Account (IRA) could be your saving grace.

An IRA is not just another savings account; it’s a powerful tool that provides tax advantages allowing your money to compound faster.

Maximizing Returns through Individual Retirement Account

An Individual Retirement Account (IRA) is like a savings account on steroids. It’s where you put stocks, bonds, mutual funds, and other assets.

Unlike regular investment accounts, IRAs offer tax benefits that can significantly enhance your ability to save for retirement.

Contribs to a trad or Roth IRA can provide tax benefits now, or later when you start taking out cash.

- Traditional IRAs: Contributions are often tax-deductible, all transactions and earnings within the IRA have no impact on taxable income, and withdrawals at retirement are taxed as income except for those portions of the withdrawal corresponding to contributions that were not deducted.

- Roth IRAs: Contributions are made with after-tax assets; all transactions within the IRA have no impact on taxable income; and withdrawals usually aren’t taxed provided certain conditions are met.

The magic behind maximizing returns through individual retirement accounts lies in their unique feature: compounding interest over time. Compounding allows any annual gains from investments inside your IRA to generate their own gains in subsequent years. It’s like a snowball effect, but with money.

Starting early gives compounding ample time to work its magic, resulting in substantial growth by the end of your retirement term. For instance, if you invest $5k annually between the ages of 25-35 ($50k total contribution), it would grow larger than the same amount invested annually between 35-65 ($150k total contribution); assuming both portfolios earn the same rate of return throughout the tenure.

In conclusion, opening up an individual retirement account (IRA) should be part of your overall financial strategy toward achieving a comfortable post-retirement lifestyle while residing in the UAE. No matter when you start, every contribution to your retirement fund is a step in the right direction.

Remember, Quadra Wealth is always ready to assist and guide you along this journey, ensuring you reach your desired destination safely and securely without unnecessary detours or delays. Let’s create a prosperous tomorrow today.

- Tax advantages

- Compounding interest

- Investment flexibility

- Long-term financial security

- Missed tax advantages

- Limited growth potential

- Lack of investment options

- Increased risk of insufficient retirement savings

Key takeaways

The article discusses the benefits of opening an Individual Retirement Account (IRA) for UAE-based CXOs and ex-pats who do not have access to workplace pension schemes. IRAs provide tax advantages that allow money to compound faster, maximizing returns through compounding interest over time. Opening an IRA should be part of one's overall financial strategy toward achieving a comfortable post-retirement lifestyle in the UAE.

Strategic Investing in Retirement Planning for UAE Expats

Strategic investing is crucial for retirement planning, especially for UAE ex-pats and CXO-level residents. Done correctly, it can help achieve financial goals faster.

Aggressive Investing in Early Career Years

When starting your career, it’s recommended to adopt aggressive investment strategies like investing in high-risk, high-reward assets such as stocks.

Equities have been known to provide greater returns over the long haul, and younger individuals are better equipped to rebound from potential losses due to having more time on their side.

- Risk tolerance: Assess your risk tolerance before adopting an aggressive strategy. Not everyone can stomach significant market fluctuations.

- Diversification: Even within an aggressive portfolio, diversification is key. Spread your investments across different sectors and regions.

- Frequent review: Aggressive portfolios require frequent reviews and adjustments based on market conditions and personal circumstances.

- High Growth Potential

- Time Advantage

- Capitalizing on Risk

- Building Wealth

- Increased Volatility

- Higher Risk

- Emotional Stress

- Limited Diversification

Conservative Investing Approaches Close to Retirement

As you approach retirement age (around 50-55 years old), your investment approach should become more conservative. Preserving capital becomes paramount as there’s less time left for recovery from any major loss.

Conservative investments like bonds or money-market funds are considered safer options during these times due to their low volatility nature compared to stocks.

- Bonds: Bonds provide regular income through interest payments while protecting the principal amount invested.

- Annuities: Annuities offer guaranteed income streams post-retirement but come with certain limitations like lack of access until a specific age limit is reached and higher fees.

The transition between these two stages is gradual, allowing for a smoother adjustment toward changing risk profiles associated with the aging process.

Regular consultation with professional advisors ensures proper alignment of individual needs versus available resources, optimizing overall returns without compromising safety aspects related to future cash flow requirements during the golden years ahead.

Remember, “Time and compound interest are the greatest allies of an investor” – Albert Einstein.

- Capital Preservation

- Stability and Income

- Reduced Volatility

- Risk Mitigation

- Limited Growth Potential

- Inflation Risk

- Lower Income Generation

- Missed Growth Opportunities

Key takeaways

The article discusses the importance of strategic investments in retirement planning for UAE ex-pats. It recommends adopting aggressive investment strategies like investing in high-risk, high-reward assets such as stocks during early career years and transitioning to conservative investments like bonds or annuities close to retirement age. The key takeaways include assessing risk tolerance, diversifying investments, frequent portfolio reviews, and consulting with professional advisors for the proper alignment of individual needs versus available resources.

Early-Retirement Phase Activities & Unexpected Expenses

Retirement planning can be tough, especially when you’re an ex-pat or a CXO in UAE with financial obligations. One of the most critical aspects is predicting your lifestyle during the early retirement phase and preparing for unexpected expenses that may arise in the middle-retirement period.

The first step is identifying the activities you plan on engaging in during your early retirement years. Do you want to travel extensively or take up new hobbies? Before deciding how much money to save for retirement, consider the expenses associated with your chosen activities.

To help visualize these costs better, consider creating a detailed budget. List down all potential expenditures related to each activity – from travel tickets and accommodation costs if traveling is part of your plan, to equipment purchases for any hobby pursuits. Don’t forget about regular living expenses like groceries, utility bills, and healthcare too.

Activities to Consider:

- Travel: Consider factors such as destination choice (local vs international), frequency of trips per year, and travel-related expenses.

- Hobbies: Costs can vary greatly depending on whether it’s something simple like reading books versus more expensive ones like golfing or sailing.

- Lifestyle Choices: Eating out frequently? Attending concerts/theatre shows regularly? These add up over time.

Aside from planned activities, it’s equally important to account for unexpected expenses likely during the middle-retirement period. Medical emergencies are prime examples here.

While we hope they never occur, being financially prepared ensures peace of mind knowing there are enough retirement funds available should anything happen.

An effective way to manage these unpredictable costs involves setting aside a specific ’emergency fund’ within the overall retirement savings pool which remains untouched unless absolutely necessary.

Some experts recommend maintaining 3-6 months’ worth of living expenses within this fund as a safe buffer amount.

Mitigating Risk With Insurance Coverage

Investing in insurance policies providing coverage against major risks such as serious illness or disability is another strategy to consider. By doing so, we not only mitigate risk exposure significantly but also ensure our hard-earned savings aren’t depleted suddenly due to unanticipated events.

According to The Motley Fool, “Retirees should anticipate spending an average of $4,300 annually per person on healthcare.” Hence, ensuring adequate insurance coverage becomes a crucial aspect of the comprehensive retirement planning process.

Key takeaways

Retirement planning for ex-pats and CXOs in the Middle East involves identifying activities during the early retirement phase, creating a detailed retirement budget to visualize costs, and accounting for unexpected expenses like medical emergencies by setting aside an emergency fund or investing in insurance policies that provide coverage against major risks. It is important to prepare financially for both planned and unforeseen expenses during retirement.

Estate Planning and Reviewing Market Trends

As retirement approaches, it’s crucial to consider estate planning and reviewing market trends. Craig L. Israelsen, a renowned financial advisor, emphasizes these components as part of an effective retirement strategy for UAE residents and expatriates at the CXO level.

The Importance of Estate Planning

Estate planning involves making arrangements for your assets to ensure they are distributed according to your wishes after you pass away. It’s more than just drafting a will.

This process can be complex but is essential for protecting your loved ones’ financial future. Investopedia’s guide on estate planning provides detailed insights into this topic.

Avoid Becoming a "Micromanager"

Craig Israelsen advises against becoming a “micromanager” who reacts impulsively based on daily market noise. Instead, focus on maintaining a balanced portfolio aligned with your long-term goals.

Reviewing Market Trends Regularly

Staying informed about broader economic trends that may affect investment performance over time is important. Regular review of these trends allows investors to make informed decisions regarding their portfolios without being swayed by transient market events. CNBC’s article on understanding macroeconomic indicators can help navigate through this aspect.

Maintaining a Balance Between Reactivity and Proactivity

- Risk Tolerance: Your risk tolerance should inform how reactive or proactive you are when managing investments during volatile periods.

- Diversification: This principle suggests spreading investments across various asset classes (stocks, bonds, etc.) to reduce risk.

- Frequent Rebalancing: To maintain desired asset allocation, rebalance your portfolio periodically.

- Patient Investing: In times of uncertainty, it pays off to remain patient and stick with a well-thought-out investment plan.

Navigating the Retirement Journey with Confidence

Taking control of both estate planning and regular reviews of market trends forms an integral part of achieving financial independence post-retirement.

Remember, the goal isn’t necessarily about timing the markets perfectly, but rather ensuring that your overall strategy aligns with personal objectives while taking into account changing economic conditions.

This way, you’ll be better equipped not only to build wealth effectively but also to preserve it successfully throughout your retirement years.

Key takeaways

The retirement planning journey involves estate planning and reviewing market trends. It's important to avoid micromanaging investments based on daily market noise and instead focus on maintaining a balanced portfolio aligned with long-term goals. Regularly reviewing broader economic trends can help investors make informed decisions while balancing reactivity and proactivity through risk tolerance, diversification, frequent rebalancing, and patient investing is key to navigating the retirement journey with confidence.

Managing Debt Levels Prior to Retiring

One of the most critical steps in preparing for a comfortable retirement is managing and reducing your debt levels. It’s an aspect that many overlook, but it can significantly impact your financial stability post-retirement.

Paying down mortgage loans, clearing car debts, and reducing credit card liabilities not only provides you with peace of mind but also allows more flexibility with living costs after retiring.

If you’re planning to retire in the UAE as an expatriate or resident at the CXO level, here are some strategies to help manage your debt effectively:

- Paying off Mortgage Loans: If possible, aim to pay off your mortgage before retirement. Owning your home outright eliminates one of the biggest monthly expenses for most people. You might consider refinancing if interest rates have dropped since you took out the loan.

- Clearing Car Debts: Try to avoid financing new vehicles right before retirement when income may be limited. Instead, plan ahead so that any auto loans are paid off well before you stop working.

- Reducing Credit Card Liabilities: High-interest credit card debt can quickly eat into savings set aside for retirement. Consider consolidating these debts into a lower interest rate loan or paying them down aggressively while still employed.

The goal should always be entering retirement with as little debt as possible because once retired, income often becomes fixed, making it harder to handle large payments each month.

In addition to this traditional approach towards managing personal finance pre-retirement, there’s another strategy gaining popularity among savvy investors – investing through structured notes offered by Quadra Wealth.

These provide consistent growth opportunities, helping individuals achieve their long-term financial goals faster, thus enabling them to better tackle any remaining debts prior to retiring.

To ensure the successful implementation of these strategies, it’s important to have access to professional advice tailored specifically around individual circumstances rather than adopting generic solutions promoted widely across various platforms.

For instance, residents in the UAE who hold senior positions within organizations (CXOs) would likely require different approaches compared to average employees due to higher incomes coupled with greater investment options available to them.

Therefore, engaging an experienced wealth management firm like Quadra Wealth could prove invaluable in guiding such individuals towards achieving their unique financial objectives efficiently without compromising lifestyle choices during the golden years post-retirement.

Key takeaways

Managing debt levels is crucial for a comfortable retirement. Paying off mortgage loans, clearing car debts, and reducing credit card liabilities can provide peace of mind and flexibility with living costs after retiring. Expatriates or residents at the CXO level in the UAE should aim to enter retirement with as little debt as possible while also considering investing through structured notes offered by Quadra Wealth for consistent growth opportunities.

Conclusion

In conclusion, effective retirement planning is crucial for UAE expatriates to ensure a financially secure and fulfilling post-work life. By starting early, understanding diversifying investments, and managing debt levels wisely, individuals can lay a strong foundation for their future.

Embracing proactive financial strategies and staying informed about market trends is essential for navigating the complexities of retirement planning. With careful consideration of lifestyle preferences and diligent financial management, expatriates can embark on their retirement journey with confidence and peace of mind.

Ultimately, a well-prepared retirement plan tailored to individual needs promises a stable and prosperous future in the UAE.

FAQs in Relation to When to Begin Retirement Planning

Start planning for retirement in your early 20s to take advantage of compounding interest.

Start saving for retirement as soon as you start your career to give your savings ample time to grow through the power of compounding.

The 70% rule suggests that retirees will need about 70% of their pre-retirement income annually during post-retirement years, helping estimate how much money one needs after retiring.

It’s important to note that personal investment experiences should guide your retirement planning, not specific financial institutions or products unrelated to the topic.

Also, remember that non-financial retirement planning aspects such as health and travel are just as important as financial planning.

Finally, avoid any form of speculative or risky investments when planning for a worry-free retirement.