70% of life goes by without retirement planning. A secure life waits ahead for those who plan. The non-planners struggle till the end. They have to deal with the uncertainty of rising living costs, healthcare expenses, and not having enough savings to sustain their lifestyle. Proper planning for retirement is crucial if you want to live a quality life. In this aspect, life insurance can be a powerful retirement planning strategy. A Life Insurance Retirement Plan offers protection and immense growth potential allowing individuals to secure their financial future.

Read on to learn how you can prepare for retirement with life insurance.

What Is a Life Insurance Retirement Plan?

A LIRP is a method for building wealth over time that uses the cash value feature of a permanent life insurance policy. Permanent life insurance policies, such as universal life or indexed universal life, have a cash value component that increases over time, in contrast to term life insurance, which only offers a death benefit for a predetermined amount of time.

A LIRP comes with the benefits of a life insurance policy and the ability to build cash value which supports the individual when they retire. Insurance can help diversify your retirement portfolio and offer tax advantages. Most importantly the plan provides peace of mind.

The policyholder in a LIRP has the option to contribute more than the minimal amount needed to maintain the policy’s validity. The additional contributions contribute to the cash value’s growth, which is subject to tax deferral. This accrued monetary worth can eventually be accessed through insurance loans or withdrawals after retirement.

The main goal of a LIRP is to provide both a death benefit and a supplemental income source during retirement. The policyholder still enjoys the security of life insurance coverage while using the accumulated cash value as an additional financial resource.

Importance of Life Insurance Retirement Plan

The importance and benefits of a life insurance retirement plan aren’t limited to accumulating money. It is about protecting the future of your loved ones and making sure you have enough money for the future after you retire. Building wealth is the major goal to pay for your living after retirement. However, life insurance adds a special component to it. The insurance offers a tax-advantaged means to accumulate wealth while protecting your family’s financial future in the case of your death.

Also Read– How to Achieve Financial Independence and Retire Early with the FIRE Movement

How LIRPs Work

A Life Insurance Retirement Plan operates similarly to other permanent life insurance plans but it is focused more on the dual goals of cover for family after death protection and cash value growth. Read on to learn how LIRPs work-

- Choose a Permanent Life Insurance Policy– A LIRP starts with selecting a type of life insurance policy, such as a whole life policy or universal life insurance. Unlike term insurance, these policies last for your entire lifetime. They also feature a cash value component.

- Make Premium Payments– Regular premium payments are made to keep the policy active. Part of the premium goes toward the cost of insurance (to provide the death benefit), while the rest is allocated to the policy’s cash value account.

- Cash Value Growth– The cash value component grows over time. In whole life insurance, this growth is guaranteed and predictable. In universal or indexed universal life insurance, the liquidity of money grows based on the performance of certain investments or stock indices. It provides potentially higher returns but with some risks.

- Accessing the Cash Value– Once enough cash value has built up, you can access these funds through tax-advantaged policy loans or withdrawals. These funds can serve as a source of supplemental income during retirement, helping you cover expenses without relying solely on other retirement accounts.

- Repaying Policy Loans– If you sign up for cash value life insurance, you can choose to repay the loan or allow it to be deducted from the death benefit when you pass away. If unpaid, the loan may reduce the overall death benefit paid out to your beneficiaries.

- Tax Advantages– One of the key benefits of a LIRP is its tax advantages. The cash value grows on a tax-deferred basis, meaning you won’t pay taxes on the growth until you withdraw or borrow from it. Additionally, policy loans are typically not considered taxable income.

Who Should Get a Life Insurance Retirement Plan (LIRP)?

A Life Insurance Retirement Plan isn’t suitable for everyone, but it can be a valuable option for certain individuals. Here’s who might benefit from a LIRP-

- High-Income Earners– Individuals who have already maxed out contributions to other tax-advantaged retirement accounts, such as pension schemes or government-backed savings plans, may find a LIRP useful as additional retirement savings. The tax-deferred growth of the cash value can help reduce their taxable income and provide an extra source of retirement income.

- People Looking for Wealth Protection and Legacy Planning– A LIRP offers both life insurance protection and the opportunity to grow wealth. A LIRP can be an excellent solution for those who want to leave a financial legacy for their heirs while supplementing their retirement income.

- Individuals Looking for Tax Diversification– LIRPs provide tax-deferred growth and tax-free loans. Hence, they can add tax diversification to a retirement portfolio. This is important for individuals who want to reduce their tax liability in retirement.

- Those Concerned About Market Volatility– LIRPs, especially with whole life or IUL policies, can offer a more stable option for retirement planning. Unlike stock market investments, certain life insurance policies provide guaranteed growth and downside protection. They can be attractive to risk-averse individuals.

Interesting Read – What Is An IRA: Your Essential Crash Course in Building a Robust Retirement Fund

How to Use Life Insurance for Retirement

Leveraging life insurance for retirement planning requires a clear strategy. Here’s how you can bring life insurance to your use for your retirement-

- Maximize Premium Contributions– To build significant cash value in your life insurance policy, it’s essential to contribute more than the minimum required premium. By overfunding the policy (within legal limits), you can accelerate cash value growth, ensuring that there are sufficient funds to access in retirement.

- Cash Value Accumulation – It takes time for the cash value to grow, so patience is important. Ideally, you should start your LIRP early. It gives the policy enough time to build substantial value. The longer you allow the cash value to grow without making withdrawals, the more financial flexibility you will have later.

- Get Policy Loans or Withdrawals Carefully – You can supplement your income in retirement by taking tax-free policy loans or withdrawals. Be careful when taking out loans, as they will lower the amount your beneficiaries will get in the event of your death. Carefully planning your withdrawals is essential to preventing unforeseen tax liabilities.

- Focus on Hybrid Strategies– Some individuals may choose to use life insurance in combination with other retirement accounts. This hybrid approach offers tax diversification and flexibility, allowing you to draw from various sources depending on your tax situation and income needs.

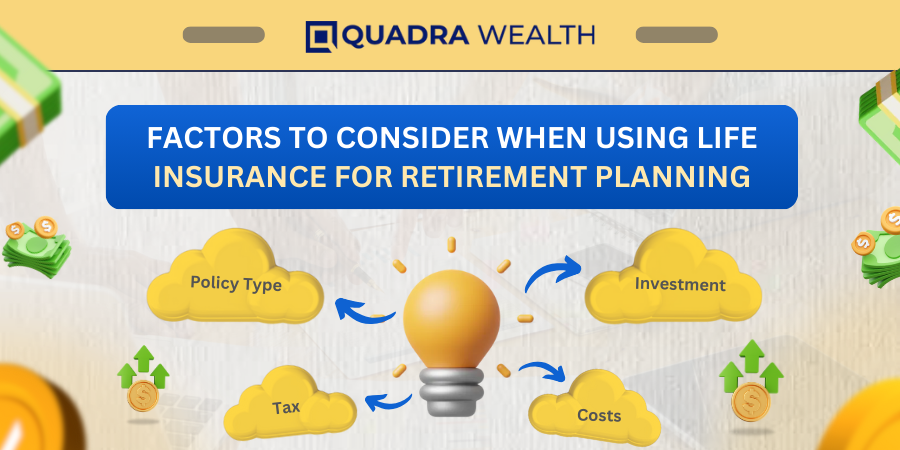

Factors To Consider When Using Life Insurance for Retirement Planning

A LIRP can be an effective retirement tool but it is essential to consider certain factors and strategies to maximize its benefits-

- Policy Type– Not all life insurance policies are created equal. Whole life offers guaranteed growth but lower potential returns, while IULs offer more growth potential but come with market-related risks. Choose a policy that aligns with your risk tolerance and financial goals.

- Costs– Permanent life insurance plans tend to be more expensive than term policies. Before committing to a LIRP make sure that you can afford the premiums and that the policy provides sufficient value.

- Tax Considerations– While policy loans are generally tax-free, they can become taxable under certain conditions (in case if the policy lapses). Make sure you understand the tax implications before withdrawing funds.

- Long-Term Commitment– Building cash value in a LIRP takes time. If you cancel the policy early or withdraw too much cash, the benefits may diminish. Be prepared to commit to the long-term strategy for the best results.

- Consult with a Financial Advisor– Life insurance is a complex financial product and retirement planning is equally nuanced. Consult with a financial advisor who specializes in life insurance and strategies for insurance to ensure you are making the best decision for your situation.

The Final Say

A Life Insurance Retirement Plan serves as a unique method of combining tax-advantaged wealth-building with life insurance protection. By understanding how LIRPs work, you can make informed decisions about adding life insurance to your retirement planning. For those who have maxed out traditional retirement accounts or are seeking additional financial security and tax diversification, a LIRP can be a valuable tool in crafting a strong retirement strategy. With proper planning and careful consideration, life insurance may be able to serve not only as a means to protect your family but also as a powerful resource to help ensure a comfortable and secure retirement.