In This Article

What Is An IRA: Your Essential Crash Course in Building a Robust Retirement Fund

Wondering how to secure a comfortable nest egg for your golden years? Well, you’re not alone. A solution is the Individual Retirement Account (IRA), a special type of savings plan with significant tax advantages designed just for your retirement.

This article will guide you step by step through everything about IRAs – types, rules, and key benefits, ensuring that you’re fully equipped to make an informed decision. Ready to dive in? Let’s get started!

Key takeaways

● An IRA is a special account to help you save for retirement. It has tax benefits that help your money grow faster.

● There are five types of IRAs: Traditional, Roth, SEP, SIMPLE, and Rollover. Each type has its own rules about how much money you can put in each year and when you can take out the money.

● The amount of money you can add to an IRA each year has limits. These limits change every few years.

● Starting an IRA is easy! You just choose where to open it, decide on the type (Roth or traditional), fill out some forms, and start saving!

● Remember not to take out your savings too soon or else there could be extra taxes or fees.

Key Functions of an IRA

An IRA, or Individual Retirement Account, is a tax-advantaged investment account designed to help individuals save for their retirement. The primary function of an IRA is to provide a way for people to set aside money for the future while enjoying some significant tax benefit in the present.

Understanding how IRAs work and what counts as income for IRS purposes can be crucial in maximizing these benefits. Whether you’re self-employed or participate in an employer-sponsored 401(k) plan, learning about this financial tool can contribute greatly towards achieving your retirement savings goals.

How IRAs Work

An IRA is a special bank account you set up to save for the time when you stop working. You put money in it each year. Some IRAs let you lower the amount of tax you have to pay now on the money you earn.

Others let their savings grow without having to pay taxes on them until later when you take out the money. The bank or investment company where you open your IRA will help choose how they use your money to try and make more money, like buying parts of companies (stocks) or lending it out with interest (bonds).

But there are rules about how much money you can put in each year, and taking out this saved-up money too soon can mean extra taxes or fees.

What Counts as Income for IRAs

The money you make from working counts as income for IRAs. This is called earned income. It includes wages, tips, and pay from freelance jobs. Money from real estate or stock sales does not count.

Only money you work to get can be put into an IRA. Self-employed people can also put their net earnings in an IRA. This rule helps ensure that the money in these accounts comes from work done by the account owner.

Different Types of IRAs

This section explores the various types of Individual Retirement Accounts (IRAs), including Traditional and Roth IRAs popular among individual savers, Simplified Employee Pension (SEP) and Savings Incentive Match Plans for Employees (SIMPLE) IRAs favored by self-employed people and small business owners, as well as Rollover IRAs that allow individuals to transfer funds from their employer-sponsored accounts such as 401(k)s or 403(b)s.

Traditional IRA

A Traditional IRA is a way to save money for when you stop working. You can put some of your pay into this account every year. The good part is, the money you put in cuts down on your taxes now.

But there’s a catch – if you take the money out before you turn 59 and a half years old, you have to pay more taxes and fees. Also, how much tax cut you get depends on how much money you make per year and if your job has its own retirement plan or not.

Roth IRA

A Roth IRA is a kind of Individual Retirement Account (IRA). You put post-tax money into it. This means you pay taxes now, not later when you take the money out. There are rules about who can have a Roth IRA and how much money they can put in each year.

The amount of tax-free money you can save for your retirement depends on these rules. If you try to take out the money before turning 59½ years old, there may be a tax penalty. But unlike other IRAs, with a Roth IRA, there is no rule that says you must start taking out the money at a certain age.

SEP (Simplified Employee Pension) IRA

A SEP IRA stands for Simplified Employee Pension Individual Retirement Account. It’s a great choice for small business owners and self-employed people. You can save more money on it because it has high limits on how much you can put in.

In 2022, the most you can put in is 25% of what you earn or $61,000, whichever is less.

Small business owners are the ones who set up this kind of account. They do this for their workers but the workers cannot put their own money into it. The good news is that when the boss puts money into a SEP IRA, they don’t have to pay tax on that part of their earned income.

So, both they and their workers win.

SIMPLE (Savings Incentive Match Plan for Employees) IRA

A SIMPLE IRA helps employees and employers save for retirement. Both can put money in this account. Workers can add up to $14,000 in 2022 and $15,500 in 2023. They do not pay tax on this money until they take it out at retirement.

Employers also have two ways to put money here. They match what the worker puts in or give a fixed amount each year. Yet, you cannot put as much into a SIMPLE IRA as other IRAs let you.

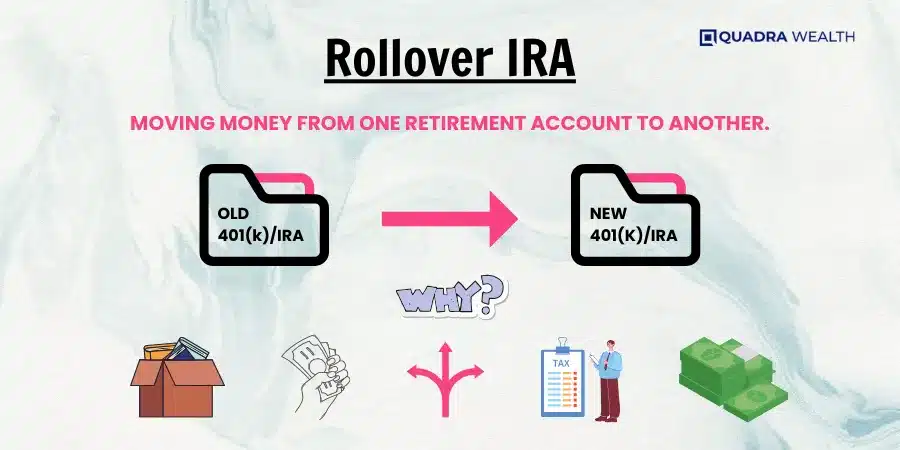

Rollover IRA

A Rollover IRA helps you move your money from an old job’s retirement plan. This can be a 401(k) or a 403(b). You put the money into the Rollover IRA. Doing this does not make you pay extra taxes right away.

Also, it saves you from fines for taking out your money early. This type of IRA has no limits on how much income you make or how much money you can move in. The good part is that there are many ways to invest with a Rollover IRA.

But do note, that any money moved into this account is not tax-free when withdrawn in the future.

Rules and Contribution Limits for IRAs

Understanding IRA rules and contribution limits is crucial to optimizing your retirement savings. We delve into the specifics of the 2022 and 2023 contribution caps, explain the wash-sale rule with its implications on IRAs, and shed light on the concept of Required Minimum Distributions (RMDs).

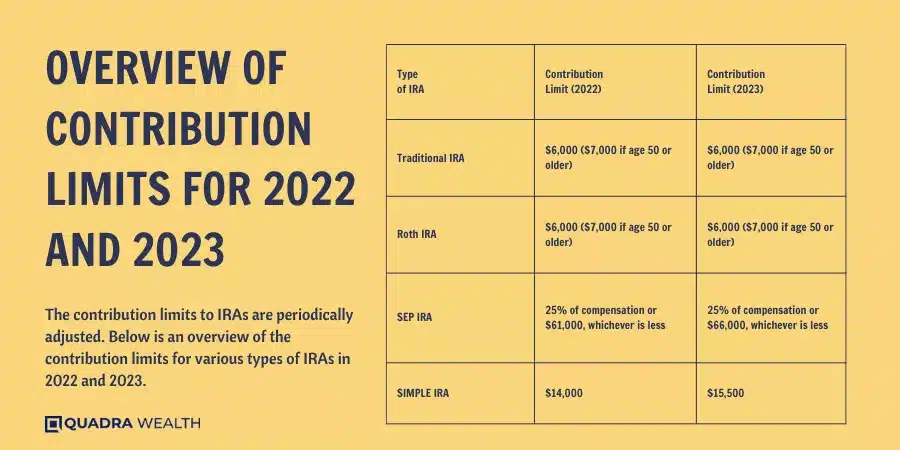

Overview of Contribution Limits for 2022 and 2023

The contribution limits to IRAs are periodically adjusted. Below is an overview of the contribution limits for various types of IRAs in 2022 and 2023.

Type of IRA | Contribution Limit (2022) | Contribution Limit (2023) |

Traditional IRA | $6,000 ($7,000 if age 50 or older) | $6,000 ($7,000 if age 50 or older) |

Roth IRA | $6,000 ($7,000 if age 50 or older) | $6,000 ($7,000 if age 50 or older) |

SEP IRA | 25% of compensation or $61,000, whichever is less | 25% of compensation or $66,000, whichever is less |

SIMPLE IRA | $14,000 | $15,500 |

The above limits apply to the total contributions made to all your Traditional and Roth IRAs in the respective years. Please note that income limits for Roth IRAs depend on your Modified Adjusted Gross Income (MAGI), which can impact your eligibility for contributions.

Understanding the Wash-Sale Rule and IRAs

The wash-sale rule links to IRAs. This rule stops people from using losses on taxes in a tricky way. If you sell an IRA investment for less money than you paid, and then buy it again soon after, that’s a wash sale.

You can’t use the loss to lower your taxes.

It is key to know about the wash-sale rule if you have an IRA account. It helps make sure we use our retirement savings well and take full advantage of tax benefits.

Explanation of Required Minimum Distributions (RMDs)

RMDs are sums you take out of your IRA each year. In most cases, people aged 72 and older must use RMDs. But starting in 2023, this rule changes to include people who turn 73. You need to take the money out by December 31st every year.

If you have a Roth account, the rules are different. You do not need to take RMDs from these accounts at all! This can make Roth accounts a great option for many folks planning their retirement savings strategies.

Advantages of an IRA

The IRA offers tax advantages that boost your retirement savings, with diverse types of IRAs suitable for different financial situations. You can choose between options like Traditional and Roth IRAs, each with its own unique benefits.

High earners or self-employed people may further benefit from SEP and SIMPLE IRA structures. Additionally, the flexibility of managing your investment decisions in an IRA favors diligent savers who want to diversify their retirement assets across various channels such as mutual funds or ETFs.

Lastly, maintaining an IRA can supplement employer-sponsored plans like a 401(k), helping maximize your tax-advantaged investment growth for a comfortable nest egg during your golden years.

Comparing IRA Options

There are several Individual Retirement Account options, each with its own set of rules and benefits. Here’s a comparison of these options in an easy-to-understand format:

Type of IRA | Income Limitations | Early Withdrawal | Minimum Distributions | Tax Advantages |

Traditional IRA | Yes, for deductible contributions | 10% penalty before age 59½ | Required from age 73 | Tax-deductible contributions, taxed distributions |

Roth IRA | Yes, for contributions | Subject to conditions | None required | No tax deductions, but tax-free distributions |

SEP IRA | No | 10% penalty before age 59½ | Required from age 73 | Contributions limit up to 25% of compensation |

SIMPLE IRA | No | 10% penalty before age 59½, with additional conditions | Required from age 73 | Both employees and employers can make contributions |

Understanding the difference between these IRAs can help individuals make informed decisions when planning for their retirement.

Benefits of an IRA for Retirement Savings

An IRA helps grow your money for retirement. It has perks that save you after-tax dollars too. You put less taxed or untaxed money into this account. The funds gain value over time without any tax deductible on the growth each year.

This lets your savings multiply faster than in a normal savings account. With Roth IRA contributions, you won’t pay taxes when you take out your money after retiring at 59 and a half years old or later.

This means all the cash is yours to enjoy!

The Process of Starting an IRA

Starting an IRA involves a series of steps, starting with choosing between a Roth or Traditional IRA contribution. This process also requires careful consideration of other factors including understanding the differences between a 401(k) and an IRA to make informed decisions about retirement saving.

Steps to Start a Roth IRA or a Traditional IRA

You can start an IRA at a bank or online. Here are the steps:

- Choose where to open your IRA. You can use a bank, credit union, or online broker.

- Decide which type of IRA you want to start: traditional or Roth IRA.

- Fill out the forms with your personal and financial information.

- Agree on how much you want to put into the account.

- Based on your income, decide if you want to make tax-deductible contributions.

- Start putting money in! Watch it grow over time.

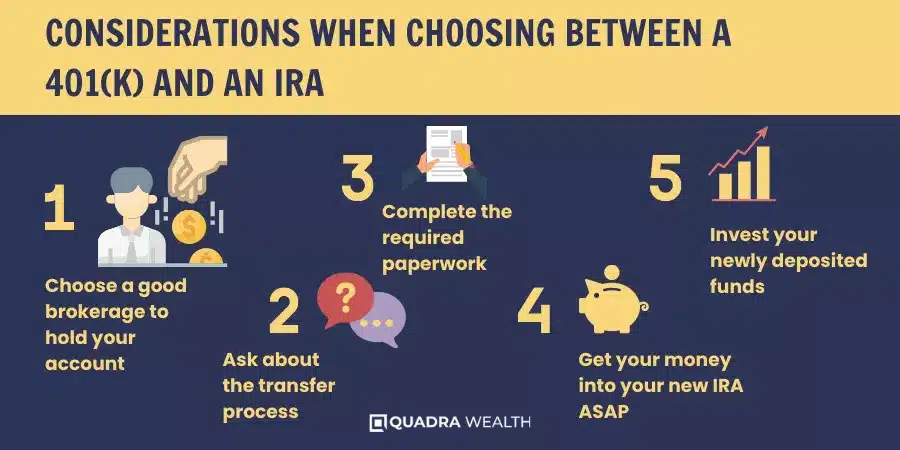

Considerations When Choosing Between a 401(k) and an IRA

Picking between a 401(k) and an IRA is not easy. Look at what your boss offers first. Next, check how much you can put into each plan. You might have more choices in investments with an IRA than a 401(k).

Think about the tax benefits too. A traditional IRA might let you deduct money now on taxes, but you pay later when you take money out. With a Roth IRA or 401(k), there are no deductions now but you get to take both your savings and gains out later tax-free.

Conclusion

Individual Retirement Accounts (IRAs) are invaluable tools for securing your financial future during retirement. This article has offered a comprehensive guide about what is an IRA and the various IRA types, rules, and benefits. IRAs offer tax advantages, enabling your savings to grow more efficiently. Whether you choose a Traditional or Roth IRA or opt for specialized options like SEP or SIMPLE IRAs, careful planning is essential. The flexibility and potential for tax-free distributions make IRAs a vital component of your retirement strategy. Remember, it’s never too early or too late to embark on the path to a secure and comfortable retirement through an IRA.

IRAs are smart ways to save money for when you stop working. They come in different types and have tax perks. You can start an IRA with any job that pays you. It’s never too early or too late to begin saving for your future!

FAQs

An IRA is a savings account that lets you set aside money for retirement. You can put your money in investment options like exchange-traded funds (ETFs) to help it grow.

Yes, Traditional IRAs and Simplified Employee Pension (SEP) IRAs are two examples. The type you pick depends on your financial goals and income eligibility limitations.

With traditional IRAs, the money you put in may be tax-deductible contributions which means they lower your tax bill now. But when you take out the money later, then it gets taxed.

Yes, there are limits called IRA contribution limits on both employee contributions and catch-up contributions that change each year.

If you make withdrawals before age 59½ in most cases, you will need to pay an early withdrawal penalty along with ordinary income tax.

Yes! A process called 401(k) and 403(b) rollovers allows moving funds from employer-sponsored accounts into an IRA.

Why You Need a Personal Financial Manager?

Personal finance management (PFM) is not confined to budgeting and investment any longer. There are

Nearing Retirement Advice for a Secure Future

Nearing retirement advice? A plan for retirement is essential to enjoy a happy healthy life

What is Debt Ceiling? A Complete Guide for Beginners

What is Debt Ceiling? Debt Ceiling, also known as the debt limit, is the highest

Is It Possible to Have No Debt?

Debt is often considered the norm in the corporate world, but the debt free companies