Introduction

These notes primarily underlie capital-protected investment products such as corporate bonds, government bonds, and fixed-income securities to predominantly protect investors’ initial investment amounts.

These notes are slightly higher priced as the notes protect the principal value of the investors by a greater extent.

On this parlance, let us discover more interesting Features, Benefits, And Risks For PPNs. Helping you get started further on the concept:

What are the primary Features of PPNs?

These are the primary features that are associated with PPNs. Helping you through with a rundown into the same:

Meaning and conceptual understanding of PPNs

The notes are specifically linked to capital-protected assets like government bonds, municipal corporation bonds, corporate bonds, or a basket of fixed-income securities.

The assets take a safer-bet allocation here to protect the capital investment of investors on the whole. However, the notes may underlie broader indexes of equities or the S&P 500 to help investors get higher returns on these investment portfolios.

At the end of the tenor period, the investors are guaranteed 100 percent of their principal investment regardless of the performance of linked-in assets.

100 percent principal protection

PPNs provide investors with 100 percent capital protection, which is a brownie factor for traditional investors who would want to protect their capital investment on their portfolios. PPNs, therefore, highly appeal to traditional retail investors, pensioners, or retirees who invest their life-long savings into investment portfolios.

Participation in market upside

PPNs provide upside investor participation to capital-protected products. These include mortgage bonds, capital bonds, municipal corporation bonds, fixed income securities, and S&P indexes. The PPNs, therefore, provide a certain degree of upside protection on capital-safe investment assets and help them see their portfolios grow on a long-term level.

Has a debt component to the structural outlay of PPNs

PPNs have a dual structural outlay like any other form of structured notes. The first component is a debt structure that provides an overall downside protection and a layer of risk mitigation to the investment capital of investors.

The other structure is the asset component, comprising bonds, fixed income securities, and capital safe equity options. This layer determines the returns of investment on the portfolio.

This is primarily because the note must comprise a debt component for capital protection, while the derivative component of the note helps the note garner market exposure.

Fixed maturity periods for PPNs

PPNs have fixed maturity periods or tenor periods, and the investors can get their capital wallet redeemed along with interest earnings that were decided at a time while the notes were being designed.

Fixed Coupon payouts

PPNs offer fixed coupon payouts, typically like traditional bonds or fixed-income securities. The coupon amounts confer through interest earnings the portfolio earns from time to time or across periodic intervals.

Investment complexity

PPNs are complex to learn or understand for newbie or amateur investors. These are structured products that underlie derivative as well as bond components. The investors, therefore, must read the offer documents carefully before investing.

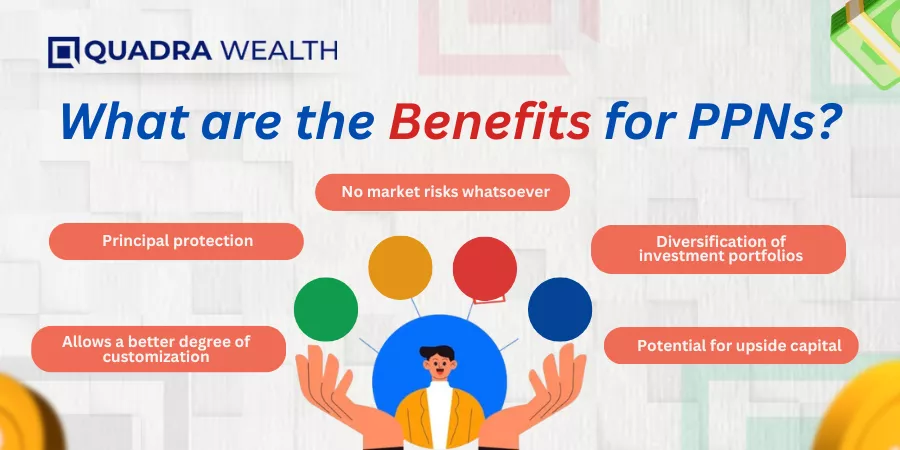

What are the Benefits for PPNs?

These are the following benefits that are pertinent for PPNs. Let us have a rundown of pointers that are connected with the same:

Principal protection

Investors get the benefit of receiving 100 percent of their capital investment or the principal investment they had invested. This is regardless of volatile market conditions. Therefore, PPNs are highly suitable for conservative or risk-averse investors.

Potential for upside capital

Investors can leverage their potential for enhanced returns as the investment portfolios get exposed to capital-protected products like bonds, fixed-income securities, and capital safe equities. This way, the returns enhanced values the investors can capitalize on over traditional bonds or fixed-income securities.

Diversification of investment portfolios

Investors get a better exposure to equities, commodities, and bonds while being able to safeguard their capital investments. You, therefore get varied exposure to different types of financial products without having the need to make direct investments into each one of them. And, you can avail a better return on your portfolios as you operate in a relatively structured and safer business environment.

No market risks whatsoever

Investors are guaranteed a 100 percent return on their capital investment regardless of how the markets perform. Therefore, this is an option that is highly favored by senior citizens, retirees, pensioners, and traditional retail investors who do not wish to lose their initial investment across financial portfolios.

Allows a better degree of customization

PPNs allow better customization on their portfolios by allowing you to include risk-free equities, fixed-income bonds, fixed-income securities, and a basket of mixed financial products that are risk-free. You get better customization to curate your investment baskets by choosing tenor periods, capped returns, or other specific dynamics of your financial portfolios.

What are the risk factors for PPNs?

These are the pertinent risk factors that one finds for PPNs. Let us have a rundown of pointers that are connected with the same:

Limited upside potential

The returns on PPNs are usually capped to a greater extent by product issuing firms on the whole. Although your principal investment is protected, you cannot encash on the entire market performance of underlying assets. Therefore, the returns you actually receive on your investment portfolio is not fully proportional to the performance of the underlying assets.

Liquidity Risk

The PPNs are not that liquid in nature. Here, the investor may have to wait until the assets mature. Therefore, the PPNs are not suitable for those investors who may want to access their funds to meet immediate family or medical emergencies. Even if you try selling the PPNs into other markets, you might incur a significant amount of losses from the money you had initially invested.

Credit risk

PPNs are at risk if the credit performance of the product-issuing firms is a potential threat. If the product issuance firms suffer liquidity issues like if they sign up for their insolvency or bankruptcy, then the PPNs would be deemed invalid or valueless. Here, the investor would not get his capital and interest earnings on the given portfolios.

Market Risk

The performance of underlying assets depends on how the initial purchase prices of linked assets hike up or exceed their values on a futuristic note. Although PPNs guarantee a 100 percent return of your capital investment, your returns on investment might be minimal if the underlying assets do not perform as expected.

The Bottom Line

PPNs are capital-protected investments that offer investors a complete return of their principal investments. However, your returns on investment might be modest and not touch potential heights. Investors must read their offer documents carefully before investing. What are your thoughts on this? Do mention it in the comments below!

Frequently Asked Questions or FAQs

Define a PPN

PPN is a principal-protected note that provides you with a 100 percent portion of your principal amount at the end of the tenor period or maturity period of ppn investments. Here, you get your principal back or can avail your principal amount at maturity regardless of the performance of the underlying assets the notes are tied to. You can also avail of lucrative tax benefits for those of you who add linked notes or ppns to your investment portfolio.

Do zero-coupon bonds appeal to risk-averse investors?

Answer: Zero-coupon bonds appeal to risk-averse investors as you buy these bonds at ‘below-par rates,’ and you can sell these bonds for at-par values. The difference in values between purchase and sale prices marks the profit margins for zero-coupon bonds. You must also look at the creditworthiness of the issuer when buying or selling zero-coupon bonds.

Can you buy bonds from a default broker or look for mutual fund companies while wanting to procure them?

Answer: It is always better that you choose a reputed wealth management firm or look for independent practitioners who would charge hourly or fee-only management fees for advisory services. This way, you would get an unbiased form of financial advice.