Introduction

Life can bring different stages of commitment or challenges that keep you on your toes. Humans have different requirements at every stage of life. Your needs in your teen phase aren’t the same when you are 40, and so they change once you reach 60. This is where understanding the wealth management life cycle becomes crucial.

As you cross the different stages of life, your financial goals and strategies should evolve accordingly to ensure long-term security and stability. This is how you cross the different stages of life.

When you look at generating a wealth basket and preserving your investment portfolio for decades, you do not expect things to fall into place overnight. It takes different stages of wealth management to see your wealth basket growing steadily. On this note, let us discover the main stages connected with the wealth management life cycle. Helping you get started here:

What is Wealth Management

Wealth management encompasses a defined set of principles that are aimed at creating wealth baskets or investment portfolios right there from scratch.

A wealth management firm or a wealth advisor guides investors into picking the right set of investments in an investment portfolio. The investment portfolio can comprise a mixed bag of financial instruments like stocks, shares, bonds, mortgage funds, exchange-traded funds or etfs, and mutual funds to name a few.

In some instances, the investors or clients give authorization to a wealth management firm or advisor to make investments on their behalf. This way, a sustainable wealth basket or income-generating basket is created for investors.

Then, the movement of how different investments perform in the market is tracked. Further to this, the wealth manager also assists their clients achieve their long-term plans:

-

Estate planning

-

Retirement planning

-

Funding of education for sons or daughters

-

Buying a dream home

-

Tax and legacy planning

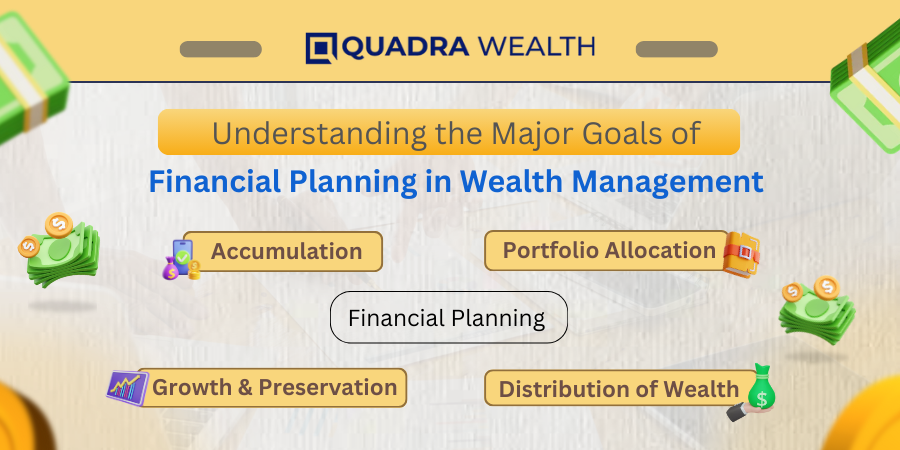

Understanding the Major Goals of Financial Planning in Wealth Management

These are the major financial goals you must aim for before you foray into following wealth management principles. Helping you through a run-down into the same:

1. Accumulation

When you are in the working phase of your life, you prepare yourself to achieve your milestones or future goals. For instance, buying a brand-new car or applying for a mortgage loan to build your dream home. At this point, a wealth advisor assesses the number of years that are left for your retirement and therefore analyzes your risk tolerance ratio. The risk tolerance ratio for every investor is unique and varies significantly from one investor to another.

2. Portfolio Allocation

Portfolio allocation is a process in which assets are distributed inside the investment portfolio diligently and precisely. Growing investments like high-paying stocks, fixed-income securities, lucrative bonds, and real estate shares that can be appreciated, are usually picked and dropped into the investment portfolio. The process is known as asset allocation or portfolio distribution.

Portfolio allocation focuses on picking the right set of investments that show growth on a short-term basis as well. Short-term investments are those types of investments that are not held inside your kitty over longer periods. Proper asset allocation ensures that your future wealth-generation objectives as well as your current financial endeavors are met simultaneously.

3. Growth and Preservation

When you have to grow your investment portfolio, you must robustly build your financial security.

Maintaining your assets calls for taking the following steps from your end and these include:

a. improving the stability of your investment portfolio

b. minimizing interest-rate fluctuations or other volatilities concerning the market

c. helping investments enhance their growth rates or replacing not well-to-do investments with better-performing investment options and finally

d. protecting your investments against taxation or inflation

Therefore, you need a wealth manager who oversees the above norms and takes necessary steps to keep your investment portfolio on a growing pace, preserve the investments, and retain their net asset values at the best level possible.

4. Distribution of Wealth or Finances in a Prudent Manner

Above all, the last goal in financial planning is the distribution of your assets amongst clients, investors, and stakeholders equally. Prudent distribution of income and wealth is required to help economies grow or evolve on a steady or prosperous note.

This way, you work towards helping economies grow and contribute to expanded GDP levels of developing economies. This way, the purchasing power of your people improves and you help growing economies advance further.

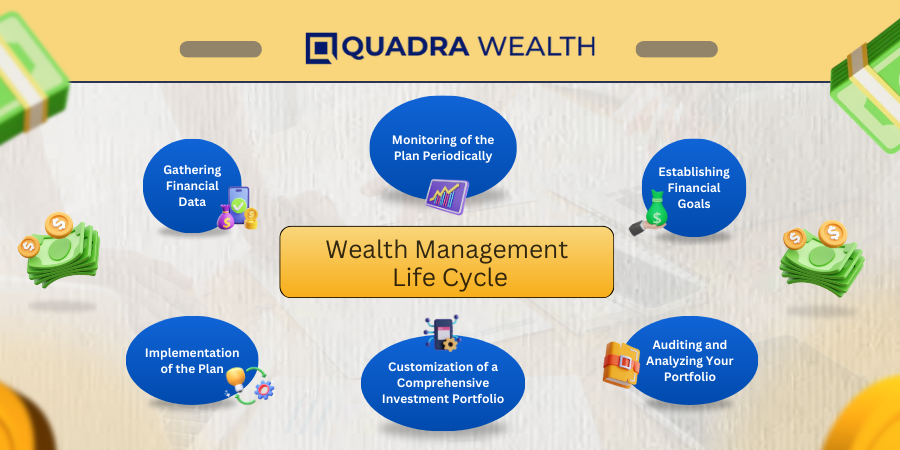

Wealth Management Life Cycle- The Different Stages as Explained

To pursue financial planning goals and objectives, these are the 6 stages the wealth management life cycle goes through. Helping you through a run-down of pointers connected with the same:

1. Gathering Financial Data

This is your first stage in a robust wealth management plan. You approach a wealth management firm or get in touch with a private wealth advisor who is a practitioner catering to independent clients.

You can establish a reasonably convenient virtual call or a meeting with a wealth manager. Otherwise, you walk down to the office of a wealth management firm.

Here, you have a tete-a-tete discussion with a wealth manager or an investment advisor. You discuss what your financial objectives are and what kind of investment options can you pick and drop into your investment portfolio or wealth basket. The wealth manager further assesses what your risk tolerance is and does the risk profiling for you to take it forward to the next step.

2. Establishing Financial Goals

Now is the time to reinforce your goal-setting process. You prepare a goal sheet vis-a-vis an assessment of your financial goals with the wealth manager at your disposal.

Here, you provide vital and critical information to your wealth manager. The info you provide must be about:

a. the current finances you have at the moment

b. a fair-view statement on the emergency contingencies you have at the moment and

c. your overall level of risk tolerance

To assess each of the above, you may have to provide your recent bank statements, investments, and insurance-related info to your wealth manager or financial advisor.

This way, your wealth manager evaluates your portfolio vis-a-vis the risk you are capable of handling at the moment. This is a crucial stage of your wealth management process.

3. Customization of a Comprehensive Investment Portfolio

Once your wealth manager takes relevant documents from you, the next main step involved with the wealth management life cycle is to build a comprehensive investment portfolio that meets the financial obligations of the client-investor.

Tailor-made or customized solutions are made to achieve the immediate financial goals of the investor vis-a-vis looking into the long-term financial planning for the investor such as retirement or tax planning.

Diversified investment baskets comprising stocks, shares, a basket of bonds, mutual funds, and real-estate mortgages will be chosen per the same. This way, you maximize your savings and returns on investment.

4. Auditing and Analyzing Your Portfolio

Once you give all the inputs from your side, the wealth manager builds a customized investment portfolio that provides you with a steady rate of returns while helping the wealth or investment portfolio grow in an even-paced manner.

The wealth manager must then periodically assess, analyze, and audit your portfolios from time to time. He should rebalance your investment portfolios by dishing out investments that are no longer doing well and replacing those investments with greener options. Therefore, constant auditing and analysis of your investment portfolio must be done so that your wealth basket remains intact and does not deteriorate.

5. Implementation of the Plan

Once your investment portfolios stand analyzed, the wealth manager further moves on to build customized solutions that aim at long-term financial planning. He generates robust plans aimed at retirement or estate planning resolutions.

Investment portfolios are further worked into to arrive at tangible rates of return from wealth baskets that stand curated or customized in the name of the investor and this paves the way to the growth and propensity of healthy investment portfolios.

6. Monitoring of the Plan Periodically

This is the last stage in a wealth management life cycle. In this step, you might have to schedule regular meetings with your wealth manager to see how your investment portfolios are faring against market conditions.

You can further discuss if your investment portfolio is moving in the direction it is supposed to move in. Above all, you can also discuss tax implications with your wealth manager to further assess the returns of income you get from your portfolio.

Suggested Reads: Difference between financial planning and wealth management

The Bottom Line

You must make sure financial planning is done years ahead of you so that you build the base and foundation of a sustainable lifestyle.

By creating wealth baskets, you not only fulfill your immediate financial obligations but also aim for long-term financial goals such as retirement or tax planning.

This way, you achieve financial freedom and can lead a stress-free life for years to come.

What are your thoughts on this? Do let us know in the comments below!