Finding the right investment option depends on liquidity or the ease with which the entire investment can be turned into cash without suffering a significant loss in value. Structured notes may have varying levels of liquidity, and principal-protected structured notes stand out for those prioritizing safety. These notes ensure that investors receive at least their original investment back, making them ideal for risk-averse individuals. This makes principal-protected notes particularly attractive to investors who want both security and personalized returns.

Having said that investors should also be aware of the liquidity limitation that comes with principal-protected structured notes. According to financial experts and gurus- the liquidity can be narrow compared to other investments. More on this in the later section but first let’s understand the liquidity in structured notes.

The Role of Liquidity in Structured Notes

It is necessary to understand the basics of structured notes before learning about the role that liquidity plays in structured products. These financial products are hybrid securities. They combine derivative elements with more conventional fixed-income assets like bonds. Structured notes provide customized returns of principal according to the market conditions. They are also linked to the performance of assets like stocks, indexes, commodities, or currencies.

Liquidity is highly important in asset investment. Unlike traditional financial products, the liquidity of structured notes is subject to significant fluctuations depending on various factors. The underlying asset’s characteristics, the note’s intrinsic design, and the stability or volatility of the secondary market where these instruments are traded are some of these.

In simple words, with liquidity in the structured notes the investors can effortlessly invest. It can be converted into cash without depreciation. Within the context of structured notes, liquidity primarily relates to how readily one can divest the note before its maturity. Structured notes come with more intricate trading challenges in comparison to other standardized financial instruments. It is because of their inherent complexity and their association with derivative instruments.

Not all structured notes are equal in terms of liquidity. The degree to which a note can be liquidated is largely dependent upon multiple factors. These include the characteristics of the underlying asset and the specific terms and conditions of the note. The existence of the active secondary market also plays a major role here. For instance, structured notes are linked to widely traded assets, such as government bonds or major stock indices. And they usually possess higher liquidity.

Certain structured notes boast a high level of liquidity, allowing them to be sold with relative ease before reaching their date of maturity. However, for investors eyeing such instruments, it is critical to gauge the liquidity profile of a structured note, particularly if they envision needing access to their capital before the note’s term concludes. Failing to account for liquidity constraints could affect one’s ability to swiftly navigate market exits. It may lead to unfavorable financial outcomes.

Importance of Liquidity

Liquidity is one of the major considerations for many investors. The ability to exit an initial investment without incurring significant losses is important in case there is a change in the market conditions. However, it is to be noted that this safety is generally only guaranteed at the note’s maturity. The structured notes allow principal protection. If an investor sells the note before maturity, the price may differ from its face value based on market liquidity. Selling liquid structured notes can lead to a significant loss if they are not handled carefully.

How Liquidity Works in Structured Notes

1. Issuance and Initial Sale

When the structured notes are issued, first they are sold to investors through brokers. They may also be sold directly through financial institutions. The issuer of the note arranges the note by combining conventional debt securities with derivatives that are linked to an underlying asset, such as the price of commodities or an index of stocks. At this point, there is usually no problem with the notes’ liquidity. Structured notes with defined maturity dates are available for purchase by investors.

However, problems with liquidity may start occurring after the first sale. Generally, the investors intend to keep the structured notes until maturity. They get gains linked to the performance of the derivative in addition to the principal return. If investors intend to sell their holdings before the note matures they must use the secondary market. This is the point at which problems with liquidity may arise.

2. Secondary Market Liquidity

It is the marketplace where the sale and purchase of previously issued financial instruments take place. Unlike publicly traded stocks, structured notes are not always easily traded in the secondary market. Some structured notes have little to no active market for trading. This lack of liquidity can create a huge challenge for individuals who want to sell their notes before maturity.

The degree of secondary market liquidity largely depends on factors such as:

- Market demand for the specific structured note

- The issuer’s reputation and financial health

- The complexity and familiarity of the underlying asset

- The market environment at the time of sale

Individuals should be careful enough when investing in structured notes, especially if there is a chance that they might need to sell before maturity. In many cases, investors may need to sell at a discount or hold the note to maturity. And it may not align with their liquidity needs.

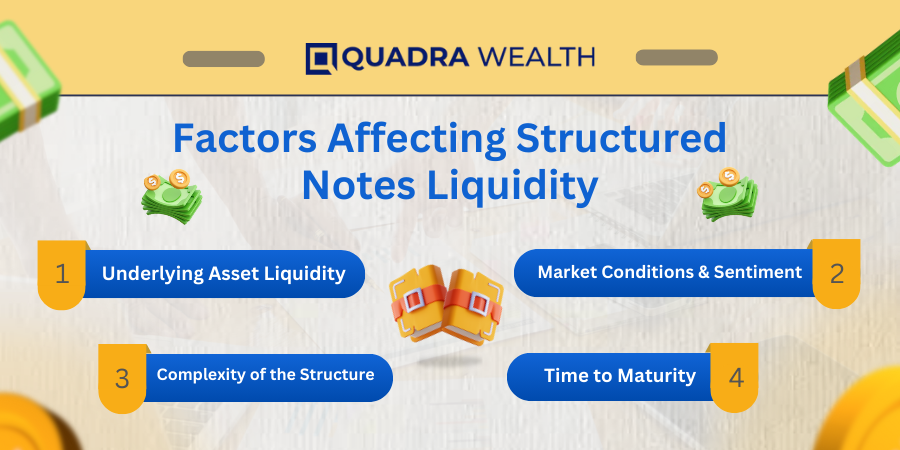

Factors Affecting Structured Notes Liquidity

Several factors impact the liquidity of structured notes, and understanding these is crucial for determining the value of the underlying and managing investment risks.

1. Underlying Asset Liquidity

The liquidity of a structured note is linked to its underlying asset liquidity. If the note is connected to a liquid asset it will likely be more liquid than a note linked to a niche commodity or exotic derivative. In other words, structured notes tied to widely traded assets tend to have more active secondary markets. This makes them easier to sell if needed.

2. Complexity of the Structure

The more complex the derivative component of a structured note, the less likely it is to have a high degree of liquidity. Notes with simpler structures such as those tied to common indices or interest rates tend to be easier to sell in secondary markets than those involving multi-asset combinations, volatile measures, or currency fluctuations. For example, a structured note linked directly to an interest rate swap will likely have better liquidity than one tied to a basket of emerging market stocks and foreign exchange options.

3. Issuer’s Financial Health and Credit Rating

The financial strength of the issuer plays a significant role in the liquidity of structured notes. Issuers with high credit ratings, strong balance sheets, and a reputable history are more likely to create highly liquid notes. On the other hand, notes from lesser-known or lower-rated issuers may face liquidity challenges. Investors should pay attention to the creditworthiness of the issuing institution. This may directly impact both the liquidity and the overall structured note value.

4. Time to Maturity

Liquidity often declines as the note approaches its maturity date. Understanding structured notes is highly important. It is to be noted that the closer the date of maturity of the note will be, the less attractive it will be to potential buyers in the secondary market. Investors buying a note close to maturity may have limited upside potential since most of the derivative’s value has already been realized. For this reason, investors looking for liquidity should plan to sell structured notes when there is still significant time before maturity.

5. Market Conditions and Sentiment

The market conditions can significantly impact the liquidity of structured notes. In times of high market volatility or economic uncertainty, investors tend to shy away from complex financial instruments, opting for safer and more liquid investments. This can lead to a decrease in demand for structured notes, making them harder to sell. Conversely, in stable or bullish markets, structured notes offer better liquidity as investors look for opportunities to capture upside returns.

Principal Protection and Its Relationship to Liquidity

One of the major things about structured notes is the principal-protection feature. It ensures that investors will receive their original investment back as long as they hold the note to maturity. And this does not count the performance of the underlying asset.

However, the principal protection feature is only guaranteed at maturity. If investors need to sell their structured note before it matures, there is the risk of losing the principal. It is due to market conditions and liquidity constraints. For example, if market demand for the structured note is low, or if the underlying asset has performed poorly, the note may sell for less than its face value.

The presence of principal-protection can also affect liquidity in both positive and negative ways:

- Positive impact: Structured notes with principal protection are often considered safer investments, attracting conservative investors who prioritize capital preservation. This can create greater demand in the secondary market, enhancing liquidity.

- Negative impact: Principal-protected type of structured notes may offer lower potential returns compared to non-protected notes. This can reduce their appeal in bullish markets. And it may result in less liquidity and payoff as investors may seek higher-yielding opportunities elsewhere.

How to Balance Liquidity and Returns in Structured Notes?

For investors, the trade-off between liquidity and returns is an important consideration when evaluating structured notes. Structured notes offer the benefit of personalizing risk levels with the potential for high returns. Structured notes that provide principal protection and downside risk mitigation generally offer lower potential returns in comparison to the ones without protection.

Investors need to carefully assess their liquidity needs and investment goals. If liquidity is a priority, it may be better to opt for structured notes with shorter maturity dates and simpler structures. If the primary goal is capital protection and long-term growth, holding the structured note until maturity may be the best strategy.

Conclusion

Liquidity is an essential consideration when investing in structured notes. While the risk associated and principal protection of these hybrid securities are similar, their liquidity varies depending on factors such as the underlying asset classes, market conditions, and the complexity of the note. Investors must be aware of the liquidity risks and weigh them against the potential rewards. Structured notes can be an excellent addition to a diversified portfolio, but understanding their liquidity profile is important to make informed investment decisions.

For investors seeking a balance between flexibility, securities exchange commission, and return potential, structured notes with well-traded underlying assets and reputable issuers may provide the ideal solution. Always consider consulting with a financial advisor to ensure your structured notes strategy aligns with your financial goals.