Introduction

With a fleet of working methodologies for each investment plan, it sometimes gets difficult to know how each investment vehicle works. As an investor, you may want to invest funds into a plan that is easy and safe to use. You need some kind of downside protection against capital losses. In other words, you do not want to lose your initial investment. At the same time, you expect decent returns from the chosen investment portfolio.

Therefore, finding a middle ground between principal protection and returns on investment becomes tough to sail on the ship.

As investors, you may be intrigued with finding the right plan that meets your specific income-generation requirements. Not many of you may be aware of structured notes barrier vs. buffer notes, which are gaining traction among sophisticated investors. Barrier notes protect your capital if the underlying asset stays above a certain level, while buffer notes offer partial protection against losses up to a limit. Both options provide a balance between protection and market-linked returns, making them worth considering in uncertain markets.

Structured notes are a mix of debt and equity. The debt component is what offers downside protection to investors and the equity gives potential opportunities for investors to receive enhanced returns on their investment portfolios. On a similar note, let us understand key points of differences covering structured notes barrier Vs buffer.

Structured notes barrier vs. buffer

Let us explore the key points of differences between the structured notes barrier and of buffer notes. Helping you understand pointers in depth:

- Definition/ Conceptual understanding between barrier notes and buffer notes

A structured barrier is a type of structured note wherein preset prices are set against the investment’s underlying assets. The product issuers gauge or monitor if the assets reach the barrier limits and the assessment of the assets is done from time to time.

The comparison values are made between the initially designed values called strike prices and the asset’s final sale point values. Here, the performance of assets is compared during an observation period or at the time of maturity of the asset.

However, when the barrier values are breached by the notes due to excessive rise or fall in the values of the asset, then the investor may lose partial or whole of his principal investment.

On the other hand, buffer notes provide downside protection to investors against incurring capital losses. A buffer limit is specified on the notes wherein the buffered portion of the asset remains protected no matter how the linked or underlying assets perform in the markets.

However, if the value of the referenced assets or stock goes below the protected buffer, the investor may lose that part of the capital investment that is not protected by the buffer and this is what the issuer states.

- Core features between the two

The prices of underlying assets may fall below or above barriers as have been set. These values are typically predetermined values that are set while the notes get curated or designed. When the price of an underlying asset goes above its initial strike price or reaches par values, then the investor gets his principal money redeemed.

On the contrary, if prices of underlying assets fall below set barriers, then the investor may lose a portion of capital investment that is not protected by the barrier notes.

Buffer notes are notes that give protection to an investor’s capital investment to the extent of the buffer coverage on the same. If the underlying assets decline within buffer coverage, then investors get their money at the time of redemption. Otherwise, their capital investment is lost to the extent of the notes that are not covered by buffers.

- Risk management

Barrier notes are meant for investors who can tackle a better degree of risk tolerance than conservative investors. This is mainly because the notes can lose their complete value if the asset doesn’t reach the barrier price. The event is also called a breach of barrier.

On the other hand, buffer notes are more applicable to traditional investors who are averse to losing their entire capital investment. As the buffers provide downside protection against capital, the investors lose only that portion of their investments that is not buffered. An increase in the value of underlying assets can help them receive potential gains on the buffered notes as well.

- Are they principal protected?

Barrier notes are not principal protected. Their potential outcomes purely depend on the performance of referenced assets that go higher up or lower down against the set barrier values. Therefore, if the assets do not reach expected values, then the investor may lose a portion of or even his entire capital money.

On the other hand, buffered notes provide a better degree of downside protection against capital investments. The buffers provide investors with protection to the extent of buffer coverage.

- Risk exposure

The possibility of asset notes going higher up or lower down barrier values cannot be estimated by product issuing firms or by investors themselves. Therefore, the volatility of market conditions impacts returns of investment for barrier notes as their values can decrease significantly with barrier breaches. Therefore, investors are exposed to a greater level of risk against fluctuating market conditions.

On the other hand, the risk exposure to buffered notes remains significantly lower. The buffered portion of investments is covered despite rising or falling prices of the assets the notes are linked to. Therefore, the significant portion of downside protection to capital favors traditional investors who may want their capital back towards maturity.

Illustration of how barrier notes work

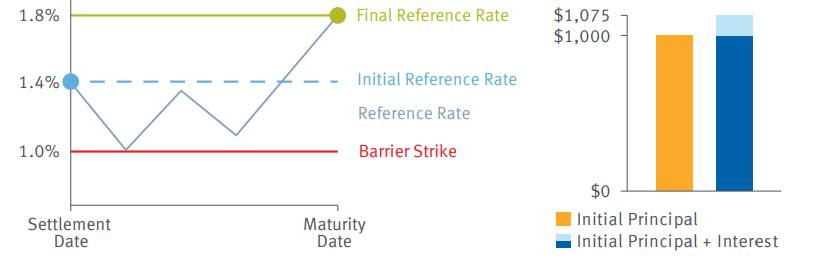

Suppose, the investor makes an initial investment of $1000. Here, the barrier strike rate is 1% and the strike rates are determined at 1.8% of the asset’s purchase value.

- Suppose the asset value goes above the barrier limit and also surpasses the initial strike prices, then we mean or imply that the asset’s performance is doing well.

The investors can get a complete value of the principal amount and coupon payouts according to the terms of the investment.

Here Principal = $1000, Coupons= $75 and the redemption amount is 1000 = 75= 1075

Note: These figures are given for illustration purposes only!

Graphical representation of the same:

Here is the graphical representation that connotes Scenario A.

Image Courtesy: https://www.googleimages.com

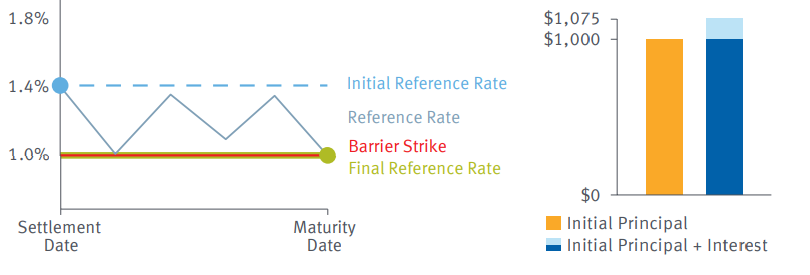

- In the 2nd scenario, the initial capital investment remains the same at $1000. However, the final strike rate of the said asset remains at 1%. This is the same as the set barrier limit. The investor still gets $1000 by the end of maturity as the strike rates have not gone below the set barrier limits. When you add specific coupon payments as well, the investor still might have received $1075 during the term of the asset.

Graphical representation of Scenario B

Image Courtesy: https://www.googleimages.com

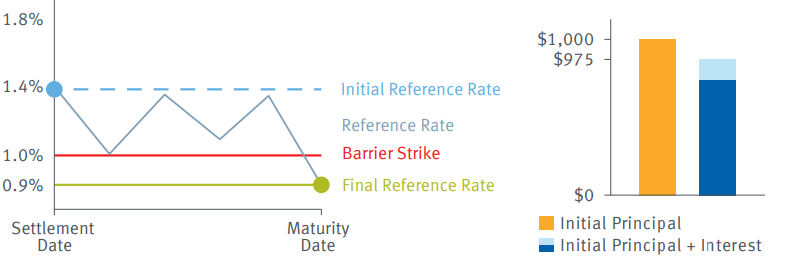

- In a third scenario, the investor has deposited $1000 into barrier notes. However, the final value of the referenced asset goes below the barrier level which stands at 1%, here the investor loses a portion of the capital.

He receives 1000 X (0.90% / 1%) = $900

Here, the investor receives only $900 towards the end of the term.

A graphical representation of Scenario C

Image Courtesy: https://www.googleimages.com

Illustration on how buffer notes work

- The initial price of a buffer note = $10

- The note is linked to XYZ asset

- Term of the asset= 2 years

- Buffer percentage = 10%, Maximum returns of 30% and Leverage factor of 300%

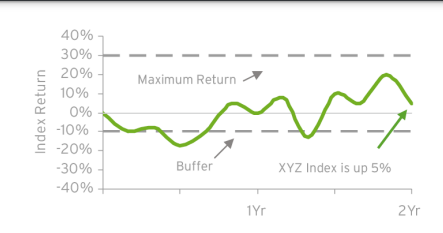

Scenario a: Here the index XYZ shows an upward trend at maturity. And, the return of the index multiplied by the leverage factor is not more than the maximum returns on investment. In this case, the investor receives $ 11.50 which is 5% of leveraged 300%.

Here is the graphical representation of the same:

Image Courtesy: https://www.googleimages.com

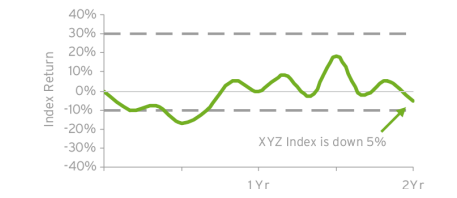

Scenario b: The value of the initial investment remains at $10 per buffer note. The indexed value of the asset at maturity does not show an increasing figure. At the same time, the index down is not more than the buffer amount. Here, the investor just receives $10 by the time of maturity.

Here is a graphical representation of the same:

Image Courtesy: https://www.googleimages.com

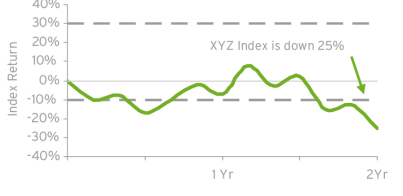

Scenario c- The index value is lower at the time of maturity and the index is also down by more than the buffer amount. Here, the investor receives $8.50. The buffer note has the index value reduced by 25% while the buffer against losses stands at 10%. Therefore, the investor loses 15% of his initial capital sum.

Here is the graphical representation of the same:

Image Courtesy: https://www.googleimages.com

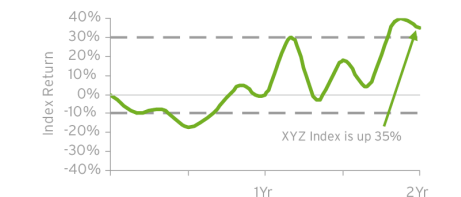

Scenario d- The index values hike by maturity and the value of the index multiplied by the leverage factor exceeds the buffer amount. Therefore, the investor receives $13 by the time the investment matures. Capital returns plus 30% of investment= $10 + $3= $13.

Image Courtesy: https://www.googleimages.com

Key takeaways between barrier and buffer notes

- Both barrier and buffer notes are structured products that provide some kind of downward protection against investment erosion.

- The notes comprise debt and equity-based underlying assets. The asset allocation can be a security, a high-paying currency, or an option-based derivative.

- The liquidity of the notes can also vary significantly in the primary or the secondary market.

- The capital investment or cap values decline when the underlying asset or commodity does not perform well in the market.

The bottom line

Structured products come to you with their pros and cons. The linked-in value of market assets plays a vital role in determining the returns of the notes that may fetch gains or inevitable losses to the investors. In other words, the structured notes may be principal-protected or come to you with partial principal protection.

Therefore, the principal risk is always on the cards. The overall index values are considered while the investment portfolios are not tracked by the hour the way the equities are dealt with.

Therefore, these investments may offer full principal by the maturity date or they may not. Some of the products offer dividend or coupon payments when held to maturity. The creditworthiness of the company also plays a role in the return of capital with earnings.

By reading about market risks comprising of terms and conditions, the investor may sign on the dotted lines.