If you’re seeking to understand “What is the fee for wealth management?”, this comprehensive guide is for you. It’s crucial to grasp the dynamics of financial advisor costs, as they can significantly impact your net returns and overall financial situation.

We’ll delve into factors influencing these advisory fees, from portfolio size to the level of service provided by certified financial planners. We’ll also discuss different types of advisors and their average cost implications.

Furthermore, we’ll explore alternative fee structures such as flat fees, and how they compare with percentage-based charges. You’ll learn about passive investing strategies that could lower your expense ratios and active investment approaches where fee-based advisors may add value.

The discourse will extend to modern digital solutions like robo-advisors versus traditional human advisors. Lastly, we aim to equip you with tips on negotiating better deals with your advisor, ensuring you get quality financial guidance at a reasonable cost.

So if you’ve ever wondered “What is the fee for wealth management?”, keep reading for an in-depth analysis tailored specifically for high-net-worth clients in UAE including expatriates at the CXO level.

How much are Wealth Management Fees?

The cost of wealth management services can vary significantly depending on the type of financial advisor and their fee structure. In 2023, the average fee for an advisor’s services was approximately 1.02% of assets under management (AUM).

However, this percentage can fluctuate based on factors such as your total investable assets and the complexity of your financial planning needs.

Factors Influencing Wealth Management Fees

A variety of elements come into play when determining how much you’ll pay in investment management fees. These include:

- Total Assets: The amount invested plays a significant role in determining advisory fees. Typically, high-net-worth clients with larger portfolio sizes may be able to negotiate lower AUM fees.

- Type Of Advisor: Fee-only advisors usually charge a flat or hourly rate for their investment advice, while fee-based advisors might also earn commissions from selling certain financial products.

- Included Services: Comprehensive financial plans that cover investment management along with other aspects like retirement planning or estate planning could have higher costs than basic investment guidance alone.

Average Costs For Different Types Of Financial Advisors

The average cost for different types of advisors varies greatly due to differences in service offerings and payment structures. Here is an overview:

- Certified Financial Planners typically charge between $1,500 – $2,500 for creating a comprehensive plan but may also offer ongoing advisory services at additional financial advisor costs.

- Fees paid to Robo-Advisors are generally low ranging from 0.25% – 0.50% per year since they mainly use exchange-traded funds (ETFs) which carry lower expense ratios compared to mutual funds.

- A registered investment advisor who actively manages portfolios by buying/selling securities frequently will likely have higher transaction costs associated thus charging more than those adopting passive strategies.

To ensure you’re getting value for money spent on these charges, it’s important to understand what each type offers before making any decisions regarding whom to entrust to manage personal finance effectively towards achieving desired goals without undue stress over unnecessary expenses incurred during the process itself.

Key takeaways

Wealth management fees can vary based on factors such as total assets, type of advisor, and included services. In 2023, the average fee for a financial advisor's services was around 1.02% of AUM. Different types of advisors have different payment structures and service offerings that affect their costs, so it's important to understand what each offers before making any decisions about managing personal finance effectively towards achieving desired goals without undue stress over unnecessary expenses incurred during the process itself.

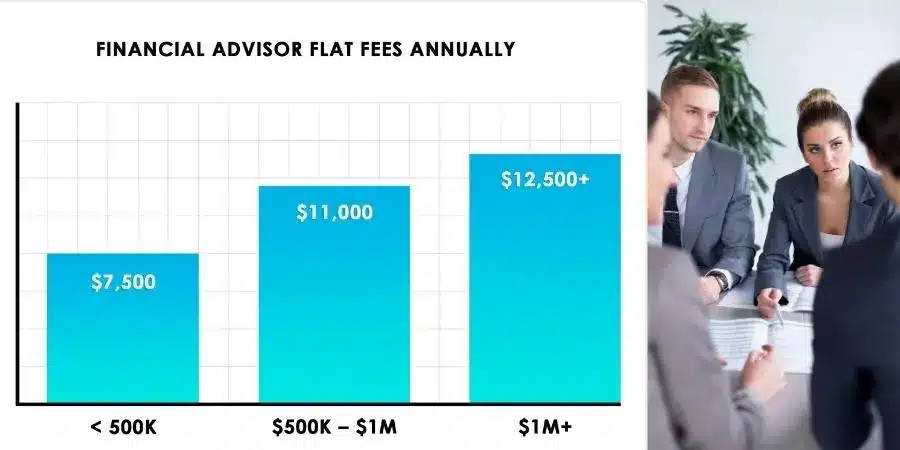

Considering Flat Fees Structure

The realm of financial counsel may be intricate, with distinct advisors charging varying prices for their offerings.

One option that is becoming increasingly popular among high-net-worth clients is the flat fee structure.

Benefits of Flat Fees

A flat fee structure offers transparency and predictability. Under a flat fee structure, you can easily budget for the same amount of payment to your advisor each year regardless of portfolio size or performance.

This means no surprise costs at the end of the year and more control over your budgeting process. In addition, this type of arrangement often aligns better with client interests than other compensation models do.

With a flat fee, advisors have no incentive to recommend certain financial products based on commissions they might receive from third parties. Instead, their sole focus becomes providing sound financial guidance tailored to meet individual client needs.

Comparing Flat Fees vs Percentage-Based Ones

If we consider an example where an investor has $1 million in investable assets and opts for an advisor who charges 1% AUM fees annually – this would mean paying out $10k per annum as advisory fees alone. However, if this same investor were to opt for a certified financial planner offering comprehensive wealth management services at a fixed annual rate of around $5k-$7k – it’s easy to see why many are considering switching over.

Bear in mind though that not all investment situations are alike; factors such as total assets invested or complexity involved could influence which model works best for you personally so always ensure thorough research before making any decisions regarding your finances.

Finding The Right Financial Advisor For Your Needs

To make sure you get value-for-money service from your chosen profession while also keeping within budget constraints set by yourself initially during consultation meetings held prior to hiring them full-time basis remember these key points:

- Evaluate Your Financial Situation: Understand what kind of investments are needed given current state affairs plus future goals aimed towards achieving eventually then discuss possible strategies together with potential candidates interviewed thus far along the journey seeking the perfect match amongst sea options available in today’s marketplace;

- Negotiate Lower Fees: Don’t shy away from negotiating lower rates especially when dealing with larger sums of money since even slight reductions in percentage terms translate into significant savings long run;

Key takeaways

The article discusses the benefits of a flat fee structure in wealth management, which offers transparency and predictability for clients. It also compares flat fees to percentage-based ones, highlighting potential cost savings for investors. The importance of evaluating one's financial situation and negotiating lower fees with advisors is emphasized as well.

Passive Investment Strategy & Its Impact On Fees

Investing can be complex, but passive investing is a simple approach that can save you money. Instead of trying to beat the market through active trading, passive investors aim to mirror its performance by purchasing index funds or ETFs that track specific benchmarks.

What is Passive Investing?

Passive investing, also known as buy-and-hold or couch potato investing, focuses on minimizing buying and selling within your portfolio, reducing costs and taxes.

How Does Passive Investing Impact Wealth Management Fees?

Passive investing can significantly reduce wealth management fees. Since this method requires less work from an advisor compared to active management, it typically results in lower fees. Fewer transactions mean lower transactional costs and many advisors charge based on a percentage of AUM.

As your portfolio grows over time, you may pay less in relative terms despite potentially higher absolute dollar amounts.

- Lower Transaction Costs: With less buying and selling, there are fewer transaction costs.

- Fewer Capital Gains Taxes: By holding onto investments longer, you can reduce potential tax liabilities.

- Simplified Fee Structure: Many robo-advisors catering to passive investors offer simple fee structures based solely on AUM.

Consult a financial expert now to explore the potential advantages of passive investing and construct an approach that meets your objectives and desires for future prosperity.

Key takeaways

Passive investing can reduce wealth management fees. With fewer transactions and simplified fee structures, it's a simple approach that saves you money.

Active Management and Fee-Based Advisors

Active management, as opposed to passive investing, attempts to capitalize on short-term market fluctuations for potentially higher returns.

While a passive strategy involves the long-term holding of investments, an active approach seeks to take advantage of short-term market fluctuations.

This method carries greater risk but potentially higher rewards too.

Advantages of Active Investing

- Potential for Higher Returns: Active investing can lead to significant profits if your financial advisor is skilled at predicting market trends.

- Flexibility: Unlike passive investors who stick with their investments regardless of market conditions, active investors have the flexibility to adjust their portfolio as needed.

- Risk Management: An experienced financial adviser can help manage risks associated with volatile markets by actively adjusting your portfolio based on current economic conditions.

An important aspect of this strategy is working with fee-based advisors. Their compensation does not depend on selling certain products or strategies, unlike commission-based advisors whose income relies heavily on transaction costs and product sales.

The Role and Benefits of Using Fee-Based Financial Adviser

A fee-based advisor’s role is to provide comprehensive financial planning services that align directly with your specific needs and goals. They provide unbiased advice since they don’t earn commissions from third parties for recommending particular financial products or services. Instead, these advisors charge a set percentage (typically around 1%) based on the total AUM.

- Honest Advice: Since fee-based advisors aren’t paid through commissions from the mutual fund or other investment vehicles, they’re more likely to offer honest advice tailored specifically towards achieving high-net-worth clients’ unique financial goals.

- No Hidden Costs: You won’t be surprised by hidden fees because all charges are disclosed upfront before any work begins.

If you’re considering hiring a certified financial planner offering wealth management services under this model, remember that it’s always possible to negotiate lower fees, especially when dealing with larger amounts invested where even small reductions in expense ratios could result in substantial savings over time.

Key takeaways

Active investing can potentially lead to higher returns, flexibility in adjusting portfolios, and risk management with the help of fee-based advisors who charge a set percentage based on total AUM. These advisors provide unbiased advice and disclose all charges upfront before any work begins, making it possible for clients to negotiate lower fees especially when dealing with larger amounts invested.

Robo-Advisors Vs Online Advisors Vs Traditional Human Advisors

As investors navigate the dynamic realm of wealth management, they have a variety of choices to consider.

From robo-advisors and online advisors to traditional human advisors, each offers unique benefits and potential drawbacks. Let’s delve into these three types of financial advisory services.

Pros and Cons Between Robo-Advisors vs Online vs Traditional Human Advisors

Robo-advisors, such as Betterment, use algorithms to automate investment decisions based on your risk tolerance and financial goals.

They’re often less expensive than their human counterparts due to their low overhead costs but may lack the personal touch some investors crave.

- Low cost

- automated portfolio management

- accessible 24/7

- Limited customization

- impersonal service.

An online advisor, like Personal Capital, typically provides more personalized advice than a robo-advisor at slightly higher costs.

They offer digital tools for tracking investments but might not provide in-depth analysis or complex planning services that high-net-worth individuals require.

- More personalized advice than robo-advisors

- access to digital tools

- Higher fees compared to robo-advisors

- may not offer comprehensive planning services

A traditional human advisor, such as those at Quadra Wealth, can provide highly customized plans tailored specifically for you while building strong relationships over time, which is something machines cannot replicate.

However, they tend to charge set prices per service offered without any standardization across the industry, meaning no “normal” rate exists generally speaking regardless of how experienced or new they may be within the field.

- Highly personalized service

- relationship-based approach

- Can be more expensive

- pricing structures vary widely across the industry

The Cost Differences Among These Options?

Determining which type of advisor suits your needs best depends largely on what you value most: cost efficiency or personalized guidance.

A recent study by Investopedia found that annual fees for robo-advisor platforms average around 0.25% – 0.50% of assets under management (AUM), whereas online advisors usually charge about 1%, with traditional advisors charging up to 2%.

However, always look out for unbiased recommendations from those who only recommend products that benefit clients instead of earning themselves commissions. Third parties should also be open to negotiating better deals whenever possible if you feel like you’re paying too much for existing services.

Key takeaways

This section compares the pros and cons of robo-advisors, online advisors, and traditional human advisors in wealth management. Robo-advisors are low-cost but lack personalization, while online advisors offer more personalized advice at a slightly higher cost. Traditional human advisors provide highly customized plans with a relationship-based approach but can be more expensive with varying pricing structures across the industry. The annual fees for these options range from 0.25% to 2%, depending on the type of advisor chosen and the services offered. It is important to seek unbiased recommendations and negotiate better deals whenever possible when choosing an advisor that suits your needs best based on what you value most: cost efficiency or personalized guidance.

Negotiating Better Deals and Looking for Options

When it comes to managing your wealth, you want to ensure that the fees you’re paying for financial advisory services are justified.

As a customer, you are entitled to seek out and negotiate better deals that fit your financial requirements.

Tips on Negotiation Skills When Dealing with Advisors

Effective negotiation can help reduce costs significantly. Here are some tips:

- Understand the Fee Structure: Before negotiating, make sure you understand how vetted financial advisors charge. This could be flat fees, a percentage of assets under management (AUM), or transaction-based fees.

- Benchmarking: Compare your advisor’s fees with industry averages. Websites like AdvisoryHQ publish average financial advisor fee schedules annually.

- Demonstrate Value: Showcase the amount invested and total assets managed by them, which might give leverage during negotiations.

- Better outcomes

- Increased confidence

- Increased confidence

- Value maximization

- Disadvantageous terms

- Missed opportunities

- Limited control

- Reduced confidence

The Importance of Finding Unbiased Recommendations

An important aspect of choosing a financial advisor is ensuring they provide unbiased advice tailored towards achieving your financial goals rather than promoting specific products or strategies from which they earn commissions.

Fiduciaries, who must always prioritize their client’s interests above all else, should be sought out.

- Objective decision-making

- Trustworthy advice

- Diverse perspectives

- Mitigation of risks

- Biased information

- Limited perspective

- Potential conflicts of interest

- Increased vulnerability

Fee-Only vs Fee-Based Advisors

In this context, understanding the difference between fee-only and fee-based advisors becomes vital. Fee-only advisors only get paid through direct charges, 1% or lower fees based on AUM or flat rates, while fee-based ones may also receive commissions from third-party product providers, potentially creating conflicts of interest due to incentive structures linked with certain investment products such as mutual funds and exchange-traded funds.

If an advisor recommends a comprehensive financial plan involving multiple complex elements, including estate planning, tax strategy, etc., then higher costs might be justifiable, but always compare these against market standards before agreeing upon any terms.

Weighing Robo-Advisors Against Traditional Financial Planners

If traditional advisory services seem too expensive, consider robo-advisors offering automated investment management at much lower expense ratios because they use algorithms instead of human intervention, making them ideal candidates, especially if one prefers a passive investing approach over an active one.

However, keep in mind that while robo-advisors offer cost-effective solutions, they lack the personalized touch offered by certified human planners capable of providing customized guidance based on individual needs.

So weigh the pros and cons carefully before deciding upon a suitable option, considering investment portfolio size and other relevant factors involved within the decision-making process.

Remember, there’s no “normal” rate when it comes down to hiring professional help to manage finances. What matters most is getting quality service at a reasonable price aligned with personal circumstances, objectives, and the long run.

Hence, don’t hesitate to explore different avenues until you find the perfect match fulfilling requirements adequately without burning a hole in your pocket unnecessarily along the way.

Always stay informed and empowered throughout the journey towards achieving the desired state of financial independence, leveraging the power of knowledge and wisdom combined together effectively and efficiently possible manner ever.

Key takeaways

This section provides tips on negotiating better deals and finding unbiased vetted financial advisors to manage your wealth. It explains the difference between fee-only and fee-based advisors, as well as weighing robo-advisors against traditional planners. The key takeaway is that clients have every right to negotiate fees and find options that suit their financial situation while ensuring they receive quality service at a reasonable price aligned with personal circumstances, objectives, and the long run.

Conclusion

Understanding Wealth Management Fees in UAE:

Knowing how much wealth management fees cost is crucial for UAE residents and ex-pats at the CXO level, as fees can vary based on factors such as advisor type, investment strategy, and financial advisor’s fee structure.

Consider all factors before choosing a financial advisor, whether it’s a robo-advisor or a traditional human advisor, and negotiate better deals to get the best value for your money.

Look for unbiased recommendations and compare different types of advisors’ costs to determine which one works best for you.

FAQ

The average fee for a financial advisor’s services is between 0.50% and 1.25% of assets under management (AUM) annually, but it can vary based on factors like the complexity of your finances and location.

A one percent advisory fee could be worth it if you’re receiving comprehensive services that include investment management, estate planning, tax planning services, etc., from an experienced professional.

Wealth Management Fees can provide value in terms of personalized advice, strategic asset allocation strategies, and access to exclusive investment opportunities. US News Money