What is the role of a wealth management advisor? A wealth management advisor is a key figure in helping affluent customers and entrepreneurs secure their financial futures.

Wealth managers are certified financial planners or chartered financial analysts who provide expert advice on investment management, estate planning, retirement planning, and tax strategies.

Their comprehensive understanding of the client’s financial picture enables them to tailor personalized solutions that align with their unique needs and goals. They navigate complex domestic and international tax laws to structure investments for optimal growth while mitigating potential inheritance taxes.

In this blog post, we will delve deeper into what a wealth manager does – from providing financial advice to offering estate planning solutions. We’ll also explore additional wealth management firms that provide wealth management services such as banking services and guidance on philanthropic activities.

We will also look at the increasing trend of automated advisors versus the more traditional preference for in-person communication from advisors. Lastly, you’ll discover various compensation methods employed by these professionals.

The Role of a Wealth Management Advisor

An asset management advisor is a financial guru who helps clients with substantial assets manage their money.

They offer personalized wealth management services that cover various aspects of finance, including financial advice, estate planning, accounting, retirement solutions, and tax services.

What Does A Wealth Management Advisor Do: Expert Investment Advice

Asset management advisors are one kind of wealth advisor who typically works with high-net-worth individuals through the complex world of finance. They analyze market trends and they can help you with financial-market investment guidance on where and when to invest for maximum returns.

This involves regular monitoring of the client’s portfolio and making necessary adjustments based on changes in market conditions or the client’s personal circumstances.

- Customized investment approach

- Diversification and risk management

- Time-saving

- Emotional discipline

- Limited investment knowledge

- Increased risk

- Lack of time and resources

- Emotional biases

- Missed opportunities

Estate Planning Solutions

Estate planning is another critical area where wealth managers play a significant role. Through careful planning, they ensure that your assets will be distributed according to your wishes after death while minimizing potential inheritance taxes.

This process typically requires regular meetings between you and your advisor where updates on changes in personal circumstances or shifts in financial markets can be discussed.

- Peace of mind

- Minimize taxes and expenses

- Asset protection

- Efficient wealth transfer

- Legacy planning

- Intestate distribution

- Higher tax liabilities

- Probate delays and expenses

- Family conflicts

- Inefficient wealth transfer

Accounting Services

An asset management advisor also offers accounting services, including managing cash flow, preparing financial statements, and budget review and analysis.

These services help maintain accurate records of all transactions carried out, ensuring transparency and accountability at every stage.

- Accurate financial records

- Compliance with tax regulations

- Financial analysis and insights

- Time-saving

- Cost efficiency

- Inaccurate financial records

- Missed tax deductions and credits

- Compliance risks

- Limited financial analysis

- Time and effort-consuming

Retirement Solutions

Retirement solutions form an integral part of any comprehensive investment management plan provided by these professionals. Hence, the retirement plan must be tailored to an individual’s age, income level, and lifestyle preferences in order to secure a comfortable future.

Hence, it becomes essential to have expert guidance to navigate through the complexities involved and ensure a secure and comfortable future post-retirement period.

Learn more about retirement planning here.

Key takeaways

"Maximize your wealth potential with a personalized approach. Asset Management Advisor offers a high-level professional who manages an affluent client's wealth holistically financial advice, estate planning solutions, accounting services & retirement solutions.

- Tailored retirement plan

- Investment expertise

- Retirement income strategies

- Social Security optimization

- Ongoing monitoring and adjustments

- Uncertainty in retirement savings

- Suboptimal investment choices

- Inadequate income planning

- Missed opportunities for tax optimization

- Lack of ongoing support

Importance of Tax Strategy in Wealth Management

A significant aspect of wealth management is the development and implementation of an effective tax strategy. A well-crafted tax plan can be a key factor in protecting one’s wealth, particularly for those with a high net worth or who are business owners based in the UAE.

By comprehending complex domestic and international tax laws, wealth management advisors can guide their clients on how best to structure their investments.

Understanding Domestic and International Tax Laws

Private wealth managers with professional designations such as certified public accountants or chartered financial analysts have the expertise to navigate through intricate tax regulations both at home and abroad.

This knowledge is especially beneficial for expatriates who need advice on how foreign income might affect their overall financial situation.

The goal here is not only to grow but also to protect the client’s net worth from excessive taxation.

The right investment decisions can significantly reduce one’s liability exposure while simultaneously maximizing returns.

Choosing the right investment vehicles, such as 401(k)s, IRAs, brokerage services, or structured notes – with a comprehensive understanding of their financial implications is key to achieving optimal growth and reducing taxation.

- Compliance with tax obligations

- Tax optimization

- Avoidance of penalties and audits

- Cross-border tax considerations

- Proactive tax planning

- Non-compliance risks

- Missed tax-saving opportunities

- Increased audit risk

- Cross-border tax complications

- Inefficient tax planning

Structuring Investments for Optimal Growth

An important part of a wealth manager’s job involves advising affluent clients about structuring their investments strategically so they yield consistent growth over time without attracting unnecessary taxes.

For instance, they may recommend certain investment vehicles based on factors such as risk tolerance level, current market conditions, long-term financial goals, etc., all aimed towards achieving optimal asset growth.

This kind of personalized service requires regular meetings where updates regarding changes in personal circumstances or shifts in financial markets are discussed openly, allowing adjustments to be made promptly if necessary, ensuring the client’s portfolio continues to perform optimally despite any unexpected fluctuations in the economy.

This provides peace of mind, knowing the future is in the hands of a trusted advisor.

In addition, individual advisors often work closely with other professionals, including lawyers and accountants, to provide a holistic approach to managing a person’s financial life, which includes estate planning among other things.

This further highlights the importance of having a reliable partner by your side when it comes to dealing with sensitive matters of finance.

- Expert investment knowledge

- Diversification and risk management

- Tax-efficient investment strategies

- Long-term focus

- Ongoing monitoring and adjustments

- Lack of investment expertise

- Concentration risk

- Inefficient tax management

- Emotional decision-making

- Inadequate portfolio monitoring

Key takeaways

The asset management advisor plays a crucial role in safeguarding the assets of high-net-worth individuals and business owners by developing an effective tax planning strategy. They navigate through intricate domestic and international tax laws to make investment decisions that reduce liability exposure while maximizing returns, advising clients on structuring their investments strategically for optimal growth. Personalized service requires regular meetings with other professionals such as lawyers and accountants to provide a holistic approach to managing one's financial life, including estate planning among other things.

Estate Planning Responsibility

As a contemporary blog manager, I’m aware that estate preparation is an indispensable part of financial planning, especially for affluent persons and families.

It’s all about making sure that your assets are distributed according to your wishes while minimizing potential inheritance taxes. And who better to help you with this than an asset management advisor?

Regular Meetings Between Advisor And Client

To ensure a comprehensive estate plan, it is essential for advisors and clients to meet regularly.

These sessions provide an opportunity for updates on changes in personal circumstances or shifts in financial markets that could impact the overall plan.

Given the frequent alterations to tax laws and regulations, it’s essential to have an expert on-hand who can keep one abreast of any changes.

For expatriates residing in UAE, where local laws can be quite different from those back home, having someone who understands both domestic and international rules can make all the difference when it comes to preserving one’s wealth across generations.

- Personalized financial advice

- Goal tracking and progress assessment

- Financial education and empowerment

- Proactive planning and adjustments

- Relationship building and trust

- Lack of personalized guidance

- Limited progress tracking

- Missed opportunities and updates

- Reactive instead of proactive planning

- Limited relationship development

Mitigating Potential Inheritance Taxes

One of the main goals of estate planning is to mitigate potential inheritance taxes.

The wealth manager helps achieve this by developing investment strategies tailored to each individual client’s needs.

Taking into account the estate’s size, type of assets, and number of beneficiaries, advisors create tailored plans to help reduce potential inheritance taxes.

An effective strategy could involve setting up trusts or gifting during a lifetime to reduce the taxable value upon death, ensuring that more goes towards loved ones and less towards government coffers.

However, every situation is unique, and seeking professional advice is crucial, especially considering the complexity of the matter and the constant changes in tax laws and policies worldwide, including in the UAE.

- Expertise in tax laws

- Estate planning techniques

- Asset valuation and allocation

- Timely planning and documentation

- Ongoing tax monitoring and adjustments

- Higher tax liabilities

- Inefficient asset allocation

- Compliance risks

- Limited understanding of tax implications

- Inadequate documentation and planning

Key takeaways

The Wealth Management advisor is essential for estate planning, especially for affluent individuals and families. Regular meetings between the advisor and client are necessary to keep up with changes in personal circumstances or the financial market that could impact the overall plan. Advisors can help mitigate potential inheritance taxes by developing tailored strategies based on factors such as estate size, asset type, and number of beneficiaries.

Additional Services Offered by Financial Advisors

A wealth manager offers a wide range of services that extend beyond traditional financial planning and holistic financial advice.

These additional services, often overlooked, can significantly enhance the overall wealth management experience for clients.

Banking Services Provided by the Wealth Manager

Aside from providing financial advisory services, many private wealth managers also offer banking solutions tailored to their high-net-worth clientele.

This might include specialized deposit accounts with preferential interest rates or exclusive credit card offers. Some may even provide mortgage consulting or facilitate loans against assets held in the client’s investment portfolios.

Wealth Managers, like those at Quadra Wealth, understand that their client’s needs are unique and require bespoke solutions rather than one-size-fits-all products offered by traditional banks.

- Comprehensive financial management

- Convenience and centralization

- Holistic financial planning

- Access to specialized banking products

- Enhanced security and privacy

- Fragmented financial management

- Missed opportunities for integration

- Limited financial advice in banking decisions

- Potential for suboptimal banking products

- Reduced security and privacy controls

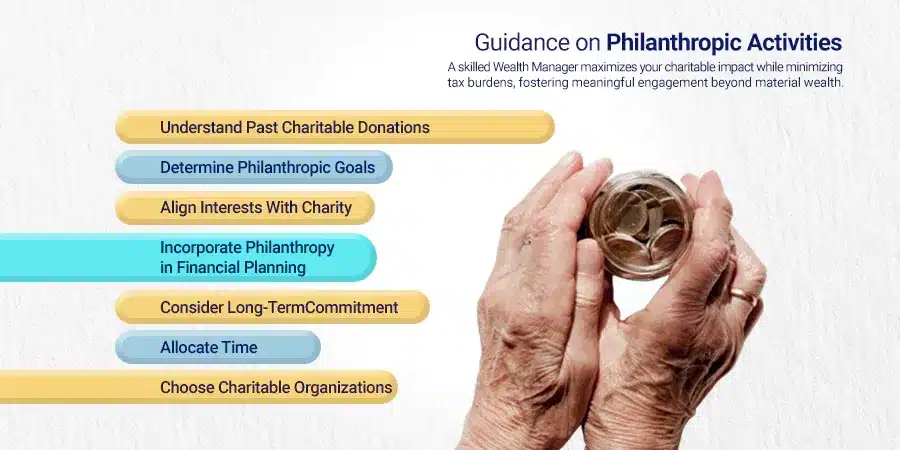

Guidance on Philanthropic Activities

Beyond just growing and preserving their fortune, many high-net-worth individuals seek to use their wealth for good causes they care about deeply.

However, effective philanthropy requires strategic planning – not only deciding which organizations align best with your values but also understanding how different types of donations (cash vs stock) can impact tax liabilities.

A knowledgeable Wealth Manager can guide you through this process, ensuring your charitable contributions have a maximum impact while minimizing potential tax implications – thus enabling meaningful engagement beyond the mere accumulation of material possessions.

Key takeaways

"The Wealth manager offers more than just financial advice. From banking solutions to philanthropic guidance, they provide bespoke services for high-net-worth clients.

- Strategic philanthropy planning

- Maximizing philanthropic impact

- Tax Advantages of Philanthropy

- Due diligence and transparency

- Legacy planning

- Lack of strategic focus

- Missed opportunities for impact

- Inefficient tax planning

- Lack of due diligence

- Incomplete legacy planning

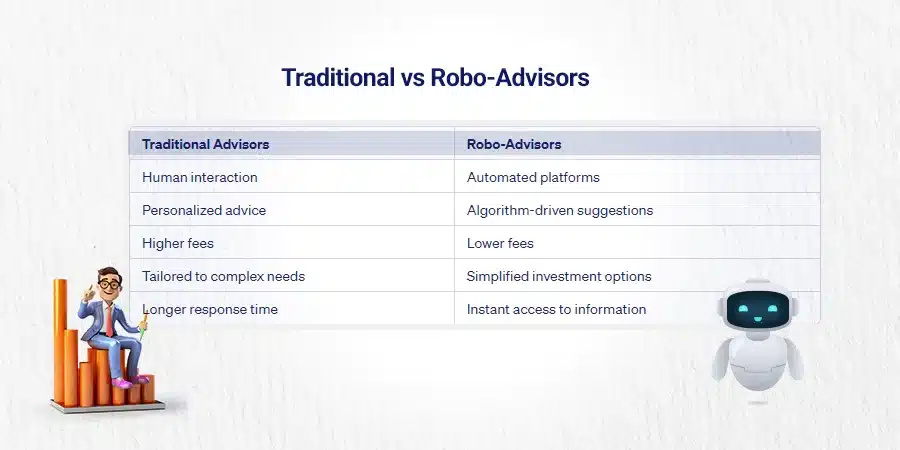

Traditional vs Robo-Advisors

The introduction of automated platforms, such as robo-advisors, has greatly changed the way people manage their finances in this digital age. These automated platforms use complex algorithms to meet individual needs without human intervention.

However, many still prefer traditional face-to-face interaction when dealing with sensitive matters like their finances.

The Rise of Robo-Advisors

Robo-advisors have gained popularity due to their efficiency and convenience. They offer 24/7 access and require minimal human interaction.

Using sophisticated algorithms, they analyze market trends and make investment decisions that align with your risk tolerance and financial goals.

Robo-advisors may be an attractive choice for those who are comfortable with technology or prefer to manage their investments digitally.

However, it’s essential to note that while robo-advisors provide algorithm-based advice tailored to your inputs about your financial situation and goals, they lack the personal touch that comes from working directly with a wealth manager.

- Accessibility and convenience

- Lower fees

- Automated investment management

- Data-driven recommendations

- Educational resources

- Lack of personalized advice

- Limited human interaction

- Inability to navigate complex situations

- Potential technology risks

- Limited emotional intelligence

The Preference for Traditional Face-To-Face Interaction

Despite advancements in technology making investing more accessible than ever before through robo-platforms, many investors continue to value traditional financial advisors for several reasons:

- Personalized Service: A traditional advisor provides personalized service tailored specifically towards each client’s unique circumstances – something not typically offered by most robot platforms.

- Detailed Financial Planning: A wealth manager doesn’t just manage investments but also offers comprehensive planning services such as retirement planning or estate planning which may not be available via a robo-platform.

- Crisis Management: In times of economic uncertainty or personal crisis situations where immediate attention is required – having someone you trust who understands your specific situation can prove invaluable compared to automated responses provided by most digital platforms.

No matter how advanced technology becomes, there will always be a need for trusted partners guiding us throughout our financial journey.

The importance of having such guidance remains paramount regardless of any technological advancements made within the field over recent years.

Whether you choose a traditional advisor or opt for a modern approach using robo-technology largely depends upon individual preferences alongside factors including the complexity involved within one’s portfolio management, and comfort level using technology, among others.

Ultimately both methods aim at achieving the same goal – helping clients grow and preserve their wealth effectively.

- Personalized guidance and advice

- Emotional support and reassurance

- Complex financial planning

- Trust and relationship building

- Flexibility and adaptability

- Higher fees

- Limited accessibility

- Potential bias and conflicts of interest

- Dependence on advisor availability

- Varying expertise and quality

Key takeaways

The article discusses the difference between traditional wealth managers and robo-advisors. While robo-advisors offer convenience and efficiency, traditional advisors provide personalized service, detailed financial planning, and crisis management during times of economic uncertainty or personal crises. Ultimately, both methods aim to help clients grow and preserve their wealth effectively based on individual preferences and portfolio complexity.

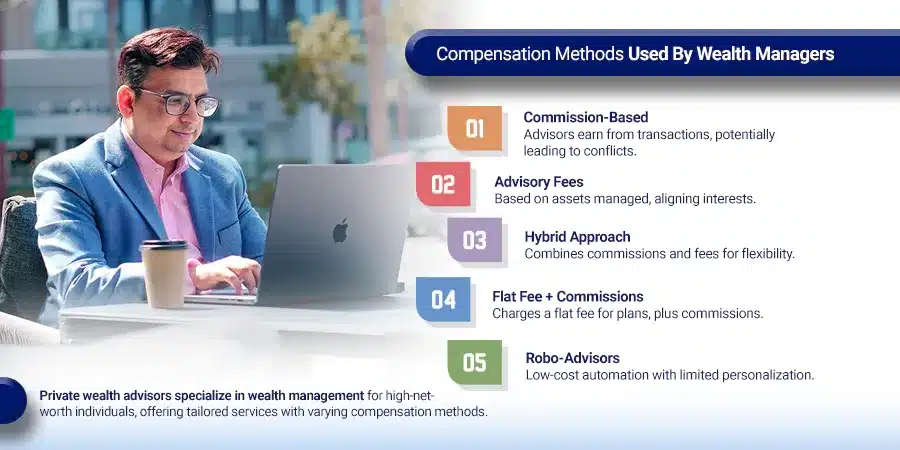

Compensation Methods Used By Wealth Managers

One kind of financial advisor who typically works with high-net-worth individuals specialized in wealth management offers a variety of services to assist wealthy individuals, affluent clients, and entrepreneurs attain their fiscal objectives.

As with any professional service, these experts charge for their expertise. However, the compensation methods used by private wealth advisors can vary widely.

Variety Of Compensation Methods Employed

The first method is through commissions on transactions carried out. This traditional approach sees individual advisors earn a percentage from each transaction they facilitate or the financial product they sell to you.

It’s common among brokerage services but has faced criticism due to potential conflicts of interest as it may incentivize advisors to recommend products that yield higher commissions rather than those best suited for your financial situation.

A second method is charging advisory fees based on a percentage of the total assets managed – often preferred by fiduciary financial advisor types such as certified public accountants (CPAs) and chartered financial analysts (CFAs).

This model aligns the interests of both parties; since the more your portfolio grows under their investment strategy guidance, the more they earn in return.

A third option some wealth managers might adopt combines both commission-based and fee-based approaches depending upon the nature and scope involved.

For instance, an private advisor might charge a flat fee for creating your financial plan, then collect commissions on specific investment decisions made within that plan.

In addition to these main models, there are other less conventional payment structures employed by certain niche providers like robo-advisors which typically offer lower costs via automation but lack personalized advice offered by human counterparts.

Finding The Right Fit For Your Needs

It’s important when seeking wealth management services not just to focus solely on the cost aspect but also to consider the value derived from the relationship established with the chosen advisor, whether it be traditional face-to-face interaction or a digital platform offering automated solutions tailored to meet the unique needs and preferences of the client.

Factors To Consider

- Evaluate Transparency: Good financial planners should clearly explain how they get paid so you understand what you’re paying for and why.

- Analyze Value: Consider if the cost matches up with what you’re getting in return – comprehensive planning including estate planning, retirement accounts handling, tax optimization strategies, etc.

- Credentials Matter: Check if prospective advisors hold reputable professional designations like Certified Financial Planner (CFP), certified public accountant (CPA), or chartered financial analyst indicating commitment towards maintaining high standards of ethical conduct, industry knowledge, competence areas of practice, and specialization. The Financial Industry Regulatory Authority (FINRA) has a tool that explains professional designations. You can also see whether the issuing organization requires continuing education, takes complaints, or has a way for you to confirm who holds the credentials.

Key takeaways

Private wealth managers use different compensation methods, including commissions on transactions, advisory fees based on total assets managed, and a combination of both. It's important to consider the value derived from the relationship with an advisor and their credentials when choosing one. Good wealth managers should be transparent about how they get paid and provide comprehensive planning services.

Conclusion

They offer financial advice to high-net-worth individuals, estate planning solutions, accounting services, and retirement solutions for clients, as well as offering additional services such as banking services and guidance on philanthropic activities.

Part of their job is to develop tax strategies that take into account domestic and international tax laws, and structure investments for optimal growth, while also regularly meeting with clients to mitigate potential inheritance taxes.

There are two types of advisors: traditional face-to-face advisors and robo-advisors, both of which employ various compensation methods.

It’s important to note that estate planning is a crucial aspect of wealth management, and a good advisor will help you plan for the future and ensure your investable assets are protected.

For more information on wealth management, check out this Investopedia article.

FAQ

A Wealth Manager is a professional who provides comprehensive financial services to clients, including investment advice, tax planning, estate planning, and retirement solutions. source

The main purpose of a financial planner is to help clients achieve their financial goals through strategic planning and managing their assets effectively. source

A Licensed Financial Advisor typically focuses on specific areas like investments or insurance while a Wealth Manager offers more holistic, comprehensive services encompassing all aspects of personal finance.

Wealth Management involves creating an investment strategy that helps grow your money over time while mitigating risks associated with market fluctuations.