How do banks make money from structured notes is a topic that warrants careful consideration, especially for expatriates at the CXO level residing in UAE.

As a complex financial product, structured notes associated with various underlying assets like interest rates, currencies, or commodities can offer enticing returns.

This post will examine the intricacies of the structured note, a complex financial product with potentially attractive returns linked to various underlying assets.

We’ll explore their working mechanism and discuss different types such as interest rate-linked structured notes, currency-linked structured notes, and more.

We will also address the risks associated with investing in these instruments – credit and market risks being primary among them.

Furthermore, we shed light on hidden fees embedded within structured notes which contribute significantly to bank’s earnings.

Apart from this, you’ll gain insights into Principal Protection Notes (PPNs) and understand the challenges faced by individual investors while dealing with them.

Last but importantly, we unravel tax implications impacting net returns which further elucidate how banks make money.

Understanding How do banks make money from structured notes

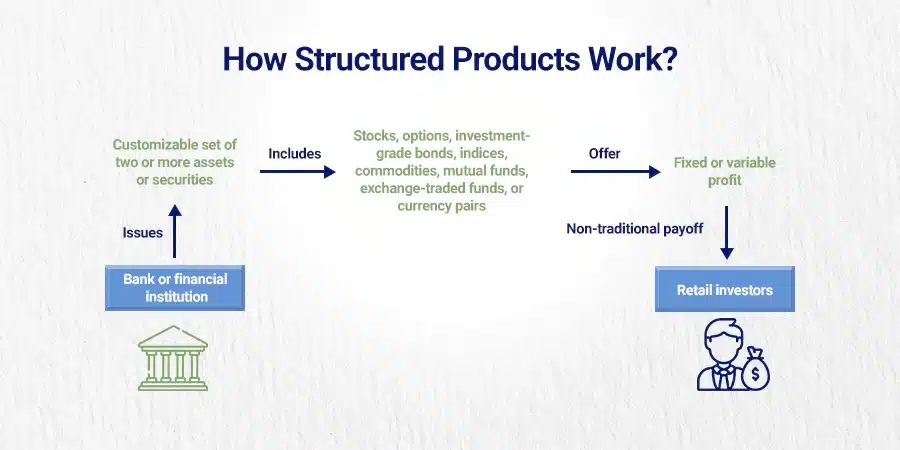

Structured notes are like a financial Frankenstein’s monster, created by banks that combine securities from different asset classes into one single investment product.

The goal is to achieve a specific risk-return balance over an agreed period of time, offering investors unique ways to diversify their portfolio and potentially could earn higher returns compared to traditional debt investments like bonds.

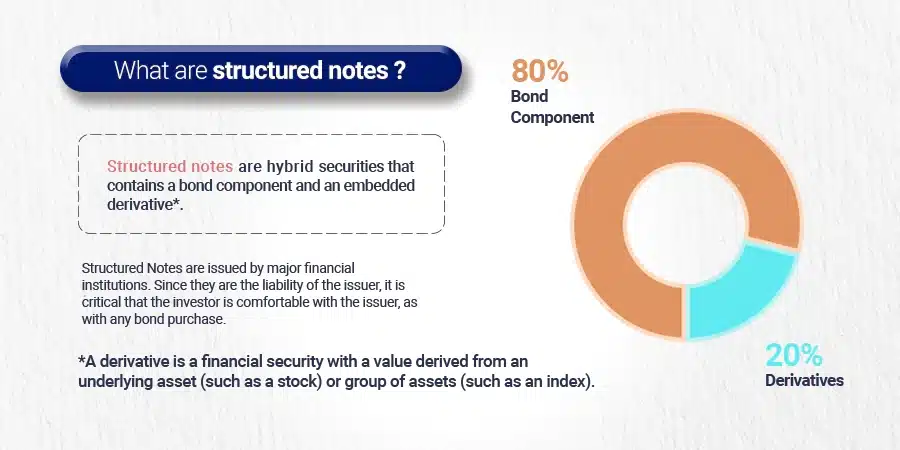

All structured notes have two underlying pieces: a bond component and a derivative component. The bond portion of the note takes up most of the investment and provides principal protection.

The rest of the investment not allocated to the bond is used to purchase a derivative product and provides upside potential to investors. The derivative portion is used to provide exposure to any asset class.

What are structured notes?

A structured note is a debt security issued by financial institutions. Its return is associated to the performance of the underlying asset such as stocks, mutual funds, commodities, indices, or interest rates.

The goal here is not only capital preservation but also the potential for high yield if the market performs well.

How do structured notes work?

The working mechanism of a structured note can be quite intricate due to its hybrid nature – part bond and part derivative. When you invest in a structured note, you’re essentially lending money to the issuing bank.

In return, the bank would make promises to pay back your principal plus any potential earnings tied up with the performance of certain specified assets at the maturity date.

This might sound similar to how regular bonds work; however, there’s one key difference: while bond payments are fixed irrespective of trading market conditions, returns on a structured note depend upon how well the (or poorly) underlying asset perform during the tenure of the note, making it more volatile yet potentially rewarding than conventional bonds.

Banks often tout these products as being ‘customizable’ since they allow investors flexibility in choosing their preferred level of risk versus reward trade-off based on individual tolerance levels and investment goals, thereby enabling them control over the final payout structure depending upon various scenarios related to movement in benchmark index or another reference asset (s).

In essence, though this feature makes them an attractive proposition, especially for sophisticated investors looking out for non-traditional avenues beyond plain vanilla equity or fixed income options available within the marketplace today, it’s crucial that prospective buyers fully understand all associated risks before diving headlong into the world of structured investing.

- Diversification

- Higher Returns

- Customization

- Principal Protection (in certain cases)

- Missed Diversification Opportunities

- Lower Potential Returns

- Limited Customization

- Missed Principal Protection Opportunities

Key takeaways

A Structured note is a type of investment product created by banks that combine securities from different asset classes to achieve a specific risk-return balance. They offer investors unique ways to diversify their portfolio and potentially earn higher returns compared to traditional debt/mortgage investments like bonds, but it's important for prospective buyers to fully understand the associated risks before investing.

The Risk of Investing in Structured Notes

Investing is like a box of chocolates, you never know what you’re going to get. Structured notes are no exception.

Investors must be cognizant of the potential risks associated with structured notes prior to investing.

Beware of Credit Risks

It is one of the biggest risks associated with a structured note. When you invest in a structured note, you’re essentially lending money to the bank issuing the note.

If the issuer goes bankrupt or defaults during the term of your investment, you could lose your entire principal amount invested.

This can be especially daunting for expatriates based in the UAE who may not have a complete understanding of the financial stability and credibility of investment banks operating in the Middle East region.

Market Volatility is a Major Concern

Market volatility is another significant challenge when dealing with a structured note. The return on these investments is typically correlated to the performance of a specified asset or based on equity indexes, which can be subject to changes based on numerous elements that are beyond an investor’s authority.

This includes everything from geopolitical tensions affecting oil prices globally to domestic economic indicators impacting local stock markets directly.

It’s important to evaluate or review market risks carefully when considering these types of investments.

Investors should weigh their appetite for taking on additional levels of uncertainty against the potential for higher returns compared to traditional debt instruments like bonds that offer fixed-rate interest payments until maturity.

Hidden Fees and Costs Embedded within Structured Notes

Investing in structured notes? Be prepared for a tumultuous journey. Gains may not be as simple to attain as they appear.

Banks often sneak hidden fees and costs into these complex financial instruments, which can significantly impact your overall earnings. Sneaky, right?

Types of Hidden Fees Associated with Structured Notes

The first type of fee you may encounter is a sales commission. This charge is paid out to brokers who sell these products on behalf of banks.

The amount varies but can be quite substantial depending on the size of your investment and the specific terms of the note. So, watch out for those brokers with dollar signs in their eyes.

In addition to sales commissions, there could also be management fees levied periodically throughout the tenure of your note. These charges cover financial supervisory costs such as record-keeping, reporting, and other operational expenses incurred by banks while managing these investments for their clients. It’s like paying for a fancy hotel room with hidden resort fees.

Furthermore, some structured notes may include early redemption fees or penalties if investors decide to exit before maturity. These charges serve as deterrents against premature withdrawals from such long-term commitments.

It’s like being punished for breaking up with your investment early.

Impact of Management Fees on Overall Earnings

The effect that management fees have on overall earnings cannot be overstated. While they might seem insignificant when viewed individually or over short periods, their cumulative impact over time can considerably erode potential profits from your investment in a structured note.

It’s like death by a thousand cuts. To illustrate this point further: suppose you invest $1000 in a structured note offering annual return rates of 5% with a management fee rate set at 1%.

After one year without factoring in any additional contributions or withdrawals during this period – instead of earning $50 (5% $1000), you would only receive $40 ($50 – 1% $1000) after deducting applicable management fees charged by the bank. Ouch. Here’s a more detailed explanation of how management fees work and how they affect investor returns over time.

Besides reducing net gains realized upon maturity or periodic payouts due to various embedded charges like those mentioned above; another significant aspect here involves federal taxes applicable on income earned via structured investments.

Taxes pose yet another layer complicating matters further for the potential investor, especially expatriates residing in UAE considering it either part retirement strategy or an alternative investment platform. We’ll delve deeper into tax implications tied up with such investments later in our discussion below. Brace yourself.

Key takeaways

Banks often charge hidden fees and costs within a structured note, including sales commissions, management fees, and early redemption penalties. These charges can significantly impact overall earnings over time, making it important for investors to be aware of them before investing in these complex financial instruments. Additionally, federal taxes on income earned through structured investments can further complicate matters for the potential investor.

Principal-Protected Note (PPN) Explained

If you’re an ex-pat or resident in the UAE seeking a safe investment, you might have come across a principal-protected note.

These financial instruments promise protection against losses up to a certain threshold level – the ‘principal’. Before making a decision, be aware that PPNs may not be complete without risk.

The Concept Behind Principal Protected Notes (PPNs)

A Principal Protected Note is essentially a structured note with two components: a zero-coupon bond and an options contract.

The zero-coupon bond component guarantees the return of principal at maturity, while the option contract provides potential upside tied to market performance. However, this assurance carries its own difficulties.

Challenges Faced By Individual Investors While Dealing With PPNs

- Complexity: PPNs are complex by nature due to their dual-component structure, which can be difficult for an average investor to fully comprehend.

- Liquidity Risk: While some PPNs offer secondary markets where they can be sold before maturity, these markets often come with substantial liquidity risks and price uncertainty.

- Credit Risk: Despite principal protection, there still exists these risks associated with the issuer defaulting or going bankrupt during the term of the note.

The complexity involved in understanding how PPNs work is one major challenge faced by the individual investor residing in the UAE who lacks adequate knowledge about such intricate financial tools.

Additionally, high costs associated with these products could potentially outweigh their benefits, making them unsuitable as an investment choice for many individuals seeking consistent growth in their portfolio through a structured note like those offered by Quadra Wealth.

- Fees & Costs: Banks issuing these notes typically charge upfront fees, which reduce the actual invested amount, thereby impacting overall returns realized upon maturity or periodic payouts from these investments. Money Crashers explains more about this here.

- Tax Implications: Federal taxes applicable on income earned via structured investments, including PPNs, can further erode net returns realized by individuals, thus indirectly contributing towards banking revenues through tax withholdings managed by banks on behalf of government authorities. For more information regarding tax implications related specifically to residents and ex-pats living within the Middle East region, you may refer to PWC’s guide here.

- Risk-Reward Balance: In pursuit of higher potential returns compared to traditional debt investments like bonds, investors should also consider inherent market risks tied to such types of alternative investment platforms.

- Capital Preservation

- Potential for Returns

- Diversification

- Tailored Risk-Reward Profile

- Lower Capital Protection

- Limited Downside Risk Mitigation

- Potentially Lower Returns

- Reduced Diversification

Key takeaways

PPNs are structured notes that promise full principal protection against losses up to a certain threshold level, but they come with complexity and risks such as credit and liquidity risk. Banks issuing PPNs charge upfront fees, which reduce the actual invested amount, while federal taxes applicable on income earned via structured investments can further erode net returns realized by individuals.

Tax Implications on Income Earned via Structured Investments

Investing in structured notes can lead to potentially lucrative outcomes, however, it is critical to be cognizant of the taxation implications associated with them.

Knowing how taxes can impact your net returns is crucial when considering this type of investment strategy.

Tax Implications Impacting Net Returns

The income earned from the structured investment is subject to federal taxes. This means that a portion of your earnings will be withheld by banks and paid directly to government authorities. These withholdings can significantly reduce your overall net return upon maturity or during periodic payouts.

For example, if you earn AED 100,000 from a structured note and are taxed at a rate of 30%, you would only receive AED 70,000 after tax deductions.

Over time, this reduction in earnings could substantially affect the growth of your portfolio and may even negate any benefits gained through diversification or higher potential returns offered by structured notes.

To help mitigate these effects, some investors choose tax-efficient strategies, such as holding onto their investments for longer periods to qualify for lower long-term capital gains rates or investing through tax-advantaged accounts where possible.

Banking Revenue Generation Through Tax Withholdings

Banks play an essential role in managing tax withholdings on behalf of government authorities. While they don’t directly profit from these withholdings themselves, indirectly it contributes towards banking revenues since handling such transactions typically involves service charges or administrative fees which are borne by customers like yourself who invest in their products including structured notes.

In essence, every time you earn money off a structured note so does the bank – not just from issuing the product but also managing its associated taxation aspects.

This dynamic further emphasizes why it’s critical for expatriates residing in UAE – particularly those at the CXO level looking into alternative investment platforms or retirement strategies – to fully understand all costs involved before venturing into complex financial instruments like structured notes.

A Word Of Caution For Potential Investors

- Educate Yourself: Always ensure you have adequate knowledge about any investment instrument before diving headfirst into it. Seek advice from a professional financial advisor who specializes in such matters if necessary.

- Analyze Costs: Prioritize transparency over complexity while dealing with banks, especially concerning hidden costs and fees embedded within sophisticated products like PPNs.

- Risk Tolerance: Determine whether taking up risks tied up with market volatility suits your risk appetite and long-term goals.

- Tax Planning: Incorporate efficient tax planning measures within your overall asset management strategy, keeping regional laws and regulations pertaining to foreign income reporting requirements into consideration.

Key takeaways

Structured notes can provide high returns, but investors need to be aware of the tax implications that come with them. Income earned from structured investments is subject to federal taxes, which can significantly reduce net returns. Banks play a role in managing tax withholdings on behalf of government authorities and indirectly profit through service charges or administrative fees. It's important for potential investors to educate themselves, analyze costs, determine risk tolerance, and incorporate efficient tax planning measures into their overall wealth management strategy when considering investing in structured notes.

Conclusion

How Banks Profit and Investors Can Lose

Structured notes are complex financial products that come with risks and hidden fees, making them a profitable investment for banks.

Banks make money from structured notes by charging management fees, creating new products for investors to buy, and earning revenue through tax withholdings.

Investors should be aware of the potential risks associated with investing in structured notes before making any decisions.

It’s essential to do your research and consult with a financial advisor before investing in structured notes or learning more about how banks profit from them.

Understanding how banks make money from structured notes can help you make informed investment decisions based on your risk tolerance and financial goals.

Frequently Asked Questions

A structured note is a debt obligation that also contains an embedded derivative component that adjusts the security’s risk-return profile.

Banks make money on structured notes through the spread between the cost of funding and payouts to investors, as well as management fees and the securities commission.

Issuers generate revenue through underwriting fees, selling premiums on options embedded within the product, and exploiting price inefficiencies.

Banks offer structured notes to raise capital without issuing bonds or shares while providing customized risk-return profiles for investors.

- Commission rates can vary widely but typically range between 1% to 8%, depending on factors like complexity of structure and tenure of investment.