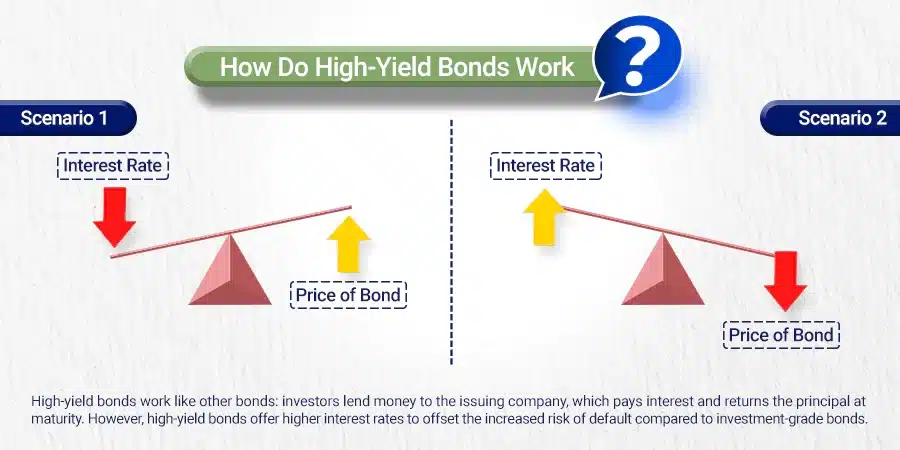

High-yield bonds, like any bond, are essentially loans you make to a company.

In exchange for your money, the company promises to pay you back a set amount (the principal) at a specific date (maturity) and make regular interest payments (coupons) throughout the loan term.

However, unlike safer bonds with investment-grade ratings, high-yield bonds are issued by companies categorized as riskier by credit rating agencies.

This higher risk translates to a higher interest rate for you, the investor, as compensation for the increased chance the company might default and not repay you.

You potentially earn more, but you also take on a greater chance of losing your investment.

Why You Need a Personal Financial Manager?

Personal finance management (PFM) is not confined to budgeting and investment any longer. There are

Nearing Retirement Advice for a Secure Future

Nearing retirement advice? A plan for retirement is essential to enjoy a happy healthy life

What is Debt Ceiling? A Complete Guide for Beginners

What is Debt Ceiling? Debt Ceiling, also known as the debt limit, is the highest

Is It Possible to Have No Debt?

Debt is often considered the norm in the corporate world, but the debt free companies