The Dilemma of Retirement

Jonathan paced his study, he was contemplating something which none of his counterparts in friends and family had considered. He was 62, retirement loomed, and he had amassed healthy retirement accounts with unwavering dedication.

The fruits of decades of hard work demanded a final resting place. Should he follow the usual path accepted by the majority, naming his children as beneficiaries, or venture into a more secure legally binding way of opting for Trusts?

Well, Trust would inculcate certain costs and also a step more added to access his retirement funds.

Children And Your Retirement Corpus Uncertainty

Jonathan had always been a meticulous planner, distrustful of ambiguity. His daughter, Sarah, a free spirit, has always been impulsive and Jonathan knew his patience and meticulous planning were not a part of her personality.

His son, Michael, while responsible, had a family to look after and was still grappling with student loans. He could imagine his retirement funds flying away in whims and obligations leaving his children vulnerable.

Retirement trusts introduced

However, as the universe conspired, he accidentally met with his old college friend Emily, now a lawyer specializing in estate planning.

The idea of trusts was introduced. Emily explained about controlled distribution, asset protection, and tax benefits, all wrapped in the security of a well-drafted document.

It sounded too convincing to be true, but a ray of hope flickered within Jonathan. He put on his research hat and found all the details of trust types and legalese.

There were multiple types of trusts, each having its benefits and drawbacks. He also found that your individual retirement account (IRA) cannot be placed in a trust while you are living.

However, you name a trust as the beneficiary of your IRA and dictate how the assets are to be handled and transferred after your death. This is true for all types of IRAs, including traditional, Roth IRA, SEP, and simple IRAs.

You must also understand the features and characteristics of IRAs if you intend to pass them on to a trust later.

Weighing The Decision To Opt For Trust

Jonathan sought Emily’s guidance, her calm demeanor and clear explanations soothed his anxieties.

He discussed his concerns with Sarah and Michael, their initial resistance melting away as they understood his desire to ensure their long-term security.

Finally, Jonathan reached a decision. He opted for a combination of trusts (details of which we will explore in the later part of the blog).

He catered to both his son’s and daughter’s requirements and even ensured their long-term security.

The process wasn’t easy. Legal fees, paperwork, and family discussions filled his days, but with Emily’s expertise and the support of his loved ones, he navigated the complexities.

As the trust documents were finalized, a sense of peace settled over him.

The Sweet Fruits Of His Decision

Years later, Jonathan looked at his children, their lives were thriving.

Sarah, her wanderlust satiated, had settled into a fulfilling career.

Michael, with a secure financial foundation, was building his legacy.

The trusts, once a source of worry, had become instruments of love and security, ensuring his legacy lived on, not just in wealth, but in the well-being of his family.

Jonathan’s story speaks about the ultimate benefits of informed decisions and careful planning.

While trusts may not be a solution for everyone, for those seeking control and security of assets even after death trusts are a great way to go.

Possibilities of Placing Retirement Accounts in Trusts

Retirement accounts represent a significant portion of their accumulated wealth, holding the promise of financial security and freedom in golden years.

But questions always loom, how to ensure a smooth transition of retirement funds to beneficiaries, will the beneficiaries access and use your hard-earned corpus in the right spirit?

While naming individual beneficiaries is a common option, an increasingly popular wand evolved way today is leveraging trusts for more control and flexibility.

However, trusts are often viewed as a third party which may just add a layer of complexity for transitioning the corpus.

Today we will understand the world of trusts and retirement accounts, exploring the potential benefits, drawbacks, and essential factors to consider.

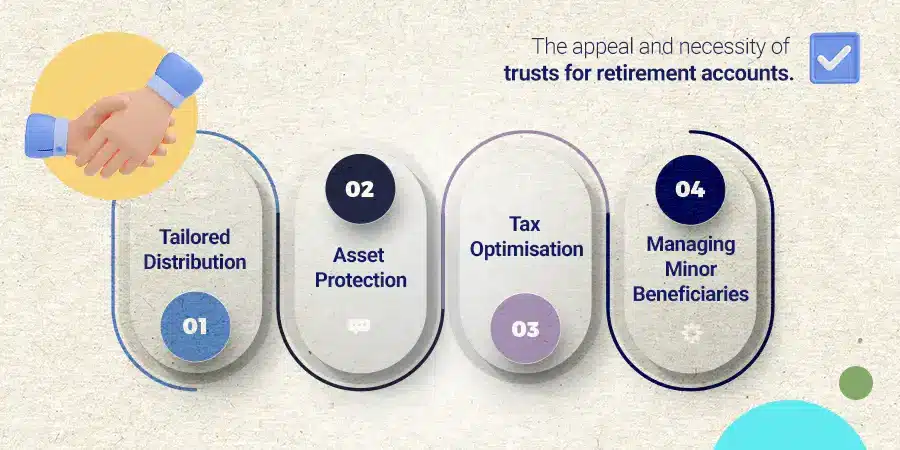

The appeal and need of trusts for retirement accounts

Traditional beneficiary designations offer simplicity, but they lack the enhanced control and potential advantages that trusts provide. Here’s why placing retirement accounts within trusts can be appealing:

• Tailored Distribution:

You can specify how the trust distributes the retirement account funds to your beneficiaries. This allows for systematic distribution, or even conditional disbursements based on specific milestones or achievements.

This ensures responsible management and catering to your beloved needs at the right time.

• Asset Protection:

Trust assets can shield them from creditors of your beneficiaries. Your assets can be attached to beneficiaries’ loans post your demise if they are not protected by trusts.

If your assets are with trusts, your beneficiaries’ creditors cannot claim them. This offers a layer of protection against unforeseen financial challenges.

• Tax Optimisation:

Depending on the trust type and structure, you may be able to minimize estate taxes and income taxes on the retirement account assets, maximizing the value passed on to your loved ones.

• Managing Minor Beneficiaries:

If you have young children or beneficiaries who may not be financially responsible, a trust can manage the retirement account assets until they reach a certain age or meet specific conditions, ensuring responsible stewardship of their inheritance.

The reality check: are retirement trust accounts worth it?

While the benefits are tempting, using trusts for retirement accounts isn’t without its complexities:

• Added Complexity:

DRIPs automatically buy stock directly at regular intervals, regardless of the market price. This helps average out your cost per share, reducing the impact of market volatility and potentially lowering your overall investment cost.

• Tax Implications:

The tax implications of trusts can be complex and vary depending on the type and structure. Consulting a tax professional is crucial to avoid unintended tax consequences.

• Loss of Control:

Once assets are transferred to the trust, you relinquish direct control over how they are managed. This can be a significant consideration, especially if you have specific preferences for how your beneficiaries utilize the funds.

Exploring the options: types of trusts for retirement funds

Not all trusts are created equal, and the type you choose significantly impacts your further course of action. Here are some common options and their key characteristics:

• Testamentary Trust:

Created within your will, this trust receives the retirement account assets upon your passing. It offers flexibility but may not protect assets from creditors during your lifetime.

• Revocable Living Trust:

Established while you’re alive, this trust allows you to transfer assets, including retirement accounts, and retain control until your passing.

It offers asset protection and flexibility but can have complex tax implications.

• Spousal Lifetime Access Trust (SLAT):

Designed for married couples, this trust allows one spouse to transfer assets to the other spouse while minimizing estate taxes. It offers tax benefits but may have limited flexibility in distribution.

Parting Thoughts

Deciding whether a trust is the right path for your retirement accounts requires careful consideration and expert guidance. Here’s what you need to do:

• Consult a financial advisor: They can assess your financial situation, goals, and risk tolerance to determine if a trust aligns with your overall strategy.

• Seek legal advice: An experienced estate planning attorney can guide you through the legal intricacies of trusts, help you choose the appropriate type, and ensure it’s drafted and structured correctly.

• Understand the tax implications: A tax professional can advise you on the potential tax consequences of using a trust for your retirement accounts and help you minimize any tax burdens.

• Communicate with your beneficiaries: Discuss your intentions and expectations with your beneficiaries to ensure they understand the trust’s purpose and their roles.

Remember, every individual’s circumstances are different, and hence their decisions regarding finances should be planned accordingly.

By carefully evaluating the benefits, drawbacks, and available options, seeking professional guidance, and ensuring clear communication, you can avail and utilize trusts effectively to secure your legacy and protect your loved ones’ financial future.