Introduction

Are you a newbie in the field of investing? Well, then you must have an overwhelming number of options that stand in front of you. You may have to choose between bonds, fixed-income securities, equities, commodities, exchange-traded funds or ETFs, mutual funds, and a whole lot of them.

The investment plans can also be confusing to learn or understand. The terms and conditions you have, followed by market volatilities or risks involved can be yet another brainstorming challenge for you to navigate.

By researching one financial topic every single day, you get a know-how on how things work in the dynamic field of investments and finances. Simple and lucid blogs can break down complex stuff into easy-to-understand layman’s language for you to get the product know-how of every financial instrument you have in town.

On a similar parlance, let us unveil the key points of differences covering Structured Notes Vs Fixed Income Securities by also giving you a touch-down into the revolving specifics. Helping you get started here:

What are Structured Notes- Meaning and Conceptualization Explained

Structured Notes are hybrid products that comprise an optimal mix of bonds and equity. A note comprises a promissory note in the name of the buyer and this is the predominant bond portion of the note. The bond portion acts as a capital protection vault that prevents your principal wallet amount from getting eroded.

The note also comprises underlying assets that comprise equities, currencies, commodities, fixed-income securities, or ETFs to name a few.

While the bond protects the capital investment for the investor, the underlying assets amplify income levels as they are exposed to equities or stock markets. You can diversify your sources of income via coupons, interest payouts, capital buyouts, dividend disbursements, etc.

At the same time, you have soft calls initiated via call or put options and you play a relatively safer game here as you get a certain percentage of your capital protected even in adverse market scenarios or plunging economic downturns.

The structured notes therefore provide you with the best of both worlds- bonds plus equity-based assets thereby lending a more diversified income portfolio for you as an investor.

What are fixed-income securities- Meaning and Conceptualization Explained

Fixed-income securities are typically bonds that appeal to risk-averse investors on the whole. The bonds offer regular interest payments in the form of coupons and offer the capital sum at the end of the tenor period that comes with the investment option.

Fixed-income securities provide passive income to retirees and pensioners as they provide regular interest payments throughout the tenure period of the investment. Plus, the capital sum is ensured at the end of the term period.

Some of the classic examples of fixed-income securities are:

- US Treasuries

- Corporate Bonds

- High yield bonds

- Tax-free municipal bonds

- Commercial paper and

- Certificates of Deposits or CDs

Fixed-income securities, as an investment product, are in demand even today owing to investors getting fixed-income sources, capital payback, and tax waivers as a part of this particular investment redemption.

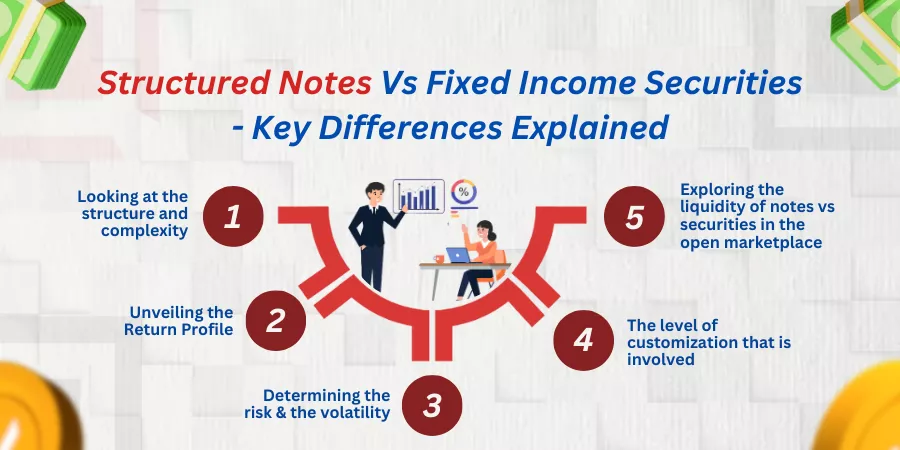

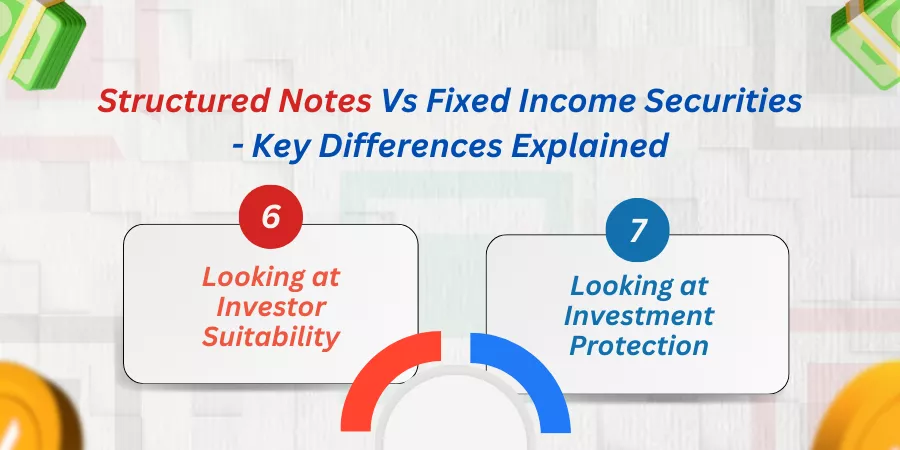

Structured Notes Vs Fixed Income Securities- Key Differences Explained

These are the key areas of differences covering Structured Notes Vs Fixed Income Securities. Helping you get started further:

Looking at the structure and complexity

Structured notes are hybrid securities that mix bonds with derivative components. The bond provides upside protection against capital loss. The notes also have underlying assets that comprise derivative/ index components. The assets include equity-based assets like high-paying securities, currencies, commodities, and futures, to name a few. The returns of investment are linked to the performance of the assets the structure notes are linked with.

Equity-linked Notes or ELNs, Autocallable Notes, Reverse Callable Notes (RCNs), Principal-protected Notes (PPNs), and Credit-Linked Notes or CLNs are the different types of structured notes you can think of.

Whereas, with respect to fixed-income securities, these are just bonds that provide investors with regular interest payments in the form of coupons. And, this investment option also repays the capital sum at the end of the tenor period of the same. Therefore, this is an investment option that has an easier structure to learn or understand. The returns on investment are usually predictable and prove the creditworthiness of the product issuer.

Unveiling the Return Profile

Structured Notes have a high risk-high returns profile. This is mainly because the returns on investment are linked to the performance of underlying assets the notes are tied with. These underlying assets include equities, high-paying stocks, shares, and commodities. The returns of investment therefore are subject to the volatilities of the derivative market the notes are exposed to.

Whereas, with fixed-income securities, the returns on capital remain static and fixed in nature. The bonds supply regular interest payments or coupons to investors and the capital sum is usually returned by the end of the term period of the investment. Therefore, fixed-income securities operate on a lower risk lower returns profile.

Determining the risk and the volatility

Structured notes are hybrid investment options that operate on a higher risk higher volatility pedestal. If the underlying assets of the notes perform exceedingly well, then the returns on investment can be much higher than traditional bonds. However, if the underlying commodities or equity stocks perform poorly in the market, then investors do not get any returns on investment and a part of their capital investment gets eroded too.

Whereas, with respect to fixed-income securities these are bonds that provide a stable rate of returns on the investment portfolio. The returns are in the form of regular interest and coupon payouts the investor receives on a periodic basis indeed. The capital sum is also returned to the investor at the end of the tenor period of bonds or fixed-income securities.

However, the capital investment is at risk if the product-issuing firm or the credit-issuing firm defaults. Fixed-income securities also face market volatility in the form of interest rate fluctuations or growing inflation rates in developing economies.

The level of customization that is involved

Structured notes allow a maximum level of customization. These notes are designed to provide tailor-made investment solutions that align with the investor’s independent needs or requirements on the whole.

Whereas, in the case of fixed-income securities, you do not have any amount of scope to customize the term period or minimum capital requirements each bond demands. The terms and conditions are designed by the credit-issuing firm alone and investors have little say on how much returns of investment can be received vis-a-vis the term period at which their capital sum is made available to them.

In a nutshell, fixed-income securities comprising municipal bonds, US treasuries, or corporate bonds are less customizable as compared to structured notes.

Exploring the liquidity of notes vs securities in the open marketplace

Structured notes are less liquid as these are notes that are extensively designed for ultra-rich and high-net-worth retail investors. Therefore, the notes are highly specialized or customized to meet the specific needs of investors. These notes therefore are not commonly traded across OTC (Over-The-Counter) Markets.

Whereas, fixed-income securities comprising govt bonds or large-value capital-intensive corporate bonds are highly liquid in nature and these investment options have established secondary markets and can therefore be actively traded in public markets comprising stock exchanges or public funded financial conglomerates on the whole.

Looking at investor suitability

Structured notes are designed for sophisticated investors and for those of you who can take higher risks over potentially higher returns. These notes are designed for those investors who can work with the call, put, or hybrid market movements that unravel in a specified direction. Therefore, these are investment portfolios for experienced and savvy investors and are not meant for risk-averse investors on the whole.

Whereas, fixed-income securities provide regular income levels in the form of interest payouts or coupons. Plus, there is a guarantee the product issuing firm gives to investors that their capital sum will be returned back to them along with interest payments at the end of a specific tenor period the investment option comes to you with. Therefore, these are risk-free investment options meant for retirees, pensioners, and the more conservative sector of investors who look for regular income flows and capital preservation.

Looking at investment protection

Structured notes come to you with full or partial principal protection. This is mainly because the returns of investment are primarily dependent on the performance of assets the notes are linked with.

Whereas, in fixed-income securities or bonds, the investment offers a greater degree of principal or capital protection to investors. This holds with the exception of the credit-issuing firm defaulting due to economic downturns or issuance of a statement by the US economy of a global recession.

For instance, US Treasuries are nearly 100% principal-protected investment options on the whole.

The Bottom Line

Structured notes require a better understanding of how the markets work. This is because you have a bond component and the underlying derivative component the notes are linked to.

While the bond component or the promissory notes offer soft capital protection the performance of the notes relies upon how the linked-in assets of the notes fare in the marketplace.

These notes therefore require years of experience for investors to learn, understand, or operate with.

On the other hand, fixed-income securities have been operating in the markets for several decades. These are investment options that have simpler structures and can be operated by newbie or amateur investors too. The fixed income securities are preferred by traditional investors who would want regular income levels with lower risk factors.

To choose between the two, you can approach a wealth management firm or get help from a fiduciary financial planner who can steer you through the nuances of choosing the right investment portfolio.

What are your thoughts on this? Do mention it in the comments below!

Frequently Asked Questions or FAQs

Define Structured Notes

Answer: A structured note is a note that comprises debt and equity. The structured notes may comprise the principal amount for the bond and comprise a group of assets that underlie within. Therefore, this is a hybrid security comprising bond component and a derivative.

Can changes in a foreign exchange rate impact returns on investment for a note?

Answer: Yes, if your note comprises multiple currencies as assets then dip or rise in foreign exchange rates can impact the return on an underlying asset for a note.

How do you decipher the returns on investment for a structured note?

Answer: The note is typically a bond component and a derivative component put into the same investment portfolio. This is a debt security component wherein the risk-reward profiling is linked to the return on investments for the assets the notes are linked with.

These notes are issued by financial institutions that have a high credibility in the financing cum investments market place. You can reap the benefits of an enhanced growth potential wherein the asset class determines the rate of returns and the bond may provide a reasonable degree of capital insured component to the investor’s initial principal money.

This is done by including soft protection options of call or put on the futures. Your understanding structured returns comes from a reasonable experience of investing in the bond or stock markets.

How can you enhance your earning potential using these notes?

Structured notes can be leveraged as income notes. Or, you can use them as commodity-linked structured notes or currency-linked structured notes or further use them as credit-linked structured notes based on your customized investing preferences.

You can use these notes as growth notes as underlying assets appreciate over a point or duration in time. You receive different payouts like coupons, interest earnings, autocallable redemption rewards, dividends, etc.

This way, you can enhance your growth potential over traditional bonds or stand-alone securities.