Introduction

As someone who has started afresh in your investment journey, you must carefully evaluate every investing plan’s pros and cons to determine which is the most ideal for you.

On a similar note, you must also know the kind of risk tolerance you can take under your investment belt. Choosing products accordingly can help you manage your income or wealth-earning dimensions accordingly.

At the same time, tax implications may vary from one investment product to another. As first-time investors, you can also get guidance from tax consultants as to how the tax protocols vary between different investment products.

In parlance to the above, let us learn how the theme behind structured notes capital gains works for investors.

Structured Note capital gains- Tax implications explained

Structured notes may work in such a way that the investing product uses an optimal level of debt and equity to realize wealth for the investors. As you can rightly see, this is one of the latest innovations in the world of finance. This is mainly because structured products offer an innovative spin to the traditional equation between stock/ commodity and bonds.

You get a potential upside from equity in a structure that is encased with a bond. Therefore, potential investors must understand the specifics behind how taxation norms work on structured notes as such.

As the notes are predominantly considered debt instruments, the potential return you receive from the notes is also treated as a regular source of income. And, the gains you receive from the notes are not treated on lower slabs of taxation as is done for the income you earn via capital gains.

Interestingly, investors may be taxed even before receiving their coupon payments or before receiving their capital money as the notes are tending to maturity. In other words, before the notes mature.

It is also be noted that different notes come with different taxation slabs. Therefore, the investors must go through the US Securities and Exchange Commission’s prospectuses to have a clearer picture of tax implications. A financial advisor can also help you with liquidity, secondary market conditions and varied aspects concerning notes.

How can structured notes help you diversify your investment portfolios?

Structured notes are gaining increasing popularity in the market as they provide a wide range of investing opportunities for savvy investors. These were issued in favor of posh retail and institutional investors a couple of decades back.

However, these notes are now touching the retail markets wherein more and more novice and low-key investors are also wanting to foray into this hybrid segment of investing. This is mainly because structured notes allow investors to build their portfolios using the highest degree of customization. The investor can simply personalize his/her risk-handling stature and thereby avail a reasonable range of returns from the performance of the underlying assets the notes are linked to.

As an investor, you gain access to a wider market exposure without directly investing in the assets of companies. Therefore, the investors are exposed to potential risk factors also in a spread-out manner. These notes provide better rates of return over traditional bonds or fixed-income securities.

In a way, structured notes provide an exposure to investors that is usually not found in standard investing practices. The innovative and intriguing aspect of these notes draws investors and financiers in favor of this trillion-dollar industry. As investors get access to unique investing opportunities, you can say that these notes offer protection against principal investment. This also means you get a safety net from volatile market conditions as potential gains are based on the performance of underlying assets.

Structured notes package risks and rewards in a hybrid format that can be complex to initially learn or understand. These reasons substantiate how structured notes or products can diversify your investment portfolios in attractive ways when you see that the notes give a unique blend of equities, fixed-income bonds, and derivatives. The customization allows investors to introduce buffers or even spreads to get downside protection against capital erosion which are otherwise challenging to achieve via traditional bonds or securities.

Understanding the pros and cons of structured notes

Let us now move on to understand the pros and cons of structured notes.

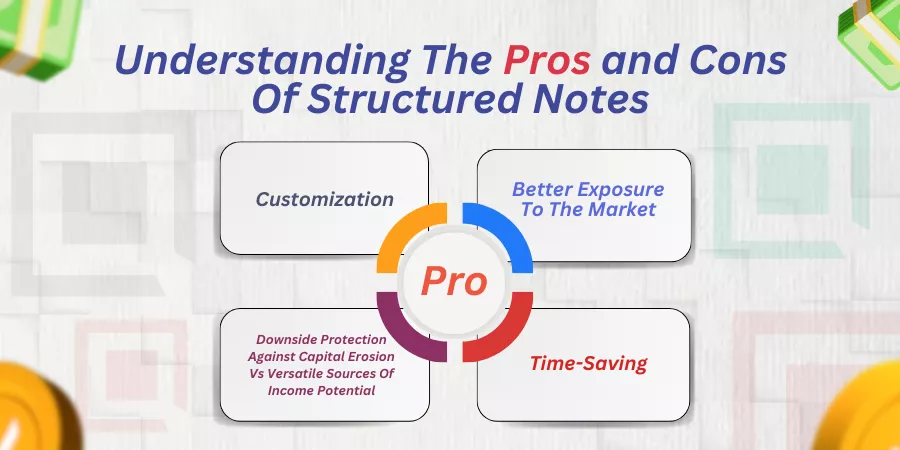

Pros of structured notes

Customization

Investors have immense potential to choose their investment portfolios based on the risk-tolerance they can take in under their belt. You can look for downside protection against capital loss or principal erosion. At the same time, you can also look for contingent sources of income that are made in the form of coupon payments.

As an investor, you can also choose between income or growth notes that link income generation with bonds or equity funds. As structured notes provide a hybrid mix of debt and equity, you are free to choose or customize the financial instruments of your choice.

Better exposure to the market

Investors get a better exposure to the growing markets. As these hybrid notes have promissory notes or bonds that are linked to equity-based assets, you get exposure to the primary as well as the secondary markets.

As structured notes are hybrid components, investors have their investments linked to the underlying assets of performing shares or securities belonging to equity. At the same time, the long-term values of assets are assessed to determine the final payoff on investments.

The underlying assets can be in the form of stock market indexes, commodities, currencies, etc. Therefore, investors get better market exposure with structured products as compared to fixed interest rate bonds or fixed income securities.

Downside protection against capital erosion vs versatile sources of income potential

The structured product issuers add buffers and options to prevent the instruments from financial degradation. For instance, a buffer can provide hard-core protection against capital erosion. Barriers on the other hand provide soft protection against non-performing assets to the limits that have been set.

Investors therefore get downside protection against unprecedented losses as in the case of direct investments made in the same asset portfolios. The potential income is also based on the performance of underlying assets the notes are attached to or linked to.

Say, for instance, an autocallable note that offers returns of 15% pa, gives you principal and coupons as the notes get auto-called. Here, investors do not even have to wait until the entire term of these notes.

However, the return on a structured note can differ from one type of structured note to another. Say for instance, notes also combine cds with derivative component, the performance of underliers have a bearing on the overall payout factor of the investment portfolio. That primarily explains how the notes do not work like traditional investing options.

In a nutshell, getting income via multiple streams vis-a-vis protecting your capital from erosion prove brownie points in structured products.

Time-saving

To physically look for income notes or growth notes that provide soft-core or hard-core protection against capital investment or to procure investment products that expose you to the upside potential for returns linked to equity markets, you may have to take a long wait to discover investment products of such a genre.

However, in the case of structured notes, you get the best of everything under a one-stop-one shop hub and thereby increase your potential to build your wealth.

Cons that are associated with Structured products

These are the cons that are associated with structured products. Helping you get a run-down into what these are:

Limited liquidity

As structured notes are curated using the highest degree of customization, these notes can be optimized for every independent or individual investor, it is hard to find buyers in a similar genre in the primary market.

However, notes can be bought, sold, or even hedged between investors in the secondary market comprising banks and stock exchange firms.

On a general note, the liquidity for structured notes is not all that great or easy to work around.

Rigidity for pricing

The pricing of structured notes is done by a matrix method or what is known as the average guessing method. Therefore, you know how the underlying assets are performing only on the day of observation.

In a way, things get riskier for investors. This is because if assets decline or slump in their values or get volatile, then investors may be at risk of losing their partial or entire capital base.

For instance, you have a 5-year term note that is linked to Proctor and Gamble. If the shares are traded above threshold limits over 4 years and 11 months, then the investors may receive a complete payout on their investment. The yield earnings from the asset also get added in the form of contingent coupon pay outs.

On the other hand, when the linked-in asset, say P& G in this case fares badly at the marketplace and no autocalls get triggered, then investors can lose income payouts and even a part of their initial investment.

Call risks

Sometimes, the product issuing company gets busted or signs up for insolvency, then investments or even structured notes of the firm gets impacted adversely.

For instance, during the year 2008, it was Lehmann Brothers that had signed up for insolvency and all of its structured notes were rendered valueless.

Higher fee structure

As a matter of fact, the initial investment for a structured note starts at 100,000 USD or roughly 0.1 million US Dollars. And brokerage fee for getting the structured product curated according to the customized requirements of investors may range from 5 to 10% of the initial investment. Therefore, the fees for designing notes is way more expensive as compared to what you have in mutual funds, etfs or regular bonds.

Tax implications

Contingent income coupons can be treated as regular income and the tax slabs are worked out accordingly. You cannot expect the income you derive from structured products to be treated as capital gains that may have lower tax slabs.

Sometimes, even while the coupons are about to get paid, investors are billed for their taxes. Therefore, investors must learn the overall tax implications with respect to structured products.

You can get relevant info from a tax advisor who can provide the right kind of guidance with respect to how taxes work on different investment portfolios.

The Bottom Line

As you find high volatility, stretched market valuations, and lower interest rates, you find that it is not a feasible option to merely invest your money in fixed bonds or mortgages. It is the structured notes that offer a convenient middle ground between debt and equity.

Investors of structured notes get a decent level of principal protection. And, they receive income from the higher-performing assets the notes are linked to. At the same time, they get exposure to potential gains from the performance of underlying assets, equities, and derivatives the notes are embedded with.

As you have all elements of investment diversification, investing in notes is rewarding.

What are your thoughts on this?