Introduction

At the speed at which inflation is rising in the US and other major economies, you may not be able to expect things to settle down that easily.

Interest rates and the cost of tangible goods and services are rising sharply.

Therefore, it is understood that the cost of living has become far dearer even for the common man. And, it is just not possible to run the family on a 9-5 job alone. You may have to look for passive sources of income to be able to pay your bills and make other ends meet.

Investing in reliable resources can be a great way to harness wealth. The compound interest grows and therefore you get handsome returns at the end of the term. Therefore, you must get into an investing platform to invest your money. And, getting to know how different investment portfolios work is also imperative.

On this note, let us discover how a leveraged credit-linked note works.

Leveraged Credit-Linked Note- Meaning And Conceptualization Explained

A leveraged credit-linked note is a structured note wherein the bond has an underlying credit-based derivative. The bond is linked to the creditworthiness of the issuing company. Here, the credit-based derivative can be one credit entity or a basket of entities.

The main aim behind issuing credit-linked notes or CLNs to investors is to diversify the credit risk profile across a firm or a group of companies.

These notes are designed in such a way that the credit risk gets transferred between two main parties. The note transfers the credit risk between the issuer and the investor.

And, the investor gets a leveraged credit risk of the firm to earn higher returns on CLNs. The potentially higher returns are given to the investor to assume the credit risk of the issuing company or firm.

Features Of Credit-Linked Notes Or CLNs

Let us have a core understanding on what are the different features that are linked to CLNs. Helping you get a run-down into the same:

Embedded With A Credit-Default Swap

The CLN is always embedded with a credit default swap through which the issuing company transfers its credit risk among a group of credit investors. This is done with the purpose of transferring the risk profile of the company amongst independent investors who are then awarded higher rates of return for assuming the company’s overall risk. Hence, this is a note that is embedded with a specific credit event for which the investor receives a higher yield on the note.

Issuance Of CLNs- The Process Know-How

The CLNs are then issued after the issuing firm bifurcates how much of the credit profiling risk is to be shared amongst every individual investor who may need to purchase these notes and the price of the notes is also determined beforehand. A special purpose vehicle or SPV is then created for these notes. The SPV is typically a trust and this investing wheel exposes the investors to collateralized forms of AAA securities. In a way, the CLN is a credit bond wherein the performance of one credit firm is linked to the performance of other credit firms that are agencies or trusts.

Returns on Investment Or ROI

When investors buy these CLNs from a trust or SPV, they get fixed or floating coupons that can be used throughout the term of the asset. To compensate investors for assuming the credit-profiling risk of the issuing company, the product issuer provides attractive rates of returns over the notes. The investors can receive a potentially higher income from what they earn via traditional bonds or fixed-income investments.

The Process Know-How Of CLNs

Would you like to know how CLNs are curated? Well, this segment deals with the process know-how behind how CLNs are created. Helping you get a run-down of steps about the same:

Loans Created To Issue To Investors

To sell the notes to customers or investors, a specific loan component must be created in the first place. The loan is issued to the investors and this is done by the product issuing firm of CLNs. As these loans are repaid by investors, the credit-issuing company receives interest-backed repayments. The credit issuing firm may decide to withhold their CLNs or sell them to other entities.

The Loan Component Gets Divided Into Bundled Parts

Usually, the credit issuer sells their loan components to other entities and trusts through their SPVs. The entire loan components are subdivided into fragmented versions of the same. The sub-divided loan fragments are further bundled together in the form of notes or securities that investors can purchase. The bundling of loan fragments is done based on their overall credit rating. This is the exact know-how to specify how CLNs are curated for investors/ borrowers to buy or purchase.

At The Time Of Maturity

When the term of this investment is about to mature, the investors usually get a complete value of their investment. Apart from the principal amount, they also receive fixed or floating coupon payouts through the term of the asset.

However, the credit-issuing firm may default or sign up for bankruptcy. It is at this point that the investor’s principal investment is at risk. In this case, the trustee manager arranges for funds based on the recovery rate the firm can afford to pay off after selling its movable and immovable assets. Hence, this is the par minus the recovery rate investors get upon redemption.

In a nutshell, a cln is a specific credit risk to credit investors wherein a reference entity has embedded credit default swaps of itself along with other entities.

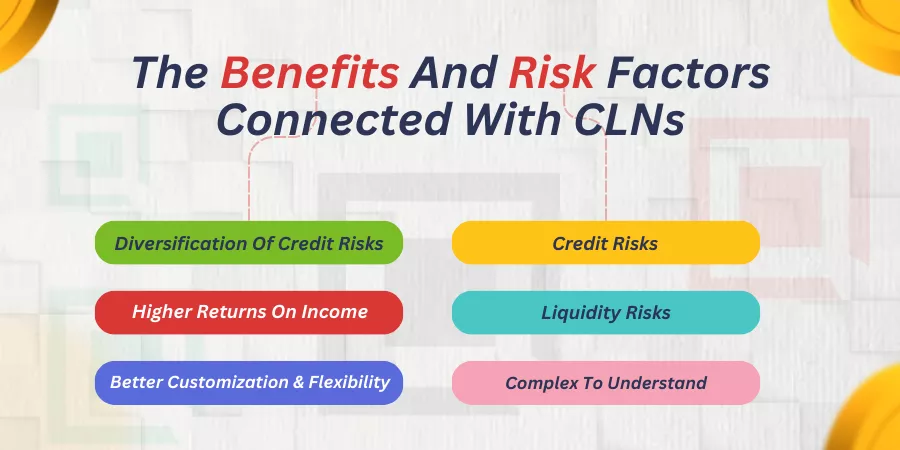

Let Us Understand The Benefits And Risk Factors Connected With CLNs

Benefits Of CLNs

These are some of the lucrative benefits the investor gets from CLNs. Let us find out what they are:

Diversification Of Credit Risks

Through CLNs, the investors get an opportunity to diversify their investment portfolio in a phenomenal manner indeed. This is because they get to invest in the credit profiling of different underlying firms. Typical to a diversified investment portfolio, this is a credit-sharing portfolio that investors take within their belt. A diversified credit portfolio helps negate the influence of individual defaults and the overall investment portfolio stays protected.

Higher Returns On Income

The credit linked notes provide investors with opportunities to receive higher returns of income over traditional bonds or fixed-income securities. As the investors assume the credit risk of the issuing firm, they are compensated or rewarded handsomely for the same. Hence, you get returns on investment from the note for accepting an exposure hedge against the credit risk of the said firm.

In a crux, in exchange for an annual fee for accepting exposure to a specified credit risk vis-a-vis gauging the performance of a reference asset, the income in the form of a higher yield covers investors in the form of floating or fixed coupons. Mostly, investors get their principal plus returns unless the referenced credit assets do not perform as expected.

Enjoy Better Customization And Flexibility

As this is a structured or leveraged credit-linked note that we are talking about, the investing product gives investors better flexibility and customization on how they want to work things around. The investors can structure these products to meet their specific financial or wealth-generation objectives on the whole. As fixed and floating coupons are paid on CLNs, the investors also get a regular stream of income to add to their kitty. Here the investors can choose coupon dates, maturity dates, and underlying asset types based on which the CLNs are customized.

As an investor, you can also choose from different types of credit-linked notes as the notes may have underlying securities with an embedded credit or have favorable issuer to transfer specific credit ratios. These notes give borrowers a hedge against credit facilities and the notes are often directly linked to the performance of underlying entities that can boost up the derivative markets on the whole.

Risk Factors Of CLNs

Like any other investment product, CLNs also have a fair share of risks attributed to the same. Let us find out what the risk factors are:

Credit Risks

CLNs are primarily subject to exposure to a specified credit event and thus the risks associated with the personal default of the product issuer are greater. if the creditworthiness of the issuing firm is at stake, then the payment obligations can be deterred which allows investors to lose their principal or capital investment. Therefore, this is a financial instrument whose total return depends on the credit health of the issuer.

Liquidity Risks

CLNs cannot easily be disposed of in the secondary market. The investor must know the implications of this product to sell the notes to another buyer. Therefore, things can run complicated from the liquidity point of view. You must evaluate the issuer-to-transfer ratios to see if the returns compared to traditional bonds are higher or not.

Complex To Learn Or Understand

As CLNs are structured products, they may be a little complex to learn or understand for an investor who has started his journey afresh. The complexity can double up if there is a lack of transparency on how CLNs work for investors. In other words, investors can find it highly challenging to gauge underlying credit portfolios. Ns work for investors. In other words, investors can find it highly challenging to gauge underlying credit portfolios.

The Bottom Line

CLNs are credit instruments that assess the credibility of product issuers along with other entities. A loan is usually given to the investor and he repays the loan component with interest.

And, in lieu of the same, the investors get their final capital sum at the time of redemption along with floating or fixed coupon payments. Therefore, these are bonds that provide better yields than traditional mortgages or fixed-income securities.

As wise investors, you can create a portfolio of underlying credit entities so that the default risk of one offsets the potential gains from other credit firms.

What are your thoughts on this? Do let us know in the comments below!