Introduction

A few decades back, the retail investment hub was pleasant and non-fussy. We could see investment offices tucked with trustees and asset managers designing portfolios for well-to-do clients.

There were institutional and retail investors who were high-heeled with financial wherewithals. Therefore, the investment or asset managers had no trouble devising a narrow range of financial instruments comprising high-quality debt and equity.

Financial innovation camouflaged with the rise in the number of investors is changing the overall landscape of the investment world.

As investors, you may want more investing options over traditional bonds or equities alone. Therefore, the third option is structured notes that combine debt and equity.

The notes can be customized to suit investor’s independent preferences and therefore the structured notes give rise to many other types of flexible financial products for investors.

Do structured products have fixed maturity?’ Well, we are going to have you covered on the same!

Structured products are hybrid investment portfolios with a debt and equity mix. The assets are linked to interest or fixed-income options and referenced to one or more variable derivatives.

The bond component of notes provides downside protection to the investor’s capital or principal investment and the potential of returns these notes earn depends on the performance of underlying notes these notes are linked to.

Do structured products have fixed maturity?

Structured products do not work similarly to traditional bonds, fixed-income securities, or other regularly traded investment options.

The notes use the bond component to save investor’s capital from investment erosion. This is because of spreads, cap limits, or buffers that are added to the notes. The returns of investment however depend on the performance of underlying assets the notes are linked to.

As the underliers are exposed to equity markets, the returns of income cannot be a fixed component but variable returns. The returns on investment are primarily performance-based for structured products.

However, investors can customize structured products that are principally guaranteed. These are 100% principal-protected notes that can assure you the return of your initial capital payoffs by the time of maturity.

How do structured products work?

As structured notes are hybrid investment products that link assets to interest rates camouflaged with one or more derivatives, the risks associated with structured products can also be quite complex for a newbie investor to handle.

The component of a structured note is an asset that is linked to equity-based assets and one or more derivatives. The asset allocation comprises equities, a basket of securities, stock-value indexes, and currencies to name a few.

The structured notes have debts linked to equity assets. The bond component helps mitigate losses and provides downside protection to investor’s capital. Therefore, the bond component in a note remains static or fixed in nature.

However, the returns or the exact payoffs in these products do not remain fixed as the return on investment is proportion to the performance of the underlying assets or equity index values the notes are linked to.

Most investors may not know how much returns the notes make until they hold the notes until maturity or until the time of redemption.

An exact know-how on how returns on investments work

The holders of structured notes receive their capital investment plus returns once they sign off. In other words, once the notes mature. As returns or payoffs are directly linked to the performance of assets, here is a calculation of how the Returns on investment work:

- Initial investment on a structured note of $12,000

- Payoffs from assets throughout the term= $2000

- Capped returns from the performing returns =$1000

- Actual returns on investment= Capital pay off plus capped returns= $12,000 + $ 1000 = $13,000

Structured products use swaps, options, and buffers to provide downside protection to investor’s capital and mitigate their losses.

The investor must know how assets work in bearish or bullish market scenarios. They must also evaluate what can be the returns on investment under a call or put options. This way, an average investor can more or less determine the value of the investment note at the time of maturity.

Case study on a worked-out example through an actual illustration

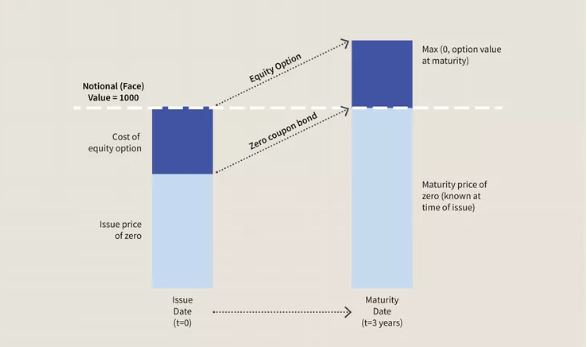

This is a zero-coupon bond with a notational face value of $1000. The bond is linked to an asset or derivative with a call option attached to it. This is an underlying equity instrument such as a common stock or an ETF that takes shape or operates like a popularly known index such as the S&P 500.

The maturity period for this structured note is a term of three years.

Here is a graphical representation of the same:

Image Courtesy: https://www.googleimages.com/

In the above-mentioned illustration, you discover that the pricing mechanisms that drive returns on investment look complex. But, the underlying principle remains fairly simple to decipher.

This is a note that is fully principal-protected. This means that the investor will get his $1000 back no matter how the underlying assets perform in the market. However, the zero bonds are issued to investors at the discounted face values as against the original price.

By the time, the zero-coupon bonds mature, investors get the bonds at their original price. To put it in simple terms, they receive their principal amount back.

As far as the performance component is concerned, you have the underlying asset that has a call option. And, the zero-coupon bond will have an intrinsic value that equals a higher value than what the bond was issued at. You receive your ROI on a one-to-one basis.

On the contrary, if the value of the asset is rendered worthless, you just get your principal money back which is $1000.

In a nutshell, you can conclude that the capital is protected and the returns are linked to the performance of an underlying asset or index the note is linked to.

What are the questions an investor may ask before investing in structured notes- Detailed insights into the same

These are the top questions an investor must ask before investing in structured notes. Let us have a look into what they are:

1. Are structured notes complex to learn or understand?

As structured notes comprise debt with equity, many investors have a misconception surrounding how notes work. The notes may be a little complex to learn or understand but when you have the right inclination to learn about the product you can get in touch with investment bankers or sign up for an appointment with a wealth manager to discuss how this investing portfolio works for investors.

2. How do structured notes work?

Structured notes combine debt with equity. Therefore, the bond lends downside protection against investor losses and protects the capital fund from entirely eroding while the upscale returns of the notes are linked to the performance of underlying assets that the notes are linked with.

3. What is the minimum level of investment concerning structured notes?

The minimum value for a structured note starts from 1 million or 100,000 USD. However, there are no upper limits to how far the portfolio can go up.

4. Can you give me a few examples of commonly traded structured notes?

Equity-linked Notes or ELNs, Reverse Convertible Bonds or RCBs, Principal protected notes, income notes, inflation-protected notes, commodity-linked notes, dual currency notes, and credit-linked notes are a few examples of structured notes that are currently trading in the market.

5. Tax implications concerning structured notes

Some of the income notes or coupon payouts you receive through structured notes might be considered as regular income sources and you might be taxed accordingly. Whilst, the lower tax slabs apply to incomes that fall under the ‘capital gains’ category.

To be in a safer haven, it is always a wise idea to get in touch with a tax advisor and discuss how tax implications work on different types of structured products. This way, you have a realistic overview of the income you have received less taxes paid.

6. For whom are structured notes available?

In the recent past, the notes were only available to high-net-worth retail investors and posh institutional investors. However, the changing landscape of the investment world has changed everything that is connected with how structured notes work and the prices have come down so that more retail segments are having a hands-on concerning these notes.

7. Are structured products entirely risk-free?

No, structured products are not entirely risk-free although the notes are designed to grow investor’s money over some time. You have credit, market, and liquidity risks that apply to structured notes and other types of investment products too. One must read the offer documents carefully before investing.

8. Who issues structured notes?

Investment-grade banks and high-scale institutional agencies usually tender or issue structured notes among posh or sophisticated investors. However, of late, these notes are also issued by secondary markets comprising stock exchanges and other securities-holding corporations at more affordable prices too.

However, the product may be subject to the risk over the creditworthiness of the issuer. The investor must check into the credibility of product issuers before investing in these notes.

Again, what type of commodities or stocks do you underline with your note? This plays a major role in the expected payoffs you get from the structured notes at the time of redemption.

Key takeaways from structured notes

- Structured notes combine debt and equity. While the debt comprises fixed-investment products, this is the component that lends downside capital protection to investors. The other component comprises asset allocation. The assets are equity-related assets like stocks, equity-based securities, and currencies to name a few.

- The notes are neither too risky nor entirely risk-free. They operate in more controlled situations with the inclusion of caps, buffers, or spreads on the investment portfolio. The returns are linked to the performance of underlying assets the notes are linked with.

- Structured notes can be customized to suit investor’s overall financial objectives. And, based on this, their maturity periods vary and do not remain fixed. You can choose short-term, medium-term, or long-term investment options based on your immediate financial needs or requirements.

- The notes offer variable payouts depending on the performance of underlying assets that are valued at the time of redemption. However, principal-protected notes offer the investor’s principal money despite the performance of underlying assets going adverse in the market.

The Bottom Line

In a way, structured products offer wider exposure to investors just dealing with regular bonds or equities on a stand-alone basis.

The market and credit risks apply to any form of investment and structured notes are no exception.

As an investor, you must read through market terms and conditions carefully before you accept any investment plan. The prospectus states the value of the return of principal vis-a-vis the diversification of income-earning plans.

The creditworthiness of mutual funds linked to bonds or ETFs may fluctuate and therefore the investor must determine the issuance of products on a case-by-case basis. Most investors may be willing to give up earnings but not their capital sum.