Introduction

As someone who would love to foray into the insurance industry, there are certain bizarre terms that can be equally confusing or harder to interpret.

However, to sign up for a policy and get your claim amount sanctioned, you must be on the know-how of how things work in the insurance industry.

On this parlance, let us understand the key points of differences covering Claims Made Vs Occurrence Insurance. Helping you get started here:

Claims Made- Meaning and Conceptualization Explained

When you talk about claims made, you refer to the claim requests that are filed by insurance subscribers in lieu of the contingency event the particular policy covers.

For instance, for a life insurance claim, you must file the death certificate of the primary policyholder. This is the contingency event for which the policy is taken.

Similarly, in the case of a cashless hospitalization, the policyholder would ask the hospital to submit the bills to the insurance company. The insurance service provider then settles the claims to the hospital center itself.

Likewise, the claims are made for the coverage amount the policy is primarily taken for.

What is meant by Occurrence Insurance- Meaning and Conceptualization Explained

Occurrence Insurance is a type of insurance wherein coverage gets triggered as long as the policy remains active in the marketplace. Here, the coverage gets triggered regardless of when the claims are being filed.

Say for instance, if the Govt declares a COVID-19 relief package for a specific country, then all the citizens residing in that particular country are entitled to receive the compensation or the package amount regardless of whether they filed for their claims or not.

Here, the coverage trigger occurs as and when the specified contingency event occurs.

Claims Made Vs Occurrence Insurance- Key Differences Explained

Helping you through a run-down of pointers covering key differences between Claims Made Vs Occurrence Insurance. Helping you get started here:

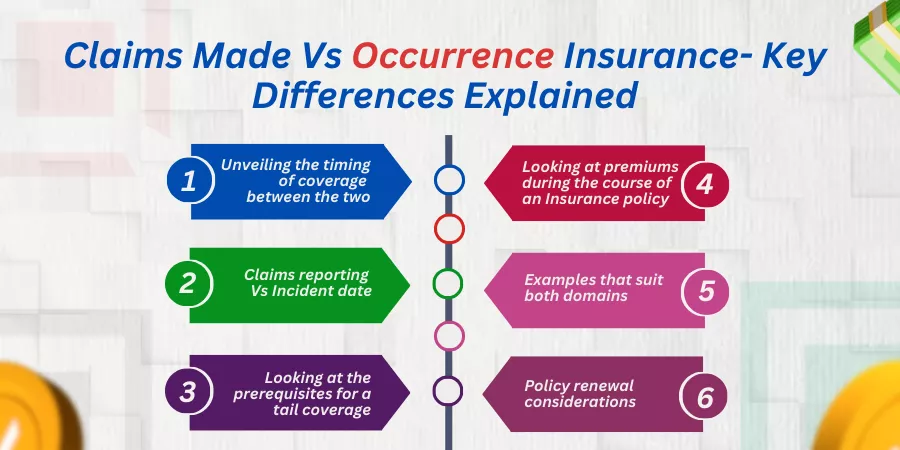

Unveiling the timing of coverage between the two

In the Claims-made policies scenario, the coverage happens as and when the claims are duly reported by policy subscribers. It can be at the time the claim events are reported. It could be an immediate hospitalization or a sudden outbreak of fire at the factory premises. The policyholder reports the events and produces claim bills in lieu of the damages the contingency suffers for him.

With respect to an Occurrence Insurance paradigm, the policy is timelined for as long as the policy exists. For instance, in a Tsunami coverage event, the policy gets covered the moment the trigger is announced. The policy does not lapse under a fixed tenor and can trigger years after the policy has elapsed too.

Claims reporting Vs Incident date

For a claims-made insurance scenario, the incident or the reporting must necessarily be done while the policy is in active force mode. The claims must be done approximately 10-15 days within the happening of the policy coverage event so as to receive the claim coverage money.

Whereas, in case of an occurrence policies, you can make a claim even after several years after the policy has elapsed. The claim trigger can be done anytime as long as the event happened during the tenor of the policy.

Looking at the prerequisites for a tail coverage

For a Claims scenario, if the policy is just about to expire, then you may have to apply for tail coverage or add an extra amount to activate the Extended Reporting Period or ERP so that the claim amount can be processed accordingly. This way, your time frame extends to avail the claim you may have incurred during the policy period.

Whereas, in Occurrence Insurance, you do not have a tail coverage concept at all. You can make a claim after several years since the policy has elapsed provided the event occurred during the policy period.

Looking at premiums during the course of an Insurance policy

For a Claim-based insurance policy, the premiums are lower at first. However, as the policyholder is of a higher age or the risk profile ratios alter, the premiums can spiral or increase in value accordingly. The cost of premiums can also increase if the policyholder has to buy tail coverage to extend the time frame or while switching between insurers.

Whereas, in an Occurrence Insurance, the premium amounts can be larger upfront. This is because the policy claims can be made even after the policy elapses as long as the initial trigger for coverage happens within the policy period. To substantiate the claim amounts that might have to be shelled out by insurance companies even later down the line, the additional premiums would be levied on to the customer.

Examples that suit both domains

In the case of Claims Made, the insurance suits general insurance policies like a health coverage policy, fire insurance, or term life insurance policies.

Whereas, in Occurrence Insurance, this is a kind of insurance that suits the liability division of individuals or businesses. Body injuries or property damage claims can be done under Occurrence Insurance policy norms.

Policy renewal considerations

For Claims made insurance plans, the policyholders have to constantly purchase tail coverage top-ups or reactivate the gap coverages by making extra payouts from time to time.

Whereas, with respect to Occurrence Insurance, the coverage can be done at any time regardless of the lapse of the policy. Here, the only criteria is that the policy event should have occurred during the tenure of the insurance.

Points to remember

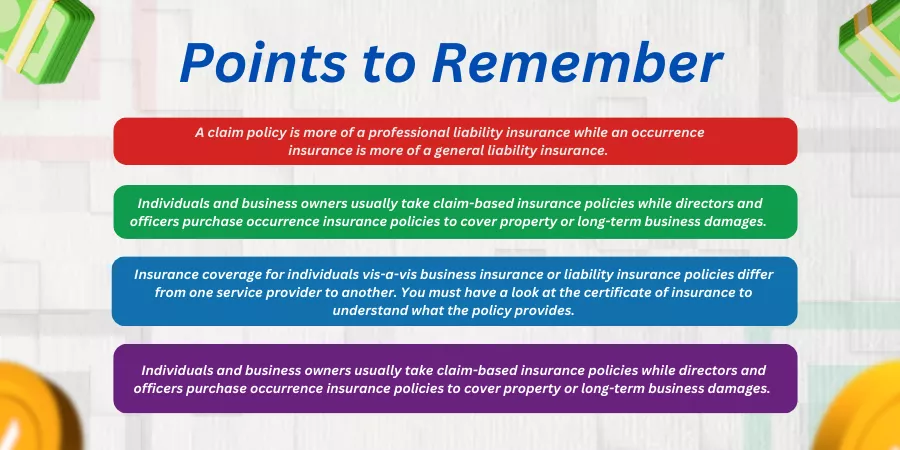

- A claim policy is more of a professional liability insurance while an occurrence insurance is more of a general liability insurance.

- Individuals and business owners usually take claim-based insurance policies while directors and officers purchase occurrence insurance policies to cover property or long-term business damages.

- Insurance coverage for individuals vis-a-vis business insurance or liability insurance policies differ from one service provider to another. You must have a look at the certificate of insurance to understand what the policy provides.

- To file a claim with the insured, the incident occurred or the claim must occur within tally with the tenor period of the concerned policy indeed. To provide coverage on one policy, you must not cancel the carrier or the insured company during the claimant period or the onset of a said retroactive date.

- To protect your coverage money, you can sue the insurance firm via a lawsuit if you do not receive your claims despite submitting documents correctly and diligently.

The Bottom Line

No one size fits it all. You must typically choose an insurance policy that suits your independent needs or requirements on the whole. Approach an insurance advisor to get the right guidelines on how different insurance policies work and discuss tailor-made solutions that can be customized to suit your overall needs to get the best value for money with respect to an insurance policy. What are your thoughts on this? Do let us know in the comments below!