Hidden Disaster Beneath Glamour

Salman is a successful young entrepreneur. He runs a thriving tech start-up, has a growing team, and just landed a major funding round.

Life is good, money is flowing easily and the future looks promising. But beneath the champagne toasts and celebratory high fives, there lies a hidden danger: financial blind spots.

What are financial blind spots?

Financial blind spots are the hidden pitfalls that can put abrupt breaks in even the most well-intentioned financial plans. These blind spots occur in various forms, such as overspending, inadequate savings, poor investment decisions, or lack of financial education.

All is well until cash flows. However, such a financial foundation fails to withhold even the slightest blow.

Businesses continuously evolve and life is uncertain. Any event like a change in market dynamics that affects the business cash flow or even personal circumstances like illness can change the course of good going, thanks to these financial blind spots.

Financial blind spots are areas in our financial lives that we may neglect or fail to recognize, leading to unforeseen consequences. Uncovering blind spots is a crucial step toward long-term success in an ever-evolving competitive landscape.

Blind spot 1: Lifestyle inflation:

Salman’s income has skyrocketed and with the rise in income his urge for a fancy living. He upgrades his apartment, splurges on designer clothes, and indulges in lavish weekend getaways.

Fancy gadgets without having an actual need keep on accumulating. Club memberships and subscriptions without the intention of meaningful networking eat time and money.

While these indulgences feel well-deserved, they’re slowly digging into his savings and putting his financial future at risk.

Blind spot 2: Neglecting emergency savings:

Reinvesting earnings is a simple and powerful way to grow wealth over time. But what if those reinvested funds fail to generate the same return as the original investment? That’s where reinvestment risk comes in – a possible pitfall that can erode your long-term gains.

Simply put, reinvestment risk is the chance that cash flows from an investment (like dividends or interest payments) are unable to reinvest at the same rate of return as the original investment. This risk arises because future market conditions may not be as favorable as the present.

Blind spot 3: Ignoring financial planning:

Retirement has not even yet crossed Salman’s mind. He’s focused on the present, neglecting the power of compound interest and the importance of the early retirement planning process.

He is investing most of his money towards depreciating assets like cars, gadgets, etc.

So, here he is with no emergency funds and no intentional retirement corpus accumulation. Sounds scary, right? Well, it is.

To make matters worse, there is no insurance in place. Unforeseen health issues can eat away even the deepest pockets; comprehensive health insurance is a must.

Insurance that safeguards in unforeseen events like fire and burglary has to be in place.

Blind spot 4: Untamed debt:

While Salman keeps his business finances separate, he has a lingering student loan and a sizeable credit card debt. He manages the minimum payments but doesn’t prioritize aggressively paying them off.

Well, compounding impacts debt as well right? These high-interest debts silently siphon off a portion of his income, hindering his ability to invest and build wealth.

Just think of it, the interest rate of any debt is usually higher than the return rate of savings and investment. So, firstly he is not saving, so no passive income generation.

On top of it, he is paying higher interest on his unsecured loans.

Blind spot 5: Lack of financial knowledge:

Salman makes his finances by instinct and feeling. He thinks ‘money matters are personal’ and doesn’t care to seek advice from financial planners. This lack of guidance leaves him vulnerable to making uninformed investment decisions or missing out on valuable financial opportunities.

Lifestyle philosophies like YOLO (you only live once), and My Life – My Rules should be taken in the right spirit. Most of these fancy life ideas are superficial and are marketed and branded in a way to lure you and make you buy what you may not need.

Also Read: Understanding the Benefits and Risks of Barrier Structured Notes

Salman’s story serves as a cautionary tale. Even amidst success, financial blind spots can lurk around the corner, impacting your present and threatening your future.

Addressing these potential blind spots requires both awareness and action:

Lessons to be learned

Lesson 1: Create a Realistic Budget:

Budgeting is primary to any financial planning. One must always be able to catch the pulse of own cash flows. Income-expense-savings must be the basis of all life decisions.

To avoid this blind spot, individuals can learn from Salman by creating a realistic budget that allocates funds for essential expenses, savings, and discretionary spending.

Regularly tracking expenses ensures financial discipline and prevents unnecessary financial strain.

Lesson 2: Prioritise Emergency Savings:

To overcome this blind spot, individuals should prioritize and consciously put efforts toward building an emergency fund. This fund must be enough to cover three to six months’ worth of living expenses in case of no income at all.

This safety net acts as a financial cushion during unexpected events, preventing the need to deplete other savings or rely on credit.

Lesson 3: Educate Yourself About Investments:

Awareness is the key to prosperity. Avoiding these common blind spots requires individuals to educate themselves about their own financial needs throughout their life cycle.

Its prudent savings and investments help us to meet the financial expectations at each stage. A financial advisor, friend, or relative can help you envision future expenses.

Whether it’s stocks, bonds, or real estate, understanding the basics empowers individuals to make informed decisions that align with their financial needs and financial goals.

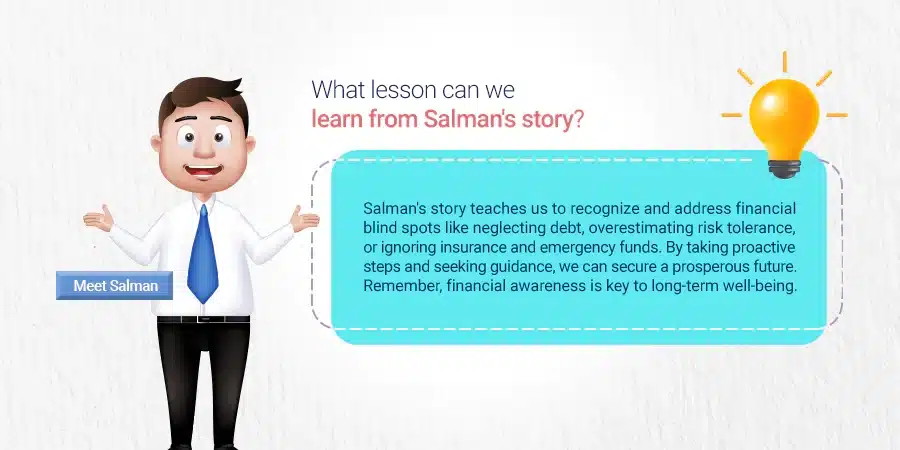

What does Salman’s tale tell us?

Salman’s experience is a cautionary and learning tale for all of us. Are you harboring any blind spots beneath you? Take the time to identify and address your common financial blind spots, whether it’s neglecting debt, overestimating risk tolerance, neglecting insurance, or ignoring emergency funds.

By taking proactive steps to address these blind spots, one can prevent disasters and lead a secure and prosperous life. Remember, financial awareness is not just about numbers; it’s about securing your well-being for the long haul.

By acknowledging and addressing his financial blind spots, Salman can regain control of his finances and build a secure future. His story serves as a reminder that financial success requires not just good earnings, but also budgeting, planning, educating, and consistency.

So don’t let your blind spots dim your financial future. The most important place to start to take control of your financial blind spots is to identify your current financial situation.

Take control, seek guidance, and build a foundation for a life of financial security and freedom.