Are you searching for a sound investment alternative that offers steady income and high yield? Welcome to the world of RCNs. In this article, we’ll be venturing deep into RCNs – how they work, their unique features, the risks involved, and tips to invest safely.

Get ready for an exciting dive into this unfamiliar financial landscape!

Key takeaways

● RCNs are a type of investment. They can give you more income but also come with risk.

● These notes use bonds, stocks, and options in unique ways. The payout depends on the performance of a related stock.

● RCNs offer higher gains than regular corporate bonds within shorter periods. But there is a chance to lose some or all of your money by the end.

● Before buying RCNs, learn about them and talk to an expert. Invest only if you understand these complex financial things really well and if it suits your interest for high-risk trades alongside steady returns expectation too on top priority.

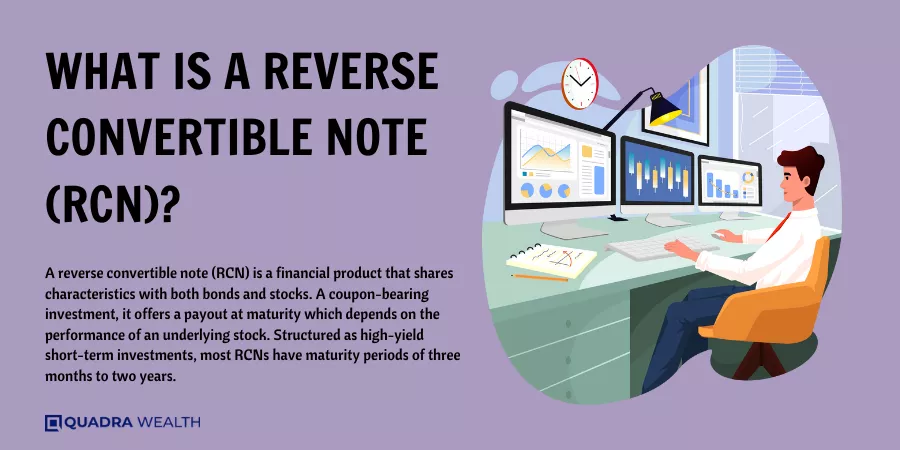

Understanding Reverse Convertible Notes (RCNs)

This section delves into the fundamentals of the Reverse Convertible Note, a type of structured product that combines elements of bonds, stocks, and options to create unique financial instruments.

It will delineate essential features such as the coupon rate, maturity term, and underlying stock – all pivotal determinants in calculating payouts for RCNs. Here we unravel complex concepts like how knock-in structure affects your initial investment amount or what role the secondary market plays in an RCN lifecycle.

Further understanding these key characteristics will empower you to mitigate associated risks while capitalizing on potential returns from this high-yield yet intricate investment opportunity.

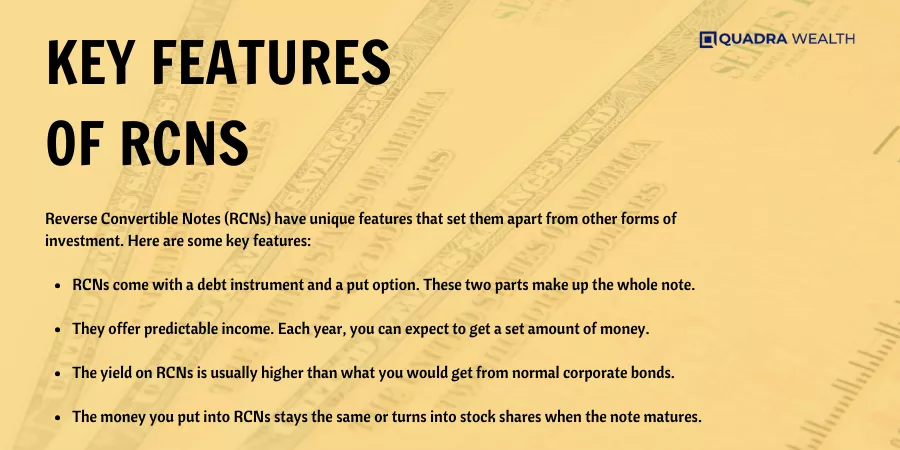

Key Features of RCNs

Reverse Convertible Notes (RCNs) have unique features that set them apart from other forms of investment. Here are some key features:

- RCNs come with a debt instrument and a put option. These two parts make up the whole note.

- They offer predictable income. Each year, you can expect to get a set amount of money.

- The yield on RCNs is usually higher than what you would get from normal corporate bonds.

- The money you put into RCNs stays the same or turns into stock shares when the note matures.

- There are basic structure and knock-in structure options for payout when the note matures.

While they bring in steady cash, RCNs also carry risks. You might lose some or all of your initial money by the time they mature.

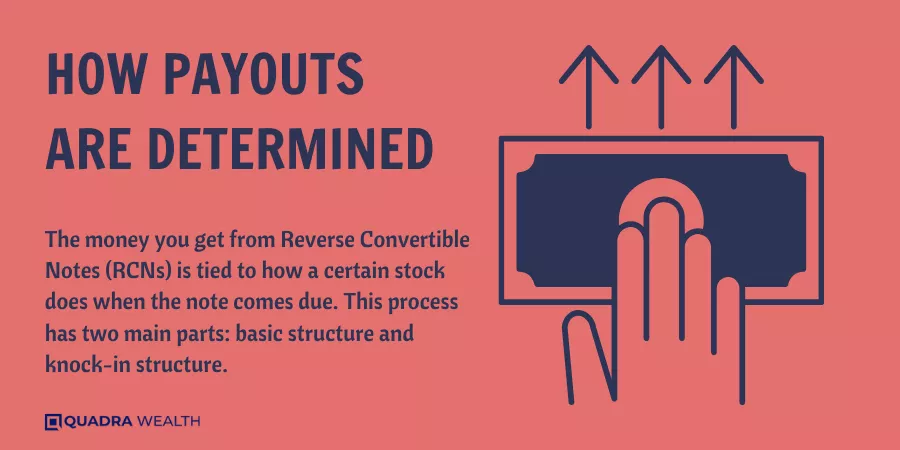

How Payouts Are Determined

The money you get from Reverse Convertible Notes (RCNs) is tied to how a certain stock does when the note comes due. This process has two main parts: basic structure and knock-in structure.

In the basic structure, if the underlying stock stays stable or grows by the end of the term, you get back your principal in full plus an agreed interest rate; this interest is called Coupon Rate.

The knock-in structure works when there’s a drop in stock price beyond what’s allowed – known as Knock-in level. Here, instead of money return on maturity, you may receive flawed stocks instead at their current low worth leading to a loss in initial investment amount.

Remember that payout results are varied; they rely on how well or poorly the original stock performs throughout its term life. It doesn’t mean sure returns always though it offers high coupons sometimes even during storms in market space.

Benefits of Investing in RCNs

Investing in Reverse Convertible Notes can be a good choice for many people. Here are some reasons why:

- Higher Yields: RCNs give more money than corporate bonds in the shorter term.

- Predictable Income: RCNs payout steady money through coupon payments.

- Reward Potential: You can make more money with RCNs because of their high risk.

- Low Investment: Even a small amount of money can get you a lot back in return.

- Downside Protection: If the stock’s value falls too low, RCNs will still keep some value.

Risks Associated with RCNs

RCNs can bring with them some risk. The price of the stock that the note sticks to might fall a lot. This could mean you lose some or all of your money when time is up. You do not get any extra money if the value of what the note sticks to goes up after it starts out.

It’s hard to sell RCNs before their times are up because not many people want to buy them from you, so they don’t have much liquidity in markets where you can sell them later on.

Some notes have a call rule which means they might be taken away from you when there is high income and low rates for borrowing money. You may also need to pay tax on any gains and normal earnings tax with RCNs, like capital gains tax and ordinary income tax.

With an RCN, your main amount of money put in is not promised back in full by banks issuing these notes, unlike other bank stuff like CDs or savings accounts.

This means that by its end term or maturity as it’s called, instead of getting real cash back like usually happens somewhere else, here under certain cases falling beyond the barrier level set during first buying terms known as a knock-in event happening due to market down trends impacting negatively over connected stocks outcome; we tend more likely than rare receive shares if underlying share prices drop below limit clauses given us before investing.

Comparing Reverse Convertible Notes with Fixed Coupon Notes

Investors are often faced with the decision between investing in reverse convertible notes (RCNs) or fixed coupon notes. Both investment options have their unique features, benefits, and risks, and understanding these can help investors make informed choices. The table below compares the two based on various factors such as yield, risk, and payout structure.

| Reverse Convertible Notes | Fixed Coupon Notes |

Yield | RCNs typically offer higher yields than traditional corporate bonds, especially over short maturities. This is largely due to the embedded put option. | Fixed Coupon Notes, on the other hand, provide fixed yields at regular intervals, usually bi-annually or annually. These are typically lower than the yields offered by RCNs. |

Risk | Investors can lose all or a part of their principal at maturity with RCNs, making them a higher-risk investment. The risk level is tied to the performance of underlying stocks. | Fixed coupon notes involve lower risk as they offer a guaranteed return at regular intervals irrespective of market conditions. However, they can also lose value due to inflation or a rise in interest rates. |

Payout Structure | The payout at maturity for RCNs can be determined by either a basic structure or a knock-in structure and is based on the performance of an underlying stock. | The payout for fixed coupon notes is fixed and is not dependent on the performance of any underlying asset. This assures investors a steady income stream. |

In conclusion, while RCNs offer higher potential returns, they also come with higher risk. Fixed coupon notes, in contrast, offer steady but generally lower returns with lower risk. The choice between the two depends on an investor’s risk tolerance, financial goals, and understanding of these complex investment instruments.

Suitable Investors for Reverse Convertible Notes

Reverse Convertible Notes (RCNs) are good for people who want a chance at more income. They can give more money than normal bonds over short time periods. However, RCNs come with risks. Some of the first cash given might be lost if things go wrong.

To buy RCNs, you must think that the stock linked to it will do well. If you believe the stock price won’t drop too much, this could work for you. It is important also to know about options before putting your money in RCNs.

This is because these notes use options as part of their rules to decide how to pay back your money and how much to some extent.

How to Invest in Reverse Convertible Notes Safely

Investing safely in Reverse Convertible Notes (RCNs) takes some steps. Here’s a clear plan to do it right:

- Learn about RCNs: Know what they are and how they work before you put money into them.

- Read and understand the terms: Each RCN comes with an offering circular and prospectus. Be sure to read these so you know what you’re getting into.

- Check the credit quality: The higher the quality, the safer your money is.

- Look at the stock attached to the note: If it’s stable or more valuable, it can provide a buffer against risks that come from bad stock moves.

- Talk with an expert: A financial advisor can help explain complex points and guide you through risks.

- Only invest money you can lose: With RCNs, it is possible for investors to lose all or part of their principal at maturity.

- Do not over-invest: Put only a small portion of your wealth into RCNs because there is limited secondary market liquidity for these notes.

- Look for steady income rather than high yields: Even though RCNs could offer better returns than other bonds, they come with higher risk too.

- Seek diversification: Don’t put all your money into one type of note or one industry.

- Buy protected investments if possible: Some RCNs are Capital Protected Investment (CPIs). They shield your initial investment amount from any loss tied to the underlying asset’s price fall.

- Follow the markets closely: Keep track of changes in bond interest rates and movements of related stocks.

- Check deadlines often: You should always be aware of when the note will mature so that you can plan ahead for repayment.

Conclusion

Reverse convertible notes aren’t for everyone. They make money when stocks stay level or rise a bit. But be careful, they can lose big if the stock falls a lot. Think hard before you buy them!

FAQs

RCNs are a type of debt instrument. They link bonds and stocks with a put option. RCNs are sometimes referred to as “revertible notes” or “reverse exchangeable securities”.

In simple terms, you make an initial investment in the RCN at its initial value. The note has a set coupon rate for principal and interest payments during its term to maturity.

Yes, when you invest in these forms of financial products like the RCN, risks exist such as credit risk and liquidity risk among others related to market volatility.

While they hold some secondary market value, selling might not fetch desirable results due to the structure’s complexity Incorporated with small-cap firms options making them less liquid than traditional corporate bond holdings.

If underlying stock dips under knock-in price level before note maturity; the investor bears a percentage of initial share price decline sharing capital loss incorporating short position strategy liability proportionate to the associated downside barrier

Major Financial Institutions issue such types of complex investments on Fortune 500 companies’ shares providing current income returns exceeding comparably-rated corporate bonds but with increased conditional drawback protection clauses incorporated ensuring capital isn’t secured completely against issuer default circumstances.