Understanding finance can be overwhelming, especially when it comes to differentiating between financial planning and investment planning. Did you know these two entities, while related, have distinct roles and processes? This blog post will simplify the complex aspects of these two concepts to help improve your personal financial management.

Keep reading as we delve into this topic that could potentially reshape your financial future for the better.

Key takeaways

● Financial planning is about your whole money life. It helps set goals and make a plan to meet them.

● Investment planning looks at how to grow wealth using things like stocks or real estate.

● Both types of plans are key for a good financial future. They help you know where your money goes and how it grows.

● These two work as one team, guiding your savings and spending choices so that you reach all your money goals.

Definition of Financial Planning

Financial planning is a big step in life. It helps you look at where you are today and where you want to be tomorrow. You take into account your current savings, income, and debt budget.

Then, you draw up a roadmap for your financial future.

This plan includes how much money you should save. Insurance coverage, retirement plans, taxes, and estate planning also play key parts in your plan. All these pieces come together to make sure that everything from daily costs to future goals gets covered!

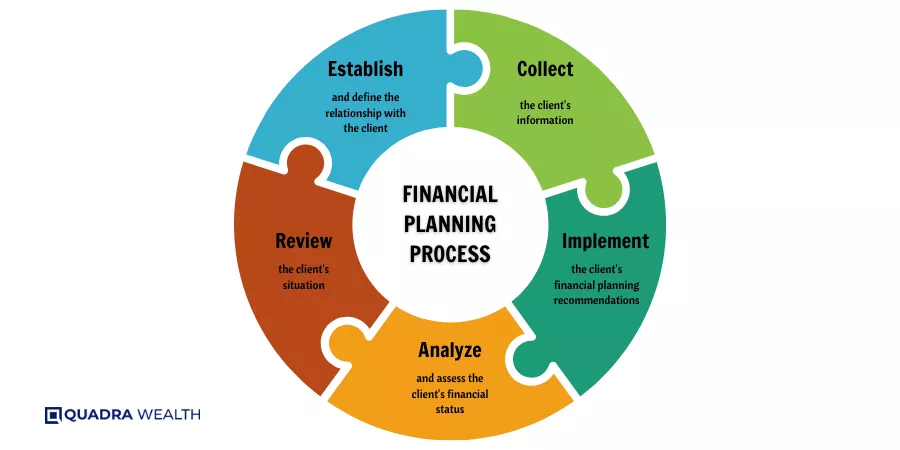

The Process of Financial Planning

Financial planning starts with assessing your current financial situation. This involves creating a summary of assets and debt, reviewing income and expenses, as well as evaluating insurance coverage and needs.

Once you grasp your present financial condition, the next step is to set clear short-term and long-term financial goals. These might include specific lifestyle shifts such as marriage, purchasing a house, or building a family that will impact your economic life.

Following this, it’s vital to develop a budget that includes future asset purchases, vacation allotment and other expected spending patterns alongside future income needs like retirement or inheritance provisions.

In case of any career changes or market volatility affecting these calculations, regular monitoring becomes essential for successful financial planning strategies leading to overall financial success.

Assessing Current Financial Situation

To know where you’re going, first, you must see where you are. That’s what assessing your current financial situation is all about. You need to list out all your assets like a house or car and any cash in the bank.

These are things of value that belong to you.

Then, make a note of any money owed such as credit card debt or loans. This is your overall financial condition right now. It makes up your ‘Net Worth Statement’. Your income after expenses is also vital here since it shows how much money stays each month for saving or spending.

This check-up helps spot problems early before they become big ones later on. When we look at our income and bills honestly, we can set clear and realistic financial goals.

Setting Financial Goals

Setting financial goals is an important step. You decide what you want to achieve with your money. Goals can be big or small. For example, buying a house, funding a child’s education, and saving for retirement are common goals.

Some people also set short-term goals like going on vacation or buying a car. While setting these goals, consider your current savings and future income needs. Planning helps make sure you have enough money in the future to meet all these goals.

Developing a Budget

Making a budget helps manage money. It is a part of financial planning. Here’s how to do it:

- First, know your income. Add up all the money you get each month.

- Next, list all your costs. These are things like rent or mortgage, food, and bills.

- Also,, note less regular expenses. These might be car repairs or doctor visits.

- Subtract your total costs from your income.

- The goal is for the number to be zero. Then every dollar has a job!

- If it’s not zero, adjust your plan. You may need to cut some costs.

- Revisit your budget often to stay on track.

- Goal setting

- Budgeting

- Risk management

- Wealth accumulation

- Peace of mind

- Time and effort

- Costs

- Market uncertainty

- Rigidity

- Overemphasis on money

Definition of Investment Planning

Investment planning is a smart step for wealth growth. It works with your money to make more money over time. It taps into things like stocks, bonds, real estate, and company retirement plans.

An investment plan looks at long and short-term goals.

This type of plan also takes care of risk factors in the market. It decides how much range to give each asset class – that’s what asset allocation means! This helps keep risks low and returns high.

With good diversification, you spread out your assets well too. Even if some parts fail, others will help cover the loss.

With an investment plan doing its job well, even times of market unrest become less scary! You have a sound strategy ready to take on any shakeups in the stock market or elsewhere.

Steps in Investment Planning

Investment planning starts with assessing your risk tolerance. It’s essential to understand how much market volatility you can handle without sacrificing your financial security or peace of mind.

Next, identify your investment goals. These may range from saving for retirement, buying a home, funding a child’s education or even taking a dream vacation. Once you’ve outlined your objectives, it’s time to plan the diversification and asset allocation in your portfolio.

This means spreading investments across different asset classes like stocks, bonds, real estate, and cash equivalents based on factors such as time frame and risk tolerance. Regular monitoring of these investments helps keep track of performance against set benchmarks while adjusting for any changes in circumstances or financial objectives.

Assessing Risk Tolerance

Knowing how much risk you can take is key. This step is called assessing risk tolerance. It means figuring out how okay you are with losing money. Some people might get scared and sell when the price drops.

Others may wait it out, hoping the price will go back up. Your comfort level can guide what kind of investment you make. You could choose stocks, bonds, cash, or real estate based on this step.

Identifying Investment Goals

Knowing what you want is the first step in any plan. For investment plans, we call these wants ‘investment goals’. They are the things you hope to get out of your investments. These could be short-term goals such as saving for a car or long-term ones like planning for retirement.

Each goal will need a different amount of money and time to reach it. It’s very important to know your goals well so that you can make a good investment plan!

Diversification and Asset Allocation

Diversification and asset allocation are key steps in investment planning. Diversification means spreading your money across different types of investments. This includes stocks, bonds, cash, and real estate. It helps to lessen risk.

- Assessing Risk Tolerance: Some people can handle more risk than others. Knowing your risk tolerance helps you decide where to put your money.

- Understanding Diversification: Don’t put all your eggs in one basket! Spread out your funds among stocks, bonds, or real estate.

- The Role of Asset Allocation: Assign specific amounts of money for each type of investment based on your comfort with risks.

- Regular Monitoring: Keep an eye on your investments often to ensure they’re still meeting your goals.

- Dealing With Market Risks: Even the market has its good and bad days. A good plan keeps these changes in mind and continues to work for you.

- Planning For Different Asset Classes: You can invest in debt, equity, or gold as well depending on what suits you best.

- Wealth Growth

- Diversification

- Financial Security

- Long-Term Goals

- Market Risks

- Volatility

- Continuous Monitoring

- Potential Losses

The Differences Between Financial Planning and Investment Planning

Financial planning and investment planning are two distinct processes that play integral roles in securing a financially stable future. Here is a table that highlights some of their key differences:

Financial Planning | Investment Planning |

Focuses on evaluating the current financial condition, setting goals, and creating a roadmap for the desired financial future. | Centers around long and short-term investment strategies to achieve specific goals. |

Considers aspects such as savings, budgeting, insurance, taxes, estate planning, and retirement. | Considers factors like risk tolerance, diversification, and asset allocation to maximize returns. |

Discusses objectives with a financial advisor or a certified financial planner, reviews the client’s financial profile, develops a financial plan, and implements recommended actions. | Requires regular review and adjustment based on market performance. |

More detailed and static in nature as the plan may not require frequent monitoring once made. | Subject to market risks and volatility, hence demands continuous monitoring and adjustments. |

Understanding these differences is crucial as it allows individuals to better manage their finances and investments, setting a foundation for a secure future.

The Importance of Both Financial and Investment Planning

Money plans are key to a good life. Financial planning helps us set and reach our money goals. We can plan for things like buying a house, saving for school, or getting ready for when we stop working.

This way, we know how much money we need and how much time it will take to save it.

Saving is not the only way to grow your wealth though. Investment planning lets us put our savings to work by buying assets that can make more money over time. This could be stocks, bonds, real estate, or other types of goods that might increase in value later on.

Both financial planning and investment planning help us secure our future and live the life we want.

How Financial and Investment Planning Work Together

Financial planning vs investment planning go hand in hand. They are like two wheels of a bike that move you toward your money goals. Financial planning is the map to the treasure; investment planning helps you pick the right tools to get there.

First, look at your whole money picture. This is what we call financial planning. It tells you about savings, spending, and all parts of your wealth. Next, invest smartly with an investment plan.

Your risk levels guide this step.

Now they join forces! The cash from a proper financial plan fuels investments. These grow and help achieve big life goals like buying a home or going on a dream vacation.

Keep them both working well by checking regularly if everything goes as planned – tweaking when needed. This way, they always work together for best results towards meeting personal targets.

Conclusion

Financial planning and investment planning are two sides of the same coin. They work together to make our money grow. Both help us set goals, plan steps, and check progress. So, we must use both for a secure financial future.

FAQs

Financial planning looks at all interrelated aspects of financial life, like income taxes, living expenses,, and company-sponsored retirement plans. Investment planning focuses on creating a comprehensive investment strategy to meet long-term goals.

An investment planner helps by picking the right mix of asset class returns, guiding during recession times, and advising on principles of wealth creation for maximum growth expectation.

Comprehensive financial planning includes calculating the sum needed for a house purchase or a child’s education after considering inflation, preparing annual cash flow reports, and tax calculations; it involves balance across savings ratio, solvency ratio, and liquidity rate.

You can build your future financial status through careful strategies for wealth creation like asset management, having multiple sources of income with high net worth wealth management strategies based on personal monetary policy.

If you have a high-income job with a financially stable employer and low debt levels then an aggressive strategy may work better due to higher risk-taking ability. But if there are high debts or unstable earning situations then conservative methods could be safer.

Pensions along with social security form part of retirement plan distributions which contribute positively towards one’s overall financial well-being leading to an idealistic post-retirement phase keeping up the desired lifestyle intact even though active earning stops.